|

市場調査レポート

商品コード

1687270

世界の分散型サービス拒否(DDoS)保護- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Distributed Denial of Service (DDoS) Protection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の分散型サービス拒否(DDoS)保護- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

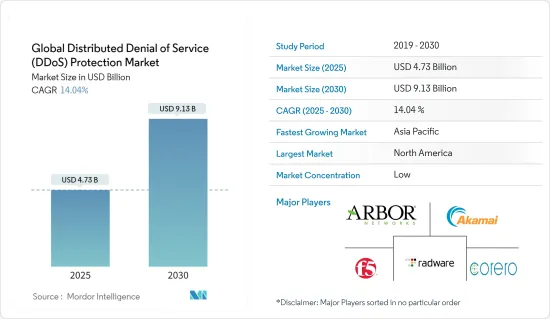

分散型サービス拒否保護の世界市場規模は、2025年に47億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.04%で、2030年には91億3,000万米ドルに達すると予測されています。

COVID-19パンデミックの出現により、労働環境は約全面的にウェブに移行しました。世界中の人々は、以前と比較して、ますますオンラインで仕事や勉強、買い物をするようになっています。これは最近のDDoS攻撃の目標にも反映されており、最も標的とされたリソースは、医療機関、配送サービス、ゲームと教育プラットフォームのウェブサイトです。

主要ハイライト

- ネットワーク攻撃の憂慮すべき増加は、DDoS保護ソリューションの採用の大きな原動力になると予測されます。このような攻撃の脅威は、使いやすいツールへの容易なアクセスと、恐喝による利益の可能性に対する犯罪者の包括的な理解によってもたらされています。これらの攻撃は、ビジネスシステムや個人を直接標的にするため、莫大な金銭的・個人的損失につながる可能性があります。

- 攻撃への対処に失敗すると、収益、生産性、評判、ユーザーロイヤルティに影響を及ぼす可能性があるため、企業に対するDDoS保護の要件は非常に重要な意味を持っています。Cloudflareによると、DDoS攻撃の金銭的負担は大きく、DDoS攻撃の被害を受けると、攻撃が1時間継続するごとに組織に約10万米ドルの損害が発生するため、DDoS保護ソリューションの需要はさらに高まっています。

- さらに、Cloudflareによると、DDoS攻撃の頻度と巧妙さは急増しています。第1四半期から第2四半期にかけて倍増した後、第3四半期に確認されたネットワーク層攻撃の総数は再び倍増し、その結果、第1四半期のCOVID-19以前のレベルと比較して4倍に増加しました。また、これまで以上に多くの攻撃ベクターが導入されたことも確認されました。SYN、RST、UDPフラッドが引き続き主流である一方、mDNS、Memcached、Jenkins DoS攻撃など、プロトコルに特化した攻撃が爆発的に増加しています。

- シスコによると、トラフィックが毎秒1ギガビットを超えるDDoS攻撃の数は、予測期間の半ば、すなわち2021年までに310万に増加すると予想されており、これは2016年から2.5倍に増加します。近年、こうした攻撃は頻度と深刻さを増しています。

- さらに、国別分布では米国がL3/4 DDoS攻撃の最多を観測しており、ドイツ、オーストラリアがこれに続いています。地域別では、北米(米国、カナダ)、欧州(ドイツ、ロシアなど)、中東(アラブ首長国連邦、クウェート)、アジア太平洋、オセアニア(オーストラリア、タイ、日本)が上位を占めています。

- 2021年第1四半期にDDoS攻撃が最も標的としたのは通信産業でした。Cloudflareによると、アプリケーション層への攻撃は増加傾向にあり、HTTPサーバーのリクエスト処理能力を妨害することを目的とした攻撃は大きな懸念材料となっています。また、身代金要求型のDDoS攻撃も2021年第1四半期に引き続き大きな課題となっています。

