|

市場調査レポート

商品コード

1441584

自動車用スーパーチャージャー:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Automotive Supercharger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用スーパーチャージャー:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

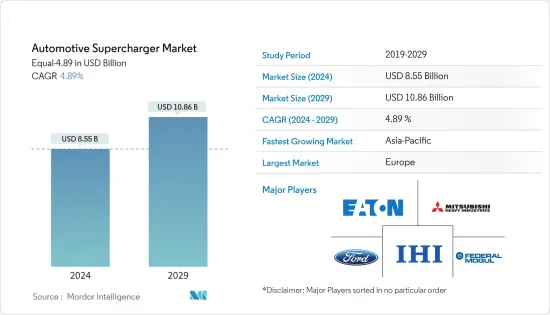

自動車用スーパーチャージャー市場規模は、予測期間(2024年から2029年)中に4.89%のCAGRで、2024年の85億5,000万米ドルから2029年までに108億6,000万米ドルに成長すると予想されます。

長期的には、エンジンに高出力を提供し、効率を向上させるための自動車用スーパーチャージャー技術の強化、および燃料効率が高く軽量なコンポーネントへの需要の高まりが、世界全体の自動車用スーパーチャージャー市場の成長の主要な決定要因となるでしょう。世界。さらに、新エネルギー自動車の導入に向けた政府の積極的な推進により、さまざまな液化石油(LPG)、圧縮天然ガス(CNG)、および水素ベースの自動車が市場に統合され、先進的な自動車の需要にプラスの影響を与えるでしょう。メーカーはこれらの車両モデルに高出力エンジンを組み込むことをますます好むようになるため、スーパーチャージャーシステムも同様です。

欧州自動車工業会(ACEA)によると、2022年に欧州連合に登録された新車のうち36.4%がガソリンベースで、ディーゼルは16.4%を占めました。

しかし、電気自動車は通常の内燃機関を備えていないため、カーボンニュートラル車の利用を求める消費者の嗜好の高まりによる電気自動車の導入の増加が、自動車用スーパーチャージャー市場の成長の大きな阻害要因となっています。それに加え、ガソリンおよびディーゼルベースの自動車を禁止する政府の厳しい規制は、今後数年間でスーパーチャージャーの需要に悪影響を与えると思われます。

たとえば、欧州連合は2023年 3月に、欧州で販売されるすべての新車とバンを2035年までにゼロエミッションにしなければならないという新しい法律を承認しました。

さらに、車両の電動化の進展に伴い、自動車メーカーはそれぞれの生産拠点を閉鎖しています。たとえば、ステランティスは2022年11月、ブラジルのカンポ・ラルゴにあるフィアット・パワートレイン・テクノロジーズ(FPT)エンジン工場の閉鎖を発表したが、これは2038年までにゼロエミッションを達成するという同社の目標のために発表されたものです。

さまざまな自動車メーカーは、バス、ピックアップトラック、バンなどのディーゼル駆動の商用車に幅広く使用できるディーゼルベースのスーパーチャージャーの開発に向けて幅広く戦略を立てています。アジア太平洋地域は、インドや中国などの国で予想されるディーゼル車の販売増加により、予測期間中に自動車用スーパーチャージャーの最も急成長する市場になると予想されています。北米、欧州、アジア太平洋地域は、軽量、高出力、高効率のエンジンを顧客に提供するために常に戦略を立てている大手自動車メーカーの存在と、その後の高級車の需要により、世界の自動車用スーパーチャージャー市場を独占しています。これらの地域では。

自動車用過給機市場動向

乗用車セグメントが予測期間中に市場を独占する

内燃機関(ICE)乗用車が馴染み深いことと、多くの新興国では電気自動車の充電インフラが不足していることが、EVの普及を妨げています。したがって、消費者は依然としてICEを搭載した自動車を利用することを好み、その結果、より高出力でより効率的な自動車を顧客に提供するために、これらの自動車のエンジンシステムにおける絶え間ない革新につながっています。したがって、より高出力の乗用車に対する需要の高まりは、世界中で自動車用スーパーチャージャーの需要の急増に寄与しています。例えば、

