|

市場調査レポート

商品コード

1444463

ミサイルおよびミサイル防衛システム:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Missiles and Missile Defense Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ミサイルおよびミサイル防衛システム:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

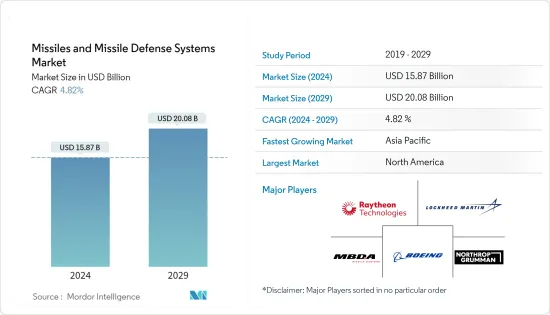

ミサイルおよびミサイル防衛システムの市場規模は、2024年に158億7,000万米ドルと推定され、2029年までに200億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.82%のCAGRで成長します。

新型ミサイルおよびミサイル防衛システム市場に対するCOVID-19の影響は、軍事支出と新世代ミサイル調達への軍の投資に影響がなかったため、無視できる程度でした。いくつかの国からの支出の増加と先進的なミサイル防衛システムの調達の増加が、パンデミック期間中の市場の成長を推進します。COVID-19のパンデミックにもかかわらず、世界の国防支出は2021年に2兆米ドルを超えました。

ミサイル市場は、主に新たな脅威に対抗するために軍隊が実施する調達とアップグレード活動により成長すると予想されています。軍用機、ヘリコプター、歩兵戦闘車(IFV)、発射装置と弾頭を搭載した装甲兵員輸送車(APC)の複数の契約が現在進行中であり、予測期間中に多くの新規契約が分散すると予想され、並行して需要が生み出されます。迎撃ミサイルやミサイル防衛システムなどの対抗手段。

いくつかの国は、新しい兵器システムを調達したり、既存の配備されているシステムを高度な兵器や次世代ミサイルで近代化することによって、現在の軍事力を増強するために多大な資源を費やしています。さらに、企業は、到来するステルス脅威を特定して阻止できる高度な監視システムの開発に取り組んでおり、これが市場の成長を促進すると予想されています。

ミサイル防衛システム市場動向

短距離ミサイルが市場シェアを独占

短距離ミサイルは、予測期間中に最大の市場シェアを占めると予測されています。短距離弾道ミサイル(SRBM)は、射程が約1,000 km(620マイル)以下の弾道ミサイルです。比較的低コストで構成が簡単なため、主に地域紛争における戦略的抑止力として配備されています。近隣諸国の間で増大する領土紛争は、敵対的な近隣国の戦略的拠点の脅威を標的にして無力化できる先進的なSRBMの研究開発と生産の主要な促進要因の1つです。さらに、防衛支出の増加と先進的な防衛システムの調達の増加がセグメントの成長を推進しています。

中国とインドの国境紛争や中国が戦略的軍事基地でインドを包囲していることも、インドが自国の海域と野鳥を守るための短距離ミサイルへの投資を誘発しています。新たな防衛強化計画の一環として、インドは国営の国防研究開発機構(DRDO)と提携して、新型の対艦・対空短距離ミサイルの導入に投資しています。 2022年1月、インド海軍はDRDOと協力して、短距離対空・対艦ミサイル(垂直発射短距離地対空ミサイル(VL-SRSAM))の試験に成功しました。海軍の軍艦。

中国の軍事的脅威を受けて、日本も2022年に防衛システムへの投資を大幅に増加させました。2021年12月時点での新たな投資8億8,000万米ドルは、紛争抑止と人民軍が配備している高度な兵器に対する対抗策の開発に使用されます。中国の解放軍(PLA)。同国は現在、現在わずか100~200kmの距離にある巡航ミサイルが1,000kmの距離にある物体を攻撃できるように改良・拡張することを計画しており、より遠くの敵目標に対する防御の可能性を高めています。

各国が相互に兵器の優位性を達成することを目指しているため、SCBMのアクティブなプログラムの数は大幅に増加しています。たとえば、2021年8月に中国人民解放軍は新型通常弾頭を搭載した単段弾道ミサイルの実験を行った。新たに開発されたミサイルは、インドのプリスビ・ミサイルに匹敵する精密攻撃能力を可能にするマルチモード・シーカーも備えていると推測されています。