分散型サービス拒否(DDoS)保護市場の動向

高度化するDDoS攻撃事例の増加が市場を牽引

- さまざまな産業でDDoS攻撃の事例が急増しており、重要な組織サービスが中断され、さまざまな企業が数百万米ドルの損失を被っていることから、新興国全体で堅牢な保護ソリューションへの注目が高まっている

- インライン・ルーターやその他のネットワークサーバーなど、露出したネットワークインフラを標的とするネットワーク層攻撃は、ITと通信ベンダーのかなりの割合が業務を行っているデータセンターに大きな影響を与えています。Cloudflareによると、2021年1月に発生したネットワーク層攻撃の約44%は、同期フラグ(SYN)パケットフラッド攻撃が依然として最も多いです。その他、リセットフラグ(RST)パケット、ユーザーデータグラムプロトコル(UDP)、ドメインネームシステム増幅攻撃などが指摘されています。このような開発により、DDoS保護はこれらの産業で活動するベンダーにとって不可欠なものとなっています。

- 5Gにおける帯域幅の拡大と低遅延により、攻撃の量と深刻度はさらに増加すると予想されます。Coreroの調査によると、5Gの帯域幅が広いため、先進的ボットネットはできるだけ多くの携帯電話やIoTデバイスを利用して標的を無力化できます。

- さらに、COVIDの登場によるリモートワークの導入に伴い、個人のコンピューティングデバイスが必ずしも保護されていないため、安全でない在宅勤務環境からアクセスされた場合、企業ネットワークがより脆弱になり、ボットネットによるDDoS攻撃が増加しています。

- 世界中の企業が成長するにつれ、新たな先進的持続的脅威が重要なサービスをリスクにさらしています。このため、組織は潜在的な攻撃からエンドポイントやネットワークを保護するため、より優れたDDoSソリューションを導入するようになっています。

北米が大きなシェアを占める見込み

- 北米地域が大きなシェアを占めると予想される主要理由は、先進技術の導入が進んでいることと、サイバーセキュリティソリューションの導入が厳格化されていることです。厳しい規制やコンプライアンス要件を満たす必要があることから、同地域のエンドユーザー産業では先進的セキュリティシステムに対するニーズが高まっており、市場の成長を後押ししています。

- また、同地域はDDoS攻撃の件数も多く、複数のエンドユーザー産業に関して増加する可能性が高く、DDoS保護ソリューションの需要をさらに促進しています。さらに、この地域、特に米国ではサイバー攻撃が急増しています。同地域では、主に接続されたデバイスの数が急速に増加しているため、その数は膨大な数に達しています。

- また米国では、消費者がパブリッククラウドを利用し、バンキング、ショッピング、コミュニケーションの利便性を高めるために、複数のモバイルアプリケーションに個人情報がプリインストールされています。ここ数年、この地域の企業はDDoS攻撃の増加を目の当たりにしており、その結果、保護ソリューションに関する意識が非常に高まっています。また、ホワイトハウスの経済諮問委員会によると、米国経済は有害なサイバー活動によって年間約570億~1,090億米ドルを失っています。

- さらにAtlas VPNによると、米国では2020年3月だけで175,000件以上のDDoS攻撃があったと推定されています。攻撃者は米国保健福祉省のウェブサイトを無効にしようとしました。その主要目的は、COVID-19の大流行とそれに対する保護に関する公式データへのアクセスを市民から奪うことだったようです。

- 米国政府はまた、サイバー攻撃に対する国家防衛を強化するため、サイバーセキュリティとインフラセキュリティ機関(CISA)を設立する法律に署名しました。同庁は連邦政府と協力し、サイバーセキュリティツール、インシデント対応サービス、評価能力を提供し、提携する省庁の重要業務を支える政府系ネットワークを保護します。その結果、新規と既存の企業が、産業向けに設計された適切な保護スイートに投資するための新たな道が開かれました。

- さまざまな企業がスタンドアロン型の5Gネットワークを展開しているが、脅威が発生するかなり前に、ネットワークと攻撃に対するセキュリティに定着させるために、セキュリティパートナーが必要になると考えられます。例えば、2021年4月、DISH Network Corporationは、米国のクラウドネイティブなOpenRANベースの5GネットワークにおけるDDoS攻撃やボットネット攻撃に対するエンドツーエンドのユーザープレーンプロテクション(UPP)を提供するためにAllot Ltdを選択しました。