2022年、インドの乗用車販売全体に占めるガソリン車の割合は68%に達し、ディーゼル車は市場全体の19%を占めました。同様に、ギリシャでは、2022年の自動車販売全体の71.3%をガソリン車が占め、同期間のディーゼル車は17.42%を占めました。

スーパーチャージャーのメーカーは、軽量で出力が大きく、燃費が高い最もコンパクトな製品を開発することで、競合に先んじようとしています。さらに、これらのメーカーは、車両全体の車両重量を軽減し、排出ガスを削減するために、自社のスーパーチャージャー製品の小型化に常に取り組んでいます。

さらに、高級車の採用増加により高出力エンジンの生産が大幅に増加しており、それがスーパーチャージャーの需要を後押ししています。例えば、BMW、メルセデスベンツ、アウディなどの高級ブランドの販売台数は、2022年にそれぞれ240万台、207万台、161万台に達しました。エンジンメーカーは、需要の高まりに対応するためにビジネスの可能性を拡大しています。地域全体のガソリン車とディーゼル車の販売。例えば:

2022年11月、フランスの自動車大手ルノー・グループは、長期ビジョンの中でICエンジンの生産に注力する計画について議論しました。同社は、今後のマイルドハイブリッド車およびICエンジン車向けの生産ユニットの設立、パワートレイン、ICエンジンの供給について、拘束力のない枠組み契約を吉利控股有限公司と締結しました。

トヨタは2022年4月、ハイブリッド電気自動車を含む4気筒エンジンの生産を支援するため、米国の4つの製造工場に3億8,300万米ドルを投資すると発表しました。さらに、アラバマトヨタのハンツビル工場は、114,000平方フィートの敷地を拡張し、内燃およびハイブリッド電気パワートレイン用のエンジンを生産するための新しい4気筒生産ラインを設置するために2億2,200万米ドルを受け取った。

エンジン技術の急速な向上とアフターマーケットでの需要の高まりにより、予測期間中に自動車用スーパーチャージャーに対する膨大な需要が存在すると予想されます。

アジア太平洋地域は予測期間中に最も急成長する市場となる

アジア太平洋は、中国、インド、日本などの主要な自動車ハブの存在により、世界で販売される車両のほぼ50%がこの地域で生産されており、最も急速に成長する市場になると予想されており、アジア太平洋地域ではさらに成長が見込まれています。今後数年。エンジンの高出力化へのニーズは年々高まっています。アジアでは、エンジンのダウンサイジングへの傾向が変化しており、V6にスーパーチャージャーを装備した方が、V8エンジンを搭載した車両より効率的であることが判明しています。

さらに、アジア太平洋地域では自動車の販売が目覚ましく、エンジン全体とそれに続くスーパーチャージャーの需要がプラスの方向に向かっています。例えば:

中国汽車工業協会(CAAM)によると、2023年10月の乗用車総販売台数は24万8,800台に達し、2022年の同時期と比較して前年比11.4%増加しました。その後、2023年1月から10月までの乗用車総販売台数は206万6,400台に達し、2022年の同時期と比較して前年比7.5%の成長を記録しました。

同様に、インドの乗用車販売台数は、2022年10月の29万1,113台に対し、2023年10月には34万1,377台に達し、前年比17.2%の伸びを示しました。同時に、日本自動車販売協会連合会と全国軽自動車二輪車協会によると、2023年10月の排気量660cc以上の販売台数は前年比14.9%増の24万3,144台、排気量660cc未満の車は4.7%増の15万4,528台となった。前の月。

OEMは、高トルクとパフォーマンスを得るために技術的に先進的なエンジンの開発に注力しており、これらの車両に先進的なスーパーチャージャーを統合することで対応しています。多燃料エンジン技術の出現は、予測期間中にアジア太平洋地域全体の自動車用スーパーチャージャー市場の積極的なプレーヤーに有利な機会を提供すると予想されます。