北米が最大の市場シェアを占める

現在、北米地域が市場を独占しており、予測期間中も引き続き市場を独占すると予想されます。これは主に米国の最も高額な軍事支出によるものです。同国は、新しいミサイルとミサイル防衛システムの調達と開発に積極的に投資しています。 2022年度予算には、ミサイルと軍需品およびミサイル防衛プログラムにそれぞれ203億米ドルと109億米ドルが含まれています。ミサイル・軍需予算の下で、同国はヘルファイア・ミサイル、統合空対地ミサイル(JASSM)、統合直接攻撃弾(JDAM)、長距離対艦ミサイル(LRASM)、標準ミサイル(SM)の取得を計画しています。一方、ミサイル防衛プログラムの下では、同国は追加の標準ミサイル3ブロック IBおよびIIAミサイル、および終末高高度防衛(THAAD)迎撃ミサイルを調達することになります。

政府は新しいミサイルシステムの開発にも投資しています。同国はまた、世界のライバルである中国の脅威が増大する中、攻撃と防御のシステムを強化しています。中国の攻撃的な軍事行動はアジアの米国同盟国にも脅威を与えており、米国軍は必要な武器や防衛システムを日本と台湾の基地で自由に使える状態に保つようさらに駆り立てられています。ウクライナとロシアの戦争を受けて、米国は警戒を強めています。同国はロシアから守るため、新しいミサイルシステムを購入し、同盟国であるウクライナにこれらの兵器を供給しています。この一環として、同国は2022年6月、ウクライナに供給される予定の先進的な中長距離地対空ミサイル防衛システムの購入を発表しました。

ミサイル防衛システム業界の概要

ミサイルおよびミサイル防衛システム市場は細分化されており、市場には世界中および地域の多くの企業が存在します。ミサイルおよびミサイル防衛システム市場における著名な企業には、The Boeing Company、Lockheed Martin Corporation、Raytheon Technologies Corporation、Northrop Grumman Corporation、MBDA Inc.などがあります。これらの企業は、政府との長期的なパートナーシップや契約を通じて市場での存在感を高めています。政府機関と軍隊。たとえば、2021年 12月、レイセオンミサイル&ディフェンスは、米国向けのSM-2ブロック IIIAZオールアップ弾アップグレード 54発とスタンダードミサイル2オールアップ弾(SM-2ブロック)215発を製造するという5億7,800万米ドル相当の契約を獲得しました。 さらに、これらの企業は、新しいミサイルの研究開発に継続的に投資しており、統合兵器技術、ミサイルおよびミサイル防衛システムの関連製品およびソリューションの精度と効率の進歩を促進してきました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 範囲別

- 短距離

- 中距離

- 中級レベル

- インターコンチネンタル

- ミサイルの種類別

- ミサイル防衛システム

- 対空ミサイル

- 対艦ミサイル

- 対戦車ミサイル

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Raytheon Technologies Corporation

- The Boeing Company

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- MBDA Inc.

- BAE Systems plc

- Tactical Missile Corporation

- Israel Aerospace Industries Ltd.

- ASELSAN AS

- Kongsberg Gruppen ASA

- Saab AB

- Rheinmetall AG

- Roketsan AS

- Defense Research and Development Organization(DRDO)

第7章 市場機会と将来の動向

The Missiles and Missile Defense Systems Market size is estimated at USD 15.87 billion in 2024, and is expected to reach USD 20.08 billion by 2029, growing at a CAGR of 4.82% during the forecast period (2024-2029).

The impact of COVID-19 on the missiles and missile defense systems market was negligible as the military spending and the investments of armed forces into the procurement of new-generation missiles remained unaffected. An increase in expenditure from several countries and rising procurement of advanced missile defense systems drive the market growth during the pandemic period. Despite the COVID-19 pandemic, global defense expenditure reached over USD 2 trillion in 2021.

The missile market is expected to grow primarily due to the procurement and upgrade activities undertaken by armed forces to counter emerging threats. Several contracts for military aircraft, helicopters, infantry fighting vehicles (IFVs), and armored personnel carriers (APCs) mounted with launchers and warheads are currently underway, and many new contracts are anticipated to be dispersed during the forecast period, creating a parallel demand for countermeasures such as interceptor missiles and missile defense systems.

Several countries are expending significant resources toward augmenting their current military prowess by procuring new weapon systems or modernizing their existing deployed systems with advanced weapons and next-generation missiles. Furthermore, companies are working on developing advanced surveillance systems that may identify incoming stealth threats and intercept them, which is anticipated to boost the market's growth.

Missiles Defence System Market Trends

Short Range Missiles Dominated Market Share

Short-range missiles are projected to account for the largest market share during the forecast period. A short-range ballistic missile (SRBM) is a ballistic missile with a range of about 1,000 km (620 mi) or less. Due to their relatively low cost and ease of configuration, they are primarily deployed as a strategic deterrent in regional conflicts. The growing territorial disputes amongst neighboring countries are one of the major drivers of the R&D and production of advanced SRBMs capable of targeting and neutralizing threats at strategic strongpoints in a hostile neighboring country. Furthermore, rising defense expenditure and growing procurement of advanced defense systems drive segment growth.