分散型サービス拒否(DDoS)保護産業概要

DDoS保護市場は、主に国内外の複数の参入企業で構成され、やや競争の激しい市場空間で注目を集めようとしのぎを削っています。同市場は、製品の普及が進んでいること、製品の差別化が中程度/高いこと、競合が多いことも特徴です。市場は製品中心であり、技術の進歩が常に市場を独占しています。イノベーション、研究開発投資、提携、M&Aは、市場で活動するベンダー間の競争戦略の一部となることが予想されます。全体として、競争企業間の敵対関係は激しく、予測期間中もそれは変わらないと予想されます。

- 2022年6月-G-Core Labsは、Intelとの提携により、全体的なレイテンシへの影響を抑えながらDDoS攻撃を緩和するスタンドアロンソリューション(eBPF)を発表しました。このXDPベースのソリューションは、専用のDDoS保護サーバーの役割を不要にし、SYNフラッドDDoS攻撃を保護します。

- 2022年3月-リアルタイムで高性能なDDoSサイバー保護ソリューション・プロバイダーであるCorero Network Securityは、ボットネットとカーペットボム攻撃に対する自動保護機能を拡大しました。同社の使命は、DDoS攻撃による混乱やダウンタイムから保護することで、インターネットをより安全なビジネスの場にすることです。

- 2022年2月-RadwareはSecurityDAMを3,000万米ドルで買収し、買収後のラドウェアのクラウドDDoS保護サービスには最大1,250万米ドルの成功報酬を支払う。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 二次調査

- 一次調査

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 巧妙なDDoS攻撃の増加

- 費用対効果の高いクラウドベースとハイブリッドソリューションの導入

- 様々な産業における技術の普及とIoTの採用

- 市場課題

- ネットワークと展開の複雑化

第6章 関連する使用事例と使用事例

第7章 市場セグメンテーション

- コンポーネント

- ソリューション

- サービス

- 導入タイプ

- クラウド

- オンプレミス

- ハイブリッド

- 企業規模

- 中小企業

- 大企業

- エンドユーザー産業

- 政府と防衛

- IT・通信

- 医療

- 小売

- BFSI

- メディアエンターテイメント

- その他

- 地域

- 北米

- 欧州

- アジア太平洋

- その他

第8章 競合情勢

- 企業プロファイル

- Arbor Networks Inc.(NetScout Systems Inc.)

- Akamai Technologies Inc.

- F5 Networks Inc.

- Imperva Inc.

- Radware Ltd

- Corero Network Security Inc.

- Neustar Inc.

- Cloudflare Inc.

- Nexusguard Ltd

- Dosarrest Internet Security Ltd

- Verisign Inc.

第9章 投資分析

第10章 市場の将来

The Global Distributed Denial of Service Protection Market size is estimated at USD 4.73 billion in 2025, and is expected to reach USD 9.13 billion by 2030, at a CAGR of 14.04% during the forecast period (2025-2030).

With the emergence of the COVID-19 pandemic, working environments have shifted almost entirely to the web. People worldwide have increasingly started working, studying, and shopping online as compared to before. This has also been reflected in the goals of recent DDoS attacks, with the most targeted resources being the websites of medical organizations, delivery services, and gaming and educational platforms.

Key Highlights

- An alarming increase in the number of network attacks is anticipated to be a significant driver for the adoption of DDoS protection solutions. The threat of these attacks is driven by ready access to easy-to-use tools and a more comprehensive criminal understanding of its potential for profit through extortion. These attacks directly target business systems and individuals, which could lead to enormous financial and personal losses.

- The requirement for DDoS protection for enterprises has gained tremendous significance, as failure to deal with the attacks can affect revenue, productivity, reputation, and user loyalty. According to Cloudflare, the financial burden of a DDoS attack is significant, as falling victim to a DDoS attack can cost an organization around USD 100,000 for every hour the attack lasts, further fuelling the demand for DDoS protection solutions.