自動車用スーパーチャージャー業界の概要

自動車用スーパーチャージャー市場は、エコシステム内で活動するさまざまな国際的および地域的プレーヤーの存在により、細分化されており、非常に競争が激しいです。企業は、スーパーチャージャーの分野における継続的な製品革新のため、研究開発活動に多額の投資を積極的に行っています。例えば、2023年12月、テキサスに本拠を置くハイパーカーメーカーで高性能車の開発会社であるヘネシーは、ゼネラルモーターズのV8エンジンを搭載したピックアップトラックの包括的なアップグレードを発表しました。このアップグレードにはスーパーチャージャーが統合され、最高出力650馬力、最高出力658ポンドフィートを実現する予定です。トルク。さらに同社は、スーパーチャージャーが既存のシエラとシルバラードの6.2リッターV8(L87 EcoTec3)ラインナップからアップグレードされており、純正比で馬力を55%向上させることができると述べた。

2023年7月、Whipple Superchargersは6.6リッター(L8T)V8エンジン用の3.0リッタースーパーチャージャーシステムの発売を発表しました。このV8ガスエンジンは、ストック形式で401馬力と464ポンドフィートのトルクを発生し、GMCシエラ2500 HDや3500 HDなどのゼネラルモーターズのヘビーデューティピックアップに標準装備されています。さらに同社は、新開発のスーパーチャージャーはトルクをさらに236 lb-ft増加させ、合計700ポンド増加させる能力があると述べた。

これらのプレーヤーが業界での競争力を獲得しようとしているため、市場では先進的なディーゼルスーパーチャージャー技術の急速な強化と発売が見込まれると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場の成長を促進する高級車の需要の増加

- 市場抑制要因

- 電気自動車の普及が市場の成長を妨げる

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額ベースの市場規模)

- テクノロジー別

- 遠心式スーパーチャージャー

- ルーツスーパーチャージャー

- ツインスクリュースーパーチャージャー

- 燃料タイプ別

- ガソリン

- ディーゼル

- 電源別

- エンジン駆動

- 電動モーター駆動

- 販売チャネル別

- 相手先商標製品製造業者(OEM)

- アフターマーケット

- 車種別

- 乗用車

- 商用車

- 地域別

- 北米

- 米国

- カナダ

- 北米のその他の地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Ferarri NV

- Eaton Corporation PLC

- Mitsubishi Heavy Industries Ltd.

- Koenigsegg Automotive AB

- Honeywell Inc.

- IHI Corporation

- Vortech Engineering

- Federal-Mogul Corporation

- A&A Corvette

- Rotrex A/S

- Aeristech

- Daimler AG

- Ford Motor Company

第7章 市場機会と将来の動向

- ディーゼルスーパーチャージャー技術の急速な向上により市場の需要が拡大

The Automotive Supercharger Market size in terms of Equal-4.89 is expected to grow from USD 8.55 billion in 2024 to USD 10.86 billion by 2029, at a CAGR of 4.89% during the forecast period (2024-2029).

Over the long term, the enhancement in the automotive supercharger technology to provide higher-power output to engines, better efficiency, and the growing demand for fuel-efficient and lightweight components will serve as major determinants for the growth of the automotive supercharger market across the world. Further, the government's aggressive push towards the adoption of new-energy vehicles will witness the integration of various liquefied petroleum (LPG), compressed natural gas (CNG), and hydrogen-based vehicles in the market, which will positively impact the demand for advanced supercharger systems, as manufacturers will increasingly prefer to integrate high powered engines in these vehicle models.

According to the European Automobile Manufacturers' Association (ACEA), 36.4% of all new cars registered in the European Union were petrol-based, while diesel accounted for 16.4% of registrations in 2022.

