|

市場調査レポート

商品コード

1444246

プレハブ建築:市場シェア分析、業界動向と統計、成長予測(2024-2029年)Prefabricated Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| プレハブ建築:市場シェア分析、業界動向と統計、成長予測(2024-2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

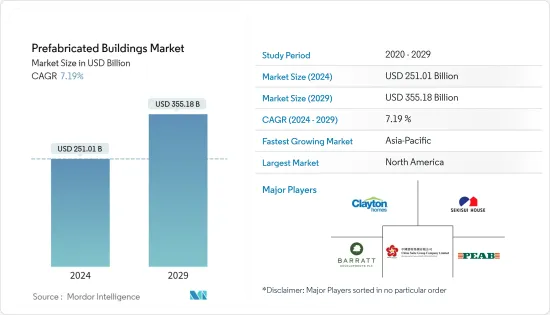

プレハブ建築市場規模は2024年に2,510億1,000万米ドルと推定され、2029年までに3,551億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.19%のCAGRで成長します。

COVID-19のパンデミックとそれに伴うロックダウンにより、世界中のすべての建設関連業務が停止しました。その結果、教育、住宅、空港などのさまざまな建設分野でのモジュール工法プロジェクトが減少し、プレハブ建築の需要に大きな影響を与えました。数カ所でサプライチェーンも寸断され、必要な建設資材の配送に遅れが生じ、建設活動に影響が出ました。

欧州での積層造形の導入により、プレハブ建築セクターが大幅に成長すると予想されます。企業は、競合との差別化を図るために、環境に優しい製品や生産方法を採用しています。エネルギー効率を重視した結果、マイクロハウスなどのエネルギー吸収材のイントロダクションです。

この地域、特にスイス、北欧、英国での市場拡大を推進するもう1つの大きな要因は、ターンキーソリューションの導入です。欧州のプレハブ建築業界はドイツ、北欧諸国、英国が主流です。

英国はプレハブ建築会社にとって有望な市場です。主要企業は、市場の成長の可能性とモジュール工法アプローチを活用するために、パフォーマンスと生産性の向上に投資しています。建設業界における既存の熟練労働者の不足は、欧州のプレハブ建築業界における英国の地位を維持する重要な要素となっています。

将来的にさらに数百、数千のプラントが必要とされるインドでは、プレハブ企業には大きなチャンスがあります。インドは今後数年間で建設生産高が最も急速に成長する国の一つになると予想されており、テクノロジーが重要な要素となっています。

インドは今後5年間で世界第2位の建築市場になると予測されています。デジタル化とBIMなどの最先端の建設技術の導入を政府が継続的に推進していることが、プレハブ建築物の導入を促進する主な要因となっています。「デジタルインディア」、「みんなの住宅」、「バラトマラパリヨジャナ」などの政府の取り組みにより、インドではプレハブ建築の使用が促進されています。

スペインに輸入されるプレハブ建築の価値は、2022年に大幅に増加しました。2003年から2007年にかけて、これらの製品の輸入は増加し、その価値は1億100万ユーロ(1億978万米ドル)に達しました。その後、輸入額は減少傾向にあり、2012年には3,600万ユーロ(3,913万米ドル)に達しました。2021年にスペインに輸入されたプレハブ建築物の評価額は6,500万ユーロ(7,065万米ドル)でした。

プレハブ建築市場の動向

モジュール工法の需要の高まり

発展途上国における急速な経済発展と多くの富裕国における歴史的な低金利により、建設需要が高まっています。これに伴い、可処分所得の増加、技術の進歩、民間の建設投資の増加などの要因により、市場は予測期間を通じて上昇すると予想されます。さらに、世界中の政府による住宅とインフラへの支出の拡大が市場の拡大を促進しています。時間とコストは、多くの新興経済国で業界の拡大に対する障壁として長い間見なされてきた、構築運営に関連する2つの要因です。この制限を克服することは、世界中の多くの重要な建築企業にとって主要な課題の1つです。プレハブ建築システムは、これらの問題に対する主な解決策の1つです。