- Additionally, as per Cloudflare, DDoS attacks are surging in frequency and sophistication. After doubling from Q1 to Q2, the total number of network layer attacks witnessed in Q3 doubled again, resulting in a 4x increase compared to the pre-COVID-19 levels in the first quarter. The company also witnessed more attack vectors deployed than ever. While SYN, RST, and UDP floods continue to dominate the landscape, the company saw an explosion in protocol-specific attacks such as mDNS, Memcached, and Jenkins DoS attacks.

- As per Cisco, the number of DDoS attacks exceeding 1 gigabit per second of traffic is expected to rise to 3.1 million by the mid-forecast period, i.e., by 2021, which is a 2.5-fold increase from 2016. In recent years, these attacks have increased in frequency and severity.

- Moreover, the United States observed the highest number of L3/4 DDoS attacks under the country-based distribution, followed by Germany and Australia. The top countries affected by region include North America (United States, Canada), Europe (Germany, Russia, among others), the Middle East (UAE, Kuwait), Asia-Pacific, and Oceania (Australia, Thailand, Japan).

- The telecom industry was at the top when DDoS attacks most targeted it during the first quarter of 2021. According to Cloudflare, application-layer attacks are on the rise, and those that aim to disrupt the HTTP server's ability to process requests are reasons for significant concern. Also, ransom DDoS attacks continued to be a significant challenge during the first quarter of 2021.

Distributed Denial of Service (DDoS) Protection Market Trends

Increasing Instances of Sophisticated DDoS Attacks to Drive the Market

- The rapidly rising instances of DDoS attacks across multiple industries, which have disrupted crucial organizational services and the loss of millions of dollars for various companies, have increased the focus on robust protection solutions across emerging economies.

- Network layer attacks that target exposed network infrastructure such as inline routers and other network servers significantly impact data centers where a significant share of IT and telecom vendors operate. According to Cloudflare, about 44% of network layer attacks occurred in January 2021, with synchronizing flag (SYN) packet flood attacks remaining the most common. Other attacks noted included reset flag (RST) packets, user datagram protocol (UDP), and domain name system amplification attacks. Due to such developments, DDoS protection is vital for vendors operating in these industries.

- The increased bandwidth and low latency in 5G are further anticipated to increase the volume and severity of the attacks. According to Corero's study, the higher bandwidth of 5G enables advanced botnets to harness as many mobiles or IoT devices as possible to cripple their targets.

- Further, with the adoption of remote working due to the onset of Covid, corporate networks have become more vulnerable when accessed from unsecured work-from-home environments, as personal computing devices are not always protected, thus causing an increase in Botnet DDoS attacks.

- As businesses worldwide grow, new and advanced persistent threats have exposed critical services to risk. This has encouraged organizations to deploy better DDoS solutions to safeguard their endpoints and networks against potential attacks.

North America is Expected to Hold a Major Share

- The North American region is expected to hold a significant market share, primarily due to the higher adoption of advanced technologies and stricter implementation of cybersecurity solutions. Given the need to meet stringent regulatory and compliance requirements, there is a rising need for advanced security systems among the region's end-user industries that positively boost the market's growth.

- The region also accounts for a significant number of DDoS attacks, which are likely to increase with respect to multiple end-user industries, further driving the demand for DDoS protection solutions. Moreover, cyberattacks in the region, especially in the United States, are increasing rapidly. They are reaching high numbers, primarily owing to the rapidly increasing number of connected devices in the region.

- Also, in the United States, consumers have been using public clouds, and multiple mobile applications are preloaded with personal information for the convenience of banking, shopping, and communication. In the past few years, companies in the region have been witnessing increasing DDoS attacks, which has resulted in tremendous awareness related to protection solutions. Also, according to the White House Council of Economic Advisers, the US economy loses approximately USD 57 billion to USD 109 billion per year to harmful cyber activity.