However, the rising adoption of electric vehicles, owing to the increasing consumers' preference towards availing carbon-neutral vehicles, is serving as a major deterrent to the growth of the automotive supercharger market, as electric vehicles do not possess regular internal combustion engines. Coupled with that, strict government regulations to ban petrol and diesel-based cars will negatively impact the demand for superchargers in the coming years.

For instance, in March 2023, the European Union approved a new law requiring that all new cars and vans sold in Europe must be zero-emission by 2035.

Moreover, with the rising electrification of vehicle fleets, automakers are shutting down their respective production bases. For instance, In November 2022, Stellantis announced the closure of its Fiat Powertrain Technologies (FPT) engine plant in Campo Largo, Brazil, which was announced due to the company's aim to achieve zero emissions by 2038.

Various automakers are extensively strategizing to pivot towards the development of diesel-based superchargers as they can be extensively used in diesel-operated commercial vehicles such as buses, pickup trucks, and vans, among others. The Asia-Pacific region is anticipated to become the fastest-growing market for automotive superchargers during the forecast period, owing to the increasing diesel vehicle sales expected in countries such as India and China. North America, Europe, and Asia-Pacific regions dominate the global automotive supercharger market due to the presence of leading automakers in these regions which are constantly strategizing to offer lightweight, high-power, and efficient engines to customers and the subsequent demand for luxury vehicles in these regions.

Automotive Supercharger Market Trends

Passengers Cars Segment to Dominate the Market during the Forecast Period

The familiarity with internal combustion engine (ICE) passenger cars and the lack of electric vehicle charging infrastructure in many emerging countries hampers the penetration of EVs. Hence, consumers still prefer availing of ICE-powered cars, which in turn leads to constant innovations in the engine systems of these vehicles to offer higher-powered and more efficient vehicles to customers. Therefore, the increasing demand for higher-powered passenger cars contributes to the surging demand for automotive superchargers across the world. For instance,

In 2022, the share of petrol cars in the overall passenger car sales in India touched 68%, while diesel cars accounted for 19% of the overall sales in the market. Similarly, in Greece, sales of petrol cars accounted for 71.3% of the overall car sales in 2022, while diesel-operated cars accounted for 17.42% during the same period.

Supercharger manufacturers try to stay ahead of the competition by building the most compact products that are lightweight, have greater power output, and have a higher fuel economy. Moreover, these manufacturers are constantly working towards downsizing their supercharger offerings to assist in decreasing the overall curb weight of the vehicle and reducing emissions.

Furthermore, the production of high-powered engines is witnessing a massive surge due to the increasing adoption of luxury vehicles, which, in turn, assists the demand for superchargers. For instance, sales of luxury brands, such as BMW, Mercedes-Benz, and Audi, touched 2.4 million units, 2.07 million units, and 1.61 million units, respectively, in 2022. Engine manufacturers are expanding their business potential to meet the rising demand for gasoline and diesel vehicle sales across the geography. For instance:

In November 2022, French automotive giant Renault Groupe discussed its plans to focus on producing IC engines during its longer-term vision. The company has signed a non-binding framework agreement with GeelyHoldings for establishing production units, supply power trains, and IC engines for upcoming mild hybrid and IC engine vehicles.

In April 2022, Toyota announced an investment of USD 383 million in four of its US manufacturing plants to support the production of its four-cylinder engines, including hybrid electric vehicles. In addition, Toyota Alabama in Huntsville plant received USD 222 million to expand 114,000 sq ft and install a new four-cylinder production line to produce engines for both combustion and hybrid electric powertrains.

With the rapid enhancement in engine technology and the rising demand in the aftermarket, there will exist a massive demand for automotive superchargers during the forecast period.

Asia-Pacific Region to become the Fastest Growing Market during the Forecast Period

Asia-Pacific is expected to become the fastest-growing market, as almost 50% of the vehicles sold globally are from this region due to the presence of major automotive hubs like China, India, and Japan, which is further anticipated to grow in the coming years. The need for higher-powered engines has been increasing year-on-year. Asia has witnessed a change in the trend toward downsizing engines, wherein equipping a V6 with a supercharger is found to be more efficient than equipping a vehicle with a V8 engine.