プレハブ建築技術は、今日の市場において建設時間を30~50%削減でき、代替手段を提供します。現場での手続きの人員が少なくて済むので経済的です。オンサイト活動が減少するプロセスのもう1つの意図しない結果は、生成されるゴミの量が大幅に減少することです。これらの利点により、プレハブ建築システムの活動は建設分野で人気が高まっています。

シンガポールやインドのような国では、政府が建築・建設部門の活性化に大規模な投資を行っており、ビジネスは活況を呈しています。オーストラリア貿易投資委員会は、シンガポールが公共インフラに毎月少なくとも20億米ドルを支出していると推定しています。さらに、オランダの建設産業は、2050年までに国内に循環経済を構築することを目的とした政府の循環経済プログラムのおかげで成長しています。

プレハブ建築システムは、環境に優しく、柔軟性があり、現場への混乱が少なく、コスト削減ができるなど、いくつかの利点があるため、住宅および非住宅構造物の建設に広く採用されています。したがって、世界中で建設活動が増加するにつれて、換気熱パネルなどのプレハブ建築システムの需要が大幅に拡大すると予想されます。結果として、このような政府の取り組みや建築分野への投資が市場の推進力となっています。

アジア太平洋は市場で最も高い成長が見込まれる

アジア太平洋のプレハブ建築市場は、今後5年間で最高の成長を遂げると推定されています。日本のプレハブ建築市場は、世界の他の地域に比べて比較的成熟し、発展しています。

安価な住宅に対する需要は、市場を牽引する主な要因の1つです。プレハブ住宅は、アジアおよび太平洋の島嶼国のいくつかにおいて、安価な住宅が不足しているという問題に対する現実的な解決策となり得る。プレハブ構造物は従来の建物よりも迅速に建設でき、通常は安価であるため、建設コストの削減に役立ちます。

建設活動の成長は、業界に影響を与えるもう1つの重要な側面です。近年、アジア太平洋地域では大幅な都市化が見られ、建設活動が増加しています。住宅、商業、産業開発プロジェクトはすべて、プレハブ建築の利用から恩恵を受けることができます。

一般的な建築基準ではなく、業界に特化した訓練を受けた専門家による検査も、日本のプレハブ住宅市場の発展に貢献しています。プレハブの概念はインドの建設市場で注目を集めています。

インドにおけるプレハブ住宅の参入により、別荘や集合住宅など、あらゆる種類の建設に革新的で技術的に進んだ建設および設計手法への道が開かれました。

日本では人口減少が進み、高齢化が進むため、新築住宅の需要も減少していることは否定できません。縮小する国内市場で新築需要が減少する中、両社は中国や他のアジア諸国での潜在的な成長を取り込もうとしています。

プレハブ建築業界の概要

この調査では、プレハブ建築業界の主要企業が対象となっています。市場は細分化されていますが、さまざまな発展途上国と先進国でのプレハブ建築への投資と今後の重要なプロジェクトが増加するため、予測期間中に成長する可能性があります。主要なプレーヤーには、Clayton Homes、Sekisui Homes、China Saite Group Company Limited、PEAB、Barratt Developments PLCが含まれます。

近年、その効率の良さからプレハブ建築の利用が増えています。これは住宅に限ったことではありません。プレハブ建築にはレストラン、ホテル、ケータリング施設などが入居する予定です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

- 分析調査手法

- 調査段階

第3章 エグゼクティブサマリー

第4章 市場洞察とダイナミクス

- 現在の市場シナリオ

- 市場力学

- 促進要因

- モジュール工法の需要の高まり

- アジア太平洋は市場で最も高い成長が見込まれる

- 抑制要因

- 消費者と建設業者の間でプレハブ建築に対する認識と受け入れが不足

- プレハブ建築に伴う輸送コストと物流コストの増加

- 機会

- 持続可能で環境に優しい建築手法に対する需要の高まり

- プレハブ建築はエネルギー効率が高く、環境に優しい設計

- 促進要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

- バリューチェーン/サプライチェーン分析

- 政府の規制

- 技術開発

- プレハブ建築業界で使用されるさまざまな構造に関する概要

- プレハブ建築業界のコスト構造分析

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 材料別

- コンクリート

- ガラス

- 金属

- 木材

- その他

- 用途別

- 住宅

- 商業

- 産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- 英国

- スウェーデン

- オランダ

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- インドネシア

- シンガポール

- マレーシア

- その他アジア太平洋

- 世界のその他の地域

- 北米

第6章 競合情勢

- 企業プロファイル

- Sekisui House

- Daiwa House Industry

- Ichijo

- Skyline Champion Corporation

- Morton Buildings Inc.