- Moreover, according to Atlas VPN, it was estimated that there were more than 175,000 DDoS attacks in the United States in March 2020 alone. Attackers tried to disable the website of the US Department of Health and Human Services. The primary purpose seemed to deprive the citizens of access to official data regarding the COVID-19 pandemic and the measures being taken against it.

- The US government also signed a law to establish the Cybersecurity and Infrastructure Security Agency (CISA) to enhance the national defense against cyberattacks. The agency works with the federal government to provide cybersecurity tools, incident response services, and assessment capabilities to safeguard the governmental networks that support essential operations of the partner departments and agencies. As a result, it opens new avenues for the new and existing companies to invest in a suitable protection suite designed for the industry.

- Various firms are deploying standalone 5G networks, and they would need security partners to become ingrained in their network and security against attacks well before a threat occurs. For instance, in April 2021, DISH Network Corporation chose Allot Ltd to provide end-to-end User Plane Protection (UPP) against DDoS and botnet attacks on the United States' cloud-native, OpenRAN-based 5G network.

Distributed Denial of Service (DDoS) Protection Industry Overview

The DDoS protection market primarily comprises multiple domestic and international players fighting for attention in a somewhat contested market space. The market is also characterized by growing product penetration, moderate/high product differentiation, and high levels of competition. The market is product-centric, and technological advancements constantly govern it. Innovations, R&D investments, partnerships, and M&As are expected to be part of the competitive strategy among the vendors operating in the market. Overall, the intensity of the competitive rivalry is high, and it is expected to remain the same during the forecast period.

- June 2022 - G-Core Labs, in partnership with Intel, launched a standalone solution (eBPF) providing mitigation of DDoS attacks with a low impact on overall latency. The XDP-based solution removes the need for a dedicated DDoS protection server role and protects against SYN Flood DDoS attacks.

- March 2022 - Corero Network Security, a real-time, high-performance DDoS cyber defense solutions provider, extended its automatic protection against Botnet and Carpet Bomb attacks. The company's mission is to make the internet a safer place to do business by protecting against the disruption and downtime caused by DDoS attacks.

- February 2022 - Radware acquired SecurityDAM for USD 30 million, with contingent payments of up to USD 12.5 million for Radware's cloud DDoS protection service after the deal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Instances of Sophisticated DDoS Attacks

- 5.1.2 Introduction of Cost-effective Cloud-based and Hybrid Solutions

- 5.1.3 Proliferation of Technology and Adoption of IoT across Various Verticals

- 5.2 Market Challenges

- 5.2.1 Growing Network and Deployment Complexities

6 RELEVANT USE CASES AND CASE STUDIES

7 MARKET SEGMENTATION

- 7.1 Component

- 7.1.1 Solution

- 7.1.2 Service

- 7.2 Deployment Type

- 7.2.1 Cloud

- 7.2.2 On-premise

- 7.2.3 Hybrid

- 7.3 Size of Enterprise

- 7.3.1 Small and Medium Enterprises

- 7.3.2 Large Enterprises

- 7.4 End-user Industry

- 7.4.1 Government and Defense

- 7.4.2 IT and Telecommunication

- 7.4.3 Healthcare

- 7.4.4 Retail

- 7.4.5 BFSI

- 7.4.6 Media and Entertainment

- 7.4.7 Other End-user Industries

- 7.5 Geography

- 7.5.1 North America

- 7.5.2 Europe

- 7.5.3 Asia-Pacific

- 7.5.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Arbor Networks Inc. (NetScout Systems Inc.)

- 8.1.2 Akamai Technologies Inc.

- 8.1.3 F5 Networks Inc.

- 8.1.4 Imperva Inc.

- 8.1.5 Radware Ltd

- 8.1.6 Corero Network Security Inc.

- 8.1.7 Neustar Inc.

- 8.1.8 Cloudflare Inc.

- 8.1.9 Nexusguard Ltd

- 8.1.10 Dosarrest Internet Security Ltd

- 8.1.11 Verisign Inc.