The border conflict between China and India and China surrounding India with strategic military bases have also provoked India to invest in short-range missiles to protect the country's waters and birders. As part of the new defense upgrade plans, India has invested in introducing new anti-ship and anti-aircraft short-range missiles in partnership with its own state-run Defense Research and Development Organization (DRDO). In January 2022, the Indian Navy, in partnership with DRDO, successfully tested the short-range, anti-aircraft and anti-ship missile - the Vertical Launch Short Range Surface to Air Missile (VL-SRSAM) that is to be equipped with Indian Naval warships.

With military threats from China, Japan has also increased its investment in defense systems by significant margins in 2022. The new investment of USD 880 million as of December 2021 will be used for conflict deterrence and develop countermeasures against the sophisticated weapons being fielded by The People's Liberation Army (PLA) of China. The country is now planning to upgrade and extend the capability of its cruise missiles to hit objects at 1,000 km, which currently is at just 100 - 200 km, improving the chance to defend against farther adversary targets.

There has been a significant rise in the number of active programs for SCBMs as the countries aim to achieve arsenal superiority over each other. For instance, in August 2021, the Chinese PLA tested a single-stage ballistic missile with new conventional warheads. The newly developed missile is speculated to also feature a multi-mode seeker enabling precision strike capabilities comparable to the Indian Prithvi Missile.

North America Accounted for Largest Market Share

The North American region currently dominates the market and is expected to continue its dominance over the market during the forecast period. This is primarily due to the highest military spending in the US. The country is robustly investing in procuring and developing new missile and missile defense systems. The FY2022 budget entails USD 20.3 billion and USD 10.9 billion for missiles and munitions and missile defense programs, respectively. Under the Missiles and Munitions budget, the country plans to acquire the Hellfire missiles, Joint Air-to-Surface Missile (JASSM), Joint Direct Attack Munition (JDAM), Long Range Anti-Ship Missile (LRASM), and Standard Missile (SM)-6, whereas, under the Missile Defense programs, the country would procure additional Standard Missile 3 Block IB and IIA missiles, and the Terminal High Altitude Area Defense (THAAD) interceptors.

The government is also investing in the development of new missile systems. The country has also been strengthening its attack and defense systems with the increasing threat from its global rival, China. The aggressive military actions from China are also threatening US allies in Asia, further driving the US military to keep the necessary weapons and defense systems at its disposal in bases in Japan and Taiwan. In the wake of the war between Ukraine and Russia, the United States has been alert. The country has been purchasing new missile systems and supplying these weapons to its ally Ukraine to defend against Russia. As part of this, the country, in June 2022, announced the purchase of an advanced medium to long-range surface-to-air missile defense system that is expected to be supplied to Ukraine.

Missiles Defence System Industry Overview

The missile and missile defense systems market is fragmented, with many global and regional players in the market. Some prominent players in the missile and missile defense systems market are The Boeing Company, Lockheed Martin Corporation, Raytheon Technologies Corporation, Northrop Grumman Corporation, and MBDA Inc. The companies are increasing their presence in the market through long-term partnerships and contracts with government agencies and armed forces. For instance, in December 2021, Raytheon Missiles & Defense was awarded a contract worth USD 578 million to manufacture 54 SM-2 Block IIIAZ all-up round upgrades for the US and 215 Standard Missile-2 all-up rounds (SM-2 Block IIIA, IIIAZ, and IIIB variants) for seven partner nations (Chile, Denmark, Japan, the Netherlands, South Korea, Spain, and Taiwan). Furthermore, the companies continuously investing in the research and development of new missiles have been fostering the advancements in accuracy and efficiency of integrated weapon technologies and associated products and solutions of the missiles and missile defense systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Range

- 5.1.1 Short

- 5.1.2 Medium

- 5.1.3 Intermediate

- 5.1.4 Intercontinental

- 5.2 By Missile Type

- 5.2.1 Missile Defense Systems

- 5.2.2 Anti-Aircraft Missiles

- 5.2.3 Anti-Ship Missiles

- 5.2.4 Anti-Tank Missiles

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Raytheon Technologies Corporation

- 6.2.2 The Boeing Company

- 6.2.3 Lockheed Martin Corporation

- 6.2.4 Northrop Grumman Corporation

- 6.2.5 MBDA Inc.

- 6.2.6 BAE Systems plc

- 6.2.7 Tactical Missile Corporation

- 6.2.8 Israel Aerospace Industries Ltd.

- 6.2.9 ASELSAN A.S.

- 6.2.10 Kongsberg Gruppen ASA

- 6.2.11 Saab AB

- 6.2.12 Rheinmetall AG

- 6.2.13 Roketsan A.S.

- 6.2.14 Defense Research and Development Organization (DRDO)