白金族金属:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Platinum Group Metals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910459

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

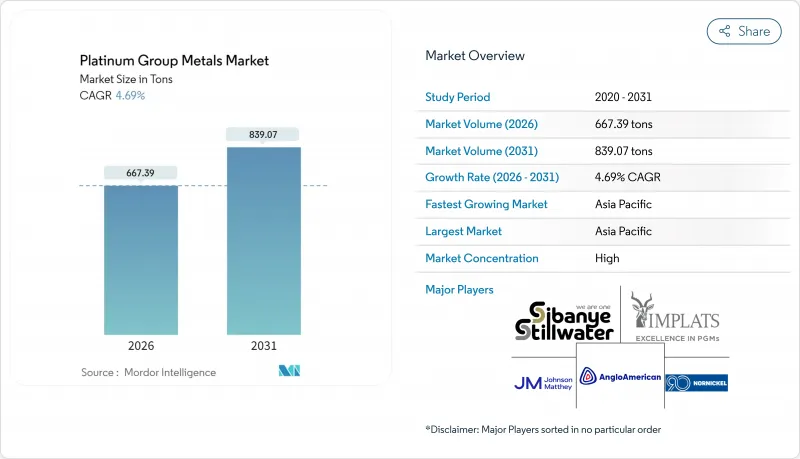

白金族金属市場は、2025年に637.51トンと評価され、2026年の667.39トンから2031年までに839.07トンに達すると予測されております。

予測期間(2026-2031年)におけるCAGRは4.69%と推定されております。

プラチナ族金属市場は、二つの需要源による恩恵を受けております。ガソリン車およびハイブリッド車向け自動車触媒の持続的な需要と、プロトン交換膜(PEM)水素技術における急速な普及拡大です。触媒におけるパラジウムからプラチナへの移行が短期的な市場心理を押し上げる一方、長期的な機会はグリーン水素の拡大に由来します。これにより、2025年までPEM電解装置向けプラチナ需要が前年比で倍増すると予想されます。イリジウムの供給制約、アジアにおける宝飾品の堅調さ、高度な電子機器におけるPGM使用量の増加が相まって、価格の基盤を支えています。一方で、価格変動の持続と南アフリカにおける生産コストの上昇が、特に燃料電池OEMメーカーにおける長期供給契約の締結を抑制しております。

世界のプラチナグループ金属市場の動向と洞察

自動車セクターにおける触媒コンバーター需要の拡大

乗用車、ハイブリッド車、大型トラックを合わせたPGM消費量は2024年に全体の60%を占めました。より厳格なユーロ7および中国VI-b基準により車両当たりのPGM使用量が増加し、ガソリン生産量の減少を相殺しています。ハイブリッド車用触媒は特にPGM含有量が高く、2025年の自動車触媒用プラチナ需要予測を8年ぶりの高水準である324万オンスに押し上げています。大型車両ではさらに高濃度のPGMが必要であり、乗用車の需要減速の影響を受けにくい収益性の高いニッチ市場を形成しています。アジアの市場規模と、クリーンエンジン推進のための政府支援策が相まって、プラチナ族金属市場は自動車需要に強く依存した状態を維持しています。

北米におけるPEM電解装置の増設

水素関連プラチナ需要は2030年までに875キロオンス(プラチナ総使用量の約10%)に達した後、2025年には再び倍増が見込まれます。カナダのクリーン水素税額控除(40%)と米国のインフレ抑制法が、数ギガワット規模の電解槽受注を支えています。イリジウムの供給不足が障壁となっており、2024年の生産量はわずか7.7トンでした。スモルテック社のナノスケールコーティング技術など、PEMセルにおけるイリジウム使用量を95%削減する技術的ブレークスルーは、供給拡大に不可欠です。こうした進展が、プラチナ族金属市場の長期的な成長基盤を確固たるものにしております。

高騰する生産コスト

南アフリカにおける電力制限と労働争議が採掘コストを押し上げました。アングロ・アメリカン・プラチナム社の2024年単位コストは6Eオンスあたり20,922ランド(前年比5%増)となりました。深部鉱床では高度な冷却技術と鉱脈安定化が必要であり、固定費ベースを押し上げています。価格低迷期には、スイング生産者は損益分岐点または赤字で操業するため、拡張のための資本能力が減少します。こうした力学は供給安定性に下方リスクを加え、プラチナ族金属市場における長期契約を制限します。

セグメント分析

パラジウムは、ガソリン触媒が消費を牽引し続けた2025年にPGM市場の46.55%を占めました。主にPEM電解槽陽極に使用されるイリジウムは、2031年までにCAGR8.92%で成長すると予測されており、全PGM中で最も高い伸び率を示します。供給逼迫と技術依存性によりイリジウムの価格プレミアムが維持され、今後数年間でPGM市場規模への貢献度が拡大します。プラチナの復活はガソリン触媒への代替需要に起因し、2023年だけで60万オンス超の需要転換が生じました。ロジウムは代替品が限られるため高価格を維持し、ルテニウムとオスミウムはニッチな化学・データストレージ用途で需要を拡大し、収益源の多様化を図っています。

