|

市場調査レポート

商品コード

1906892

欧州のプレハブ建築市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Prefabricated Buildings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のプレハブ建築市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

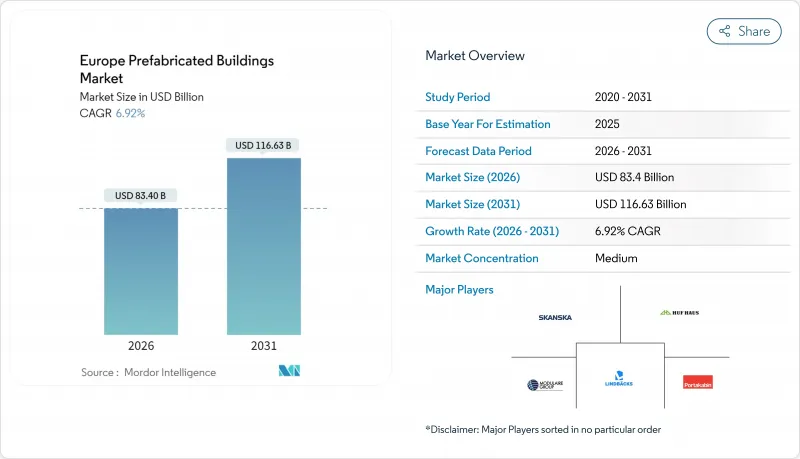

欧州のプレハブ建築市場は、2025年に780億米ドルと評価され、2026年の834億米ドルから2031年までに1,166億3,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは6.92%と見込まれます。

需要の増加は、オフサイト製造が、厳格化する炭素排出規制、拡大するESG資本の流入、工場生産を有利にする慢性的な建設労働力不足といった状況と合致していることを反映しています。欧州全域の指令ではライフサイクル炭素開示が義務付けられており、プレハブメーカーはコンプライアンスと許可取得の迅速化において測定可能な優位性を得ています。

ドイツ、スウェーデン、オランダのデジタル化工場では、予測品質管理と自動組立シーケンスによりサイクルタイムを20~35%短縮しています。同時に、EUタクソノミー規則により木材やその他の低炭素材料を使用するプロジェクト向け低コストグリーンボンドが解放され、大規模モジュラープログラム向け機関投資家資金のプールが拡大しています。こうした要因が相まって、従来の現場施工が建築許可の減少やコスト超過に直面する中でも、欧州のプレハブ建築市場は構造的な成長軌道を維持しております。

欧州プレハブ建築市場の動向と洞察

EUレベルでの炭素排出量上限規制がオフサイト建設を加速

改正建築物エネルギー性能指令の加盟国による実施により、2027年までにすべての新築住宅はライフサイクル炭素を開示することが義務付けられます。デンマークでは2025年7月より、7.1 kg CO2e/m2/年というより厳しい制限が適用されます。工場生産ソリューションは、管理された環境下での資材使用の最適化と廃棄物の循環型回収により、一貫して20~30%低い埋蔵炭素量を達成します。これにより、規制に準拠した製造業者は、計画承認とグリーンファイナンスへの明確な道筋を得られます。2024年施行の建設製品規則で義務付けられるデジタル製品パスポートは、製造過程(クレードル)から出荷時(ゲート)までの排出量が追跡可能な標準化部品をさらに優遇します。そのためプレハブメーカーは、特に自治体が入札書類に炭素上限値を既に組み込んでいるドイツや北欧諸国において、先行者優位の契約を確保すべく、施行スケジュールに先駆けて生産能力を拡大中です。規制の確実性は、次世代のボリューム生産ラインへの投資を支える長期供給契約へとつながっています。

西欧全域における熟練労働者不足の継続

欧州建設業界の空席率は2025年、退職者が新規参入者を上回り、賃金インフレが従来型請負業者の利益率を圧迫したことで10年ぶりの高水準に達しました。プレファブ工法はこの構造的ギャップを解消し、最大90%の作業時間を訓練サイクルが短く安全条件が優れた自動化工場へ移行させます。スウェーデンの工場では既に現場作業班比30%高い労働生産性を達成しており、標準化されたワークフローが人員比率の増加なしに規模拡大を実現する実証例となっています。各国政府は、このモデルを労働市場が逼迫する中でも住宅供給目標を維持する手段と捉えております。ドイツのKfW気候対応新築プログラムが、オフサイト組立比率を実証したプロジェクトに補助金付き融資を結びつけるのもこのためです。したがって、短期的な進展は、雇用主が労働者を従来の湿式工事技能ではなく、デジタル化された工場業務へ再訓練できるかどうかにかかっております。

EU/EEA域内における越境許可の分断

建設製品規則により統一されたCEマーキングとデジタル製品パスポートが導入されましたが、防火安全や耐震基準に関する加盟国の解釈は依然として分かれており、プレハブメーカーは複数の認証セットを保持し、管轄区域ごとにモジュールを再設計せざるを得ません。実施スケジュールは2028年まで延長され、不確実性が長期化し、中小メーカーが償却できない設計コストの増加を招いています。例えば、ドイツの木材接合に関する厳格なDIN規格は、ユーロコードの適応が比較的柔軟なフランスへの輸出時に構造補強コストを増加させます。調和が成熟するまでは、欧州のプレハブ建築市場では並行した設計・試験費用が発生し、利益率の拡大を抑制することになります。

セグメント分析

欧州のプレハブ建築市場シェアは、量産型住宅と多層商業施設の両方に適していることを反映しています。クロスラミネート材(CLT)は高い強度重量比と4時間の耐火性能を提供します。EUタクソノミーは、エンジニアードウッドを「実質的貢献」ステータスへの主要経路と位置付け、生物由来炭素貯蔵を将来の炭素価格変動へのヘッジと捉える年金基金や政府系ファンドを惹きつけています。現在、CLT輸出はスカンジナビアのサプライチェーンが主導していますが、オーストリアとドイツにおける生産能力の増強により、リードタイムのボトルネック解消が図られています。

コンクリートはプレキャスト市場で大きなシェアを占めており、特に駐車場構造物や工業用スラブでは、制御された養生により現場打ちコンクリートに比べて埋込炭素量を削減できます。金属は長スパンのデータセンター外殻や物流ハブにおけるデフォルト材料であり、欧州の鉄鋼生産で90%を超える高いリサイクル率の恩恵を受けています。設計者が耐震性を最適化しつつ炭素メリットを維持するため、木材コアとコンクリートポディウムを組み合わせたハイブリッドシステムが注目を集めています。構造用木材の供給リスクが主な課題であり、認証機関は2024年にCEマーク付きCLTの供給量が12%不足したことを記録しました。これにより、循環性目標を損なわずに材料選択肢を拡大できる補完原料として、積層竹や農業繊維パネルの調査が進められています。

欧州プレハブ建築市場は、材料タイプ(コンクリート、ガラス、金属、木材、その他材料)、用途(住宅、商業施設、その他)、製品タイプ(モジュラー建築、パネル化・コンポーネント化システム、その他プレハブタイプ)、国別(ドイツ、英国、フランス、スペイン、イタリア、オランダ、スウェーデン、デンマーク、ノルウェー、その他欧州諸国)に分類されます。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUレベルでの炭素排出量上限規制がオフサイト建設を加速

- 西欧全域における熟練労働者の慢性的な不足

- 長スパンPEBを必要とするハイパースケールデータセンターの急速な展開

- 加盟国のグリーン・ソーシャル住宅基金は体積単位を優先します

- EUタクソノミー「実質的貢献」ラベルによるグリーンボンド資本の解放(過小報告)

- インダストリー4.0デジタルツイン工場によるサイクルタイムの大幅短縮(過小報告)

- 市場抑制要因

- EU/EEA域内における越境許可制度の分断

- 大型モジュールにおけるラストマイル物流コストの高さ

- 限られたCLT及びLVLの供給量と急速に増加する需要(報告不足)

- EU域内におけるモジュール式移転の付加価値税(VAT)処理の複雑性(報告不足)

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- プレハブ建築物に用いられる様々な構造の概要

- プレハブ建築物のコスト構造分析

第5章 市場規模と成長予測

- 素材タイプ別

- コンクリート

- ガラス

- 金属

- 木材

- その他素材

- 用途別

- 住宅用

- 商業用

- その他

- 製品タイプ別

- モジュラー建築

- パネル化・部品化システム

- その他のプレハブ建築タイプ

- 国別

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- スウェーデン

- デンマーク

- ノルウェー

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Modulaire Group(Algeco Scotsman)

- Bouygues Construction

- Laing O'Rourke

- Skanska AB

- Lindbacks Bygg

- Portakabin Ltd

- Cadolto Modulares Bauen

- CREE GmbH

- Huscompagniet A/S

- Huf Haus

- Danwood S.A.

- Volumetric Building Companies(VBC Europe)

- Harmet OU

- Baufritz GmbH

- Peikko Group

- KOMA Modular

- Secalflor SE

- Leko Labs

- Goldbeck GmbH

- Ballex Metal