Further, the Asia-Pacific region is witnessing impressive vehicle sales, which have taken the overall engine and, subsequently, supercharger demand on the positive side. For instance:

According to the China Association of Automobile Manufacturers (CAAM), total passenger car sales in October 2023 touched 248.8 thousand units, showcasing a Y-o-Y growth of 11.4% compared to the same period in 2022. Subsequently, total passenger car sales between January and October 2023 touched 2,066.4 thousand units, witnessing a Y-o-Y growth of 7.5% compared to the same period in 2022.

Similarly, passenger car sales in India touched 341,377 units in October 2023, compared to 291,113 units in October 2022, representing a Y-o-Y growth of 17.2%. Simultaneously, according to the Japan Automotive Dealers Association and Japan Light Motor Vehicle and Motorcycle Association, in October 2023, sales with engine displacements above 660cc increased 14.9% to 243,144 units, while vehicles with engine displacements below 660cc increased 4.7% to 154,528 units compared to the previous month.

OEMs have been focusing on developing technologically advanced powered engines to gain high torque and performance, which is being catered to by integrating advanced superchargers in these vehicles. The emergence of multi-fuel engine technology is expected to provide lucrative opportunities to the active players in the automotive supercharger market across the Asia-Pacific region during the forecast period.

Automotive Supercharger Industry Overview

The automotive supercharger market is fragmented and highly competitive due to the presence of various international and regional players operating in the ecosystem. Some of the major players include Eaton Corporation PLC, Mitsubishi Heavy Industries Ltd., IHI Corporation, Federal-Mogul Corporation, Ford Motor Company, Honeywell Inc., Vortech Engineering, Aeristech, and Daimler AG, among others. These players are actively engaged in investing hefty sums in their R&D activity for constant product innovation in the realm of superchargers. For instance, in December 2023, Hennessey, the Texas-based hypercar manufacturer and high-performance vehicle creator announced comprehensive upgrades for General Motor's V8-powered pickup trucks, which will be integrated with a supercharger to deliver 650 bhp and 658 lb-ft of torque. Further, the company stated that its supercharger is upgraded from its existing Sierra and Silverado's 6.2-liter V8 (L87 EcoTec3) lineup, which can increase horsepower over stock by 55%.

In July 2023, Whipple Superchargers announced that the launch of its 3.0-liter supercharger system for the 6.6-liter (L8T) V8 engine. This V8 gas engine produces 401 horsepower and 464 lb-ft of torque in stock form and is standard fitment on General Motors' Heavy Duty pickups like the GMC Sierra 2500 HD and 3500 HD. Further, the company stated that the newly developed supercharger has the capability of boosting the torque by an additional 236 lb-ft for a total of 700.

The market is anticipated to witness a rapid enhancement and launch of advanced diesel supercharger technology as these players try to gain a competitive edge in the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Luxury Vehicles to Foster the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 Rising Adoption of Electric Vehicles Deter Market Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Technology

- 5.1.1 Centrifugal Supercharger

- 5.1.2 Roots Supercharger

- 5.1.3 Twin-Screw Supercharger

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.3 By Power Source

- 5.3.1 Engine Driven

- 5.3.2 Electric Motor Driven

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicles

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Ferarri N.V.

- 6.2.2 Eaton Corporation PLC

- 6.2.3 Mitsubishi Heavy Industries Ltd.

- 6.2.4 Koenigsegg Automotive AB

- 6.2.5 Honeywell Inc.

- 6.2.6 IHI Corporation

- 6.2.7 Vortech Engineering

- 6.2.8 Federal-Mogul Corporation

- 6.2.9 A&A Corvette

- 6.2.10 Rotrex A/S

- 6.2.11 Aeristech

- 6.2.12 Daimler AG

- 6.2.13 Ford Motor Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Enhancement in Diesel Supercharger Technology Fuels the Market Demand