PEMシステムと先進メモリの持続的な負荷増加により、イリジウムとルテニウムは特殊用途から主流用途へと移行しています。2024年のロジウム価格は平均5,375米ドル/オンスと、供給制約を示唆しています。プラチナの供給拡大と代替需要の定着により堅調な需要が維持され、PGM市場は安定化しています。ディスクドライブ等の技術廃棄物のリサイクル率向上はルテニウムの供給安定性を高め、価格上昇圧力を緩和する一方、電子機器メーカーが重視する循環型経済への貢献度を強化しています。

宝飾品分野は2025年においてもPGM消費量の28.75%を占め、特に中国・日本・インドにおいて最大の用途としての地位を確固たるものにしております。マクロ経済の軟調さにもかかわらず、静かな贅沢動向とプラチナの投資魅力が基礎需要を支えております。一方、燃料電池分野はマルチギガワット級電解装置プロジェクトや定置型電源プログラムに支えられ、28.47%のCAGRで急成長を遂げております。したがって、燃料電池スタック向けプラチナ族金属の市場規模は2031年まで急速に拡大すると予想されます。

排出規制基準の強化に伴い、自動車触媒は依然として不可欠です。半導体ノードが3nm以下に微細化するにつれ、電子機器用途も増加を続けています。ガラス繊維製造や顔料用途では白金の高い融点が活用され、医療機器分野ではカテーテルやステントへの生体適合性が重視されています。化学プロセス用触媒、特に硝酸製造や製油所の水素化分解プロセスでは、依然として多量かつ安定したPGM消費量が見込まれ、景気変動をヘッジする多様な用途基盤を提供しています。

プラチナグループ金属レポートは、金属種別(プラチナ、パラジウム、ロジウムなど)、用途別(自動車触媒、電気・電子機器など)、供給源別(一次(採掘)、再生/二次)、最終用途産業別(自動車、工業用化学品など)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は数量(トン)単位で提供されます。

地域別分析

2025年、アジアはプラチナ族金属市場において51.60%という圧倒的なシェアを占めました。これは、自動車触媒用パラジウムおよび宝飾品用プラチナの最大消費国である中国の地位に支えられたものです。北京が国内価格決定権の獲得を目指す中、広州先物取引所はプラチナおよびパラジウム先物契約を上場させました。これにより流動性が深まり、産業ユーザーが長期ポジションのヘッジを行うよう促しています(日経アジア)。日本の宝飾品需要の回復とインドの婚礼需要に牽引された装飾品需要が地域的な需要を強化する一方、台湾と韓国の電子機器産業クラスターが工業用消費を支えています。

欧州では、ドイツと英国の厳しい排出規制を背景に消費量が大幅に増加し、触媒負荷量が高まっています。今後導入予定のユーロ7規制により、乗用車・大型車両双方のPGM使用量が増加する見込みですが、電気自動車への移行が需要バランスを複雑化させています。欧州はPGMリサイクルの先進地域でもあります。ジョンソン・マッセイ社とウミコア社は、排出量を最小限に抑えながら自動車触媒金属を回収する最先端施設を運営しており、循環型経済の目標達成を支援するとともに、プラチナ族金属市場の安定化に貢献しています。

北米は水素政策とガソリン車販売の持続により成長拠点として台頭しています。カナダは世界第3位のパラジウム生産国、第4位のプラチナ生産国であり、2022年には主にオンタリオ州で71万オンスが採掘されました。オタワ政府のクリーン水素税制優遇策は電解装置プロジェクトを加速させ、同地域へのプラチナ・イリジウム需要をさらに喚起しています。米国のインフレ抑制法は水素ハブへの資金提供によりこの流れを強化し、プラチナ族金属市場の長期的な見通しを確固たるものにしております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 自動車産業における触媒コンバーターの需要拡大

- 北米におけるPEM電解装置の増設がプラチナ需要を加速

- 電子産業におけるプラチナ、パラジウム、ルテニウムの需要増加

- パラジウムによる白金触媒の代替が二金属の需要拡大をもたらす

- アジア太平洋諸国における宝飾品消費の拡大

- 市場抑制要因

- 生産および維持管理に伴う高コスト

- 燃料電池OEMによる長期的な引き受けを阻害する価格変動性

- リサイクル競合

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 金属タイプ別

- プラチナ

- パラジウム

- ロジウム

- イリジウム

- ルテニウム

- オスミウム

- 用途別

- 自動車用触媒

- 電気・電子機器

- 燃料電池

- ガラス、セラミックス、顔料

- 宝飾品

- 医療(歯科・医薬品)

- 化学産業

- その他(航空宇宙、センサー、水処理、法医学)

- ソース別

- 一次(採掘)

- 再生/二次

- 最終用途産業別

- 自動車

- 工業用化学品

- 再生可能エネルギーと水素

- 電子機器および半導体

- 宝飾品・高級品

- 医療機器

- ガラス製造

- 石油精製

- その他

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- African Rainbow Minerals Limited

- Anglo American plc

- BASF SE

- DOWA Holdings Co., Ltd

- Glencore

- Heraeus Group

- Impala Platinum Holdings Ltd

- Ivanhoe Mines

- Jinchuan Group International Resources Co. Ltd

- Johnson Matthey

- Norilsk Nickel

- Northam Platinum Holdings Limited

- Platinum Group Metals Ltd

- Sibanye-Stillwater Limited

- TANAKA PRECIOUS METAL GROUP Co., Ltd.

- Umicore

- Vale

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日