|

市場調査レポート

商品コード

1692538

ワイヤレス接続チップセット:市場シェア分析、産業動向、成長予測(2025~2030年)Wireless Connectivity Chipset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワイヤレス接続チップセット:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 153 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

ワイヤレス接続チップセット市場規模は2025年に92億3,000万米ドル、2030年には137億9,000万米ドルに達すると予測、予測期間(2025~2030年)のCAGRは8.36%。

主要ハイライト

- 高速インターネットの普及に伴い、コネクテッドデバイスやスマートホーム用途の採用が、特に欧州、北米、アジア太平洋などの地域で増加しています。主要ソリューションには、音声アシスタント、スマートサーモスタット、スマート照明、防犯カメラ、スマート民生用電子機器などがあります。

- さらに、2024年5月、MediaTekは、強力な性能と、複数の業種にわたる最新のAI機能強化をサポートする2つの新しいチップセットのデビューを発表しました。これには、プレミアムChromebook向けのKompanio 838 SoCと、4KプレミアムスマートTVとディスプレイ向けのPentonic 800 SoCが含まれます。同社は、AI、自動車、IoT、テレビ、Chromebook、ワイヤレス接続などの製品カテゴリーにおける主要な開発を強調しました。

- 例えば、6G技術の研究開発を加速させるため、IMT~2030年(6G)推進グループが中国で結成されました。2030年頃には、世界中で6Gの商用化が始まると予想されています。中国は5Gの商用化を率先して支援しており、これは6G開発の確かな基礎となります。

- IoTのように複数のデバイスを追加すると、ネットワークの表面積が増大し、その過程で潜在的な攻撃ベクトルが増えます。ネットワークに接続された1台の安全でないデバイスでさえ、ネットワークに対する能動的な攻撃の入口となる可能性があります。

- 経済協力開発機構(OECD)の調査によると、2025年までにコンピュータのある世帯数は12億6,247万世帯に増加すると予想されています。少なくとも1台のコンピューターがある家庭はコンピューター世帯と呼ばれます。このようなコンピュータ普及の大幅な促進は、市場参入企業がWi-Fiチップセット製品ポートフォリオを拡大し、さまざまな地域でのプレゼンスを拡大し、市場シェアを拡大する機会を創出します。

- 市場のさまざまな参入企業が競合を維持するために新製品を開発しており、これが市場成長をさらに促進する可能性があります。例えば、Wi-Fi 7技術の早期パイオニアであるMediaTekは、2023年11月、最新の製品であるFilogic 860とFilogic 360を発表し、市場リーダーとしての地位を固めました。これらの追加製品は、優れた性能と揺るぎない信頼性を実現する最新の接続技術を重視し、MediaTekの最先端製品ラインを大幅に拡大しました。

- Filogic 860チップセットは、デュアルバンドアクセスポイントと先進的ネットワークプロセッサを搭載し、企業向けアクセスポイント、サービスプロバイダゲートウェイ、メッシュノード、各種小売とIoTルーター向けに調整されています。一方、Filogic 360は、1チップでWi-Fi 7 2x2機能とデュアルBluetooth 5.4無線を実現しています。この設計は、次世代Wi-Fi 7接続をエッジ機器やストリーミング機器、幅広い民生用電子機器製品に提供するために特別に設計されています。

- 先進的なWi-Fiチップセットの開発と製造に関連する高コストは、市場に大きな課題をもたらしています。これらのチップセットの製造に必要な高度で高価な技術は、最終製品のコストを上昇させ、特に価格に敏感な消費者の間での採用を妨げる可能性があります。

- COVID-19以降、関連する会議やディスカッションにはデジタルモードを選択する一方で、コラボレーションツールの採用により重点を置くようにシフトしています。さらに、学校教育や在宅勤務の増加をサポートする必要性など、5Gの新たな使用事例が5G投資を促進すると予想されます。さらに、多くの職場がハイブリッド型勤務モデルを採用しており、5G接続を導入することで接続性を高めることができます。このようなケースは、サプライチェーンの不足による混乱にもかかわらず、市場を積極的に牽引しています。

無線接続チップセット市場動向

Wi-Fiスタンドアロンが市場の最大シェアを占める

- Wi-Fiネットワーク技術の進化により、ユーザーはより高速で低遅延な通信を体験できるようになりました。これにより、データ量の多いサービスや用途の利用が促進されました。Wi-Fiネットワークで伝送されるデータ量の大幅な増加は、主にビデオに対する顧客の需要や、ビジネスと消費者のクラウドサービスへの移行によってもたらされています。この要因により、高速・大容量ネットワークを備えたワイヤレス5G接続のニーズが高まると予想されます。

- 現代世界ではインターネットの普及が拡大しています。国際通信連合によると、2023年時点で世界のインターネットユーザー数は54億人と推定され、前年の51億人から増加しました。このシェアは世界人口の67%に相当します。

- Snapchatのレポートによると、2025年までに世界人口の約75%、スマートフォンユーザーのほぼ全員がAR技術を頻繁に利用するようになり、そのうち15億人以上がミレニアル世代になると予想されています。GSMAのMobile Economy Chinaによると、中国では2025年までに約3億4,000万台のスマートフォン接続が増加し、普及率は10接続のうち9接続、中国本土で15億台、香港で1,230万台、マカオで190万台、台湾で2,570万台に達します。

- 2024年2月、韓国企業のステージXは、国内第4のモバイルキャリアとなる周波数帯を獲得し、2025年前半に全国規模のモバイルネットワークサービスを開始する予定であると発表しました。同社は4億6,200万米ドル(6,128億ウォン)を投資し、6,000の基地局を建設する計画で、28GHzの5Gネットワークを韓国全土に展開します。

- Ericsson Mobility Reportによると、北米におけるモバイルデータの月間平均使用量は、2026年にはスマートフォンで月間49GBに達すると予想されています。スマートフォンに精通した消費者層、ビデオリッチな用途、大容量データプランがトラフィックの伸びを促進します。スマートフォン1台当たりのトラフィックは短期的には堅調に伸びるかもしれないが、ARやVRを活用した没入型のコンシューマー向け5G接続の採用により、長期的にはさらに高い成長率が見込まれます。

- また、低遅延化により、グリッチや遅延のない高速の仮想現実や拡張現実の映像が実現する態勢が整っています。モバイル接続は、スモールセルインフラによって強化され、5Gワイヤレス信号を高密度化し、コンクリートの建物や壁を通る動きを改善することができます。また、スモールセルアンテナは無線接続を強化し、同じネットワーク上でより多くのデバイスを同時にサポートします。このような開発が市場を牽引すると予想されます。

アジア太平洋が最も急成長する市場になる見込み

- アジア太平洋における5Gの登場は、高速ネットワーク接続のための無線接続チップセットの展開を加速させました。日本政府は全国20万8,000基の信号機に5G基地局を設置する許可を与えました。地方自治体と通信事業者は、5G配備のために信号機を使用する費用を分担しました。これにより、より短時間でより多くのソリューションが展開され、5G接続性がより早く全国に行き渡ることになります。

- ビジュのような様々なインドの多国籍教育技術企業は、教育カリキュラムの一環として生徒にタブレットを提供し、伝統的教育方法とともにデジタル手法で生徒を教育しています。同市場における企業のこうした取り組みは、タブレット、スマートフォン、その他の民生用電子機器製品の需要をさらに促進し、予測期間中、同地域のタブレット用無線接続チップセット市場を牽引すると予想されます。

- また、アジア太平洋におけるインターネットサービスの需要増加も、同地域における無線接続チップセットの採用を促進すると予想されます。インド首相によると、インドにおける5Gインターネットサービスの開始は、国家に新たな経済的可能性と社会的利益をもたらすと期待されています。

- さらに、中国は世界規模で5G開発をリードしています。全国で254万以上の5G基地局が建設され、5億7,500万人以上が5Gスマートフォンを所有しています。同国はさらに、2025年までに5Gネットワーク建設に1兆2,000億人民元(1,742億米ドル)を投資する計画です。このような5Gの安定したネットワークに対する需要の高まりは、同国におけるスモールセルソリューションの展開を加速させています。

- 5Gスマートフォンが入手しやすくなり、価格も手頃になり、大都市圏や農村部でのスマートフォンの普及が急速に進んでいることから、5Gの契約数は急速に増加し、2023年末までに同地域で約5,000万件に達すると予想されます。

- 2023年2月、シンガポールのネットワーク事業者M1とStarHubは、Antinaと名付けられたアライアンスを結成しました。両社はNokiaとの契約を延長し、全国で屋内と屋外の5Gカバレッジを向上させました。Nokiaは、高帯域幅、猛烈なスピード、最小限の待ち時間でより良い5Gユーザー体験を提供するため、ASiR(Air Scale Indoor Radio)と呼ばれるスモールセルソリューションを設置し、MIMO(Multiple Input, Multiple Outputs)適応型アンテナで新しい建物をカバーします。

ワイヤレス接続チップセット産業概要