- Clayton Homes

- Skanska AB

- Barratt Developments PLC

- Persimmon Homes Limited

- China Saite Group Company Limited

- ILKE Homes*

第7章 市場の将来

第8章 付録

The Prefabricated Buildings Market size is estimated at USD 251.01 billion in 2024, and is expected to reach USD 355.18 billion by 2029, growing at a CAGR of 7.19% during the forecast period (2024-2029).

All construction-related operations worldwide stopped due to the COVID-19 pandemic and consequent lockdowns. As a result, modular construction projects in various construction segments, such as educational, residential, airports, and others, had decreased, thus significantly impacting demand for prefabricated buildings. In several places, the supply chain had also been interrupted, thus causing a delay in the delivery of construction material required and affecting the construction activities.

The adoption of additive manufacturing in Europe is expected to significantly boost the prefabricated construction sector. Companies are embracing eco-friendly products and production practices to set themselves apart from the competition. The introduction of energy-absorbing materials such as micro dwellings resulted from the focus on energy efficiency.

Another major factor driving market expansion in the region, particularly in Switzerland, the Nordics, and the United Kingdom, is the introduction of turnkey solutions. Germany, the Nordic countries, and the United Kingdom dominate the prefabricated building industry in Europe.

The United Kingdom is a prospective market for prefabricated building companies. The major players are investing in improved performance and productivity to capitalize on the market's growth potential and modular construction approaches. The existing shortage of skilled labor in the construction industry is a crucial element sustaining the United Kingdom's position in the European prefabricated building industry.

Prefab enterprises have a huge opportunity in India, where there is a need for hundreds or thousands more plants in the future. India is anticipated to be among the fastest-growing countries in terms of construction output over the next few years, making technology a critical component.

India is projected to be the world's second-largest building market in the next five years. A continued government push for digitalization and the adoption of cutting-edge construction technology like BIM is a key driver for the adoption of prefabricated buildings. Government efforts such as "Digital India," "Housing for All," and "Bharatmala Pariyojana" have boosted the use of prefabricated buildings in India.

The value of prefabricated buildings imported into Spain increased significantly in 2022. From 2003 to 2007, the imports of these products increased until they were valued at EUR 101 million(USD 109.78 Million). After that, those imports had a downward trend, reaching EUR 36 million(USD 39.13 Million) in 2012. The prefabricated buildings imported in 2021 into Spain were valued at EUR 65 million(USD 70.65 Million).

Prefabricated Buildings Market Trends

Growing demand for Modular Construction

Due to rapid economic development in developing nations and historically low interest rates in many wealthy nations, there is a rising demand for construction. Along with this, the market is anticipated to rise throughout the forecast period due to factors like rising disposable income, technological advancements, and increased private-sector investments in construction. Additionally, greater spending on housing and infrastructure by governments around the world is boosting market expansion. Time and cost are two factors related to building operations that have long been viewed as a barrier to the industry's expansion in many emerging economies. Overcoming this restriction has been one of the main challenges for many significant building enterprises across the world. The prefabricated building system is one of the primary remedies for these issues.

Prefabricated building technologies can reduce construction time by 30 to 50 percent in today's market and provide an alternative. Since fewer workers are needed for the on-site procedures, the system is economical. Another unintended consequence of the process is reduced on-site activity is the significantly smaller amount of garbage that is generated. Because of these benefits, prefabricated building system activities are growing in popularity in the construction sector.

In nations like Singapore and India, where governments are investing extensively in boosting the building and construction sector, business is booming. The Australian Trade and Investment Commission estimates that Singapore spends at least USD 2 billion a month on public infrastructure. Additionally, the Dutch construction industry is growing thanks to the government's program for a circular economy, which aims to create a circular economy in the country by 2050. Furthermore, due to different government efforts like Foreign Direct Investments, the building and construction industries are also expanding.

Prefabricated building systems are widely employed in the construction of both residential and non-residential structures because they have several advantages, including being environmentally friendly and flexible, causing less site disruption, and cost savings. Therefore, it is anticipated that demand for prefabricated building systems like ventilated thermal panels will expand significantly as construction activity increases globally. As a result, such government initiatives and investments in the building sector serve as a market driver.

Asia-Pacific is Projected to Witness Highest Growth in the Market

The Asia-Pacific prefabricated buildings market is estimated to witness the highest growth over the next five years. The prefabricated construction market in Japan is comparatively mature and developed compared to other regions of the world.

The demand for cheap housing is one of the main factors driving the market. Prefabricated houses can be a practical answer to the issue of a lack of cheap housing in several Asian and Pacific Island nations. Prefabricated structures can be built more rapidly and are typically less expensive than traditional buildings, which can help bring down the cost of construction.

The growth in construction activity is another significant aspect influencing the industry. Recent years have seen significant urbanization in the Asia Pacific region, which has increased construction activity. Residential, commercial, and industrial development projects can all benefit from the utilization of prefabricated buildings.

The inspections by industry-specific trained professionals rather than a general building code have also contributed to the development of the Japanese prefabricated housing market. The concept of prefabrication is gaining prominence in the Indian construction market.

The entry of prefabricated homes in India has paved the way for innovative and technologically advanced construction and design methods for all kinds of construction, such as villas and mass townships.

With the population continuing to decline in Japan combined with an aging population, it is undeniable that the demand for new house construction also decreases. The companies are looking to capture the potential growth in China and other Asian countries as demand for new construction declines in the shrinking domestic market.

Prefabricated Buildings Industry Overview

The major companies in the prefabricated buildings industry are covered in this research. The market is fragmented, but it is likely to grow during the forecast period as prefab construction building investments and upcoming significant projects in various developing and developed countries increase. The major players include Clayton Homes, Sekisui Homes, China Saite Group Company Limited, PEAB, and Barratt Developments PLC.

Due to their efficiency, Prefabricated buildings are being used more and more frequently in recent years. This is not limited to housing either. The prefabricated buildings will also house restaurants, hotels, catering establishments, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMERY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Growing demand for Modular Construction

- 4.2.1.2 Asia-Pacific is Projected to Witness Highest Growth in the Market

- 4.2.2 Restraints

- 4.2.2.1 Lack of awareness and acceptance of of prefabricated buildings among consumers and builders

- 4.2.2.2 Higher transportation and logistics costs associated with the prefabricated buildings

- 4.2.3 Opportunities

- 4.2.3.1 Increasing demand for sustainable and eco-friendly building practices

- 4.2.3.2 Prefabricated buildings can be designed to be energy - efficient and environmentally friendly

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Government Regulations

- 4.6 Technological Developments

- 4.7 Brief on Different Structures Used in the Prefabricated Buildings Industry

- 4.8 Cost Structure Analysis of the Prefabricated Buildings Industry

- 4.9 Impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Material

- 5.1.1 Concrete

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Timber

- 5.1.5 Other Materials

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.3 By Region

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 Italy

- 5.3.2.3 United Kingdom

- 5.3.2.4 Sweden

- 5.3.2.5 Netherlands

- 5.3.2.6 Spain

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Indonesia

- 5.3.3.6 Singapore

- 5.3.3.7 Malaysia

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Sekisui House

- 6.2.2 Daiwa House Industry

- 6.2.3 Ichijo

- 6.2.4 Skyline Champion Corporation

- 6.2.5 Morton Buildings Inc.

- 6.2.6 Clayton Homes

- 6.2.7 Skanska AB

- 6.2.8 Barratt Developments PLC

- 6.2.9 Persimmon Homes Limited

- 6.2.10 China Saite Group Company Limited

- 6.2.11 ILKE Homes*