バーチャルリアリティ(VR):市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Virtual Reality (VR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1849814

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

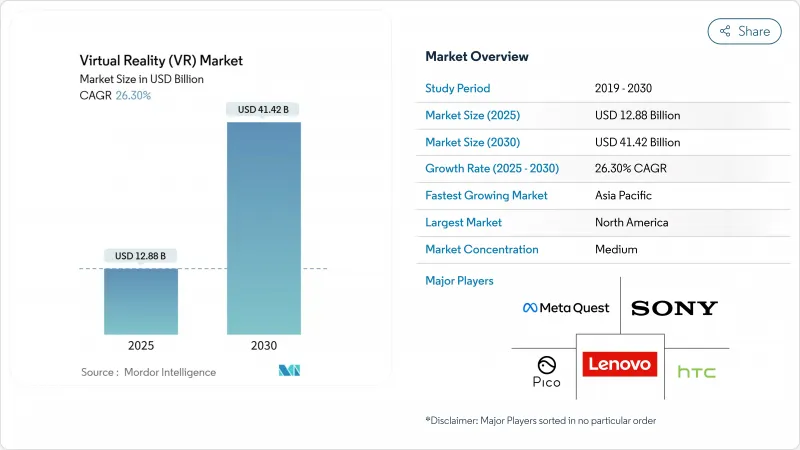

バーチャルリアリティ市場規模は、2025年に128億8,000万米ドルと推定され、2030年にはCAGR 26.30%で成長し、414億2,000万米ドルに達すると予測されます。

没入型トレーニング・プラットフォームの急速な企業採用、ミックスド・リアリティ対応プロセッサの利用可能性の上昇、5Gエッジ・インフラの成熟が、この拡大を下支えしています。企業のネット・ゼロ誓約はバーチャル・ファースト・イベントへの需要を加速させ、治療アプリケーションの規制クリアランスはエンターテインメントを越えて技術の範囲を広げます。ハードウェアの技術革新は引き続き不可欠であるが、企業がテーラーメイドのコンテンツ、堅牢な分析、学習管理システムとのシームレスな統合を優先するにつれて、ソフトウェアとサービスは勢いを増しています。

世界のバーチャルリアリティ(VR)市場の動向と洞察

企業全体でのVRトレーニング導入の増加

各企業は試験的な成功の後、本格的なVRトレーニングプログラムを展開し、従来の方法と比較してトレーニング時間が75%短縮され、学習者の自信が275%向上したことを挙げています。ボーイング社はトレーニング時間を75%削減し、デルタ航空は技術者の熟練度チェックを5,000%向上させました。損益分岐点は375人の受講者で達成され、受講者数が3,000人を超えると、費用対効果は52%向上します。フォーチュン500社の75%以上が現在、ウォルマートの小売シミュレーションや米国陸軍のメンタルヘルス・モジュールを含む学習戦略にVRを組み込んでおり、SOMPOのような日本の保険会社は職場での事故を抑制するためにVR危険シミュレーションを導入しています。その結果、知識はより強固に定着し、現場でのパフォーマンスもより安全になり、トレーニングはバーチャル・リアリティー市場への主要な企業参入口として確固たる地位を築いています。

複合現実対応GPUおよびSoCの主流化

クアルコムのSnapdragon XR2+Gen 2のような次世代チップセットは、1眼あたり4.3Kの解像度を実現し、空間マッピング用に12台のカメラを編成して、ミッドレンジのヘッドセットにフラッグシップの性能をもたらします。アップルのVision Proは、2,300万画素のマイクロOLEDパネルを駆動するためにデュアルチップを採用しており、処理需要曲線を示しています。ディスプレイ部品だけでも単価に530米ドルが上乗せされるため、ダイナミックフォベーテッドレンダリングと視線追跡が効率化には不可欠となります。サムスンとグーグル、クアルコムの3社による提携は、こうしたシリコンの進歩を主流商品化し、価格帯を段階的に引き下げ、バーチャル・リアリティ市場へのアクセスを拡大することを示唆しています。

サイバー酔いと長期的な前庭の懸念

動きと光との不一致は吐き気、頭痛、見当識障害を引き起こし、長時間のセッションを躊躇させる。感覚の不一致に関する調査では、視覚と前庭の不一致が主な原因であると指摘されており、デバイスの揺れが複雑さを増すモバイルVRではその傾向が強まる。医療用ヘッドセットのFDAガイドラインでは、臨床的な重大性を強調し、吐き気の警告を目立つようにすることを義務付けています。ハードウェア・メーカーは、より高いリフレッシュ・レートと待ち時間の短縮を追求しているが、生理的な限界は依然として存在します。企業はより短いモジュールでリスクを軽減するため、コンテンツ設計コストが上昇し、当面のバーチャルリアリティ市場の成長が鈍化します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 企業全体でのVRトレーニング導入の増加

- 「複合現実対応」GPUとSoCの普及

- 5G/エッジを活用したVRコンテンツのアンテザーストリーミング

- 企業のネットゼロ誓約が「バーチャルファースト」イベントを推進

- VRベースのメンタルヘルス療法の規制承認

- コントローラー不要のインタラクションを可能にする超音波触覚

- 市場抑制要因

- サイバーシックネスと長期的な前庭機能障害

- アイボックスの熱蓄積により連続使用が制限される

- ゲーム以外でのAAA級VRコンテンツの不足

- 視線追跡分析におけるデータプライバシーコンプライアンスコスト

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- ライバル関係の激しさ

- マクロ経済要因の評価

第5章 市場規模と成長予測

- 提供別

- ハードウェア

- ソフトウェア

- サービス

- デバイスのフォームファクタ別

- テザーHMD

- スタンドアロンHMD

- スクリーンレスビューア

- CAVE/没入型ルーム

- 没入レベル別

- 非没入型

- 半没入型

- 完全没入型

- エンドユーザー業界別

- ゲーム

- メディアとエンターテイメント

- ヘルスケア

- 教育と訓練

- 軍事と防衛

- 小売業と電子商取引

- 不動産とアーキテクチャ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Meta Platforms(Meta Quest)

- Sony Corporation

- HTC Corporation

- Samsung Electronics Co. Ltd

- Apple Inc.

- Qualcomm Technologies Inc.

- Lenovo Group Ltd

- Pico Interactive Inc.

- Valve Corporation

- Varjo Technologies Oy

- Microsoft Corporation

- Magic Leap Inc.

- Vuzix Corporation

- FOVE Inc.

- DPVR(Lexiang Tech Co. Ltd)

- Unity Technologies Inc.

- Unreal Engine(Epic Games Inc.)

- Autodesk Inc.

- Dassault Systemes SE

- 3D Systems Corporation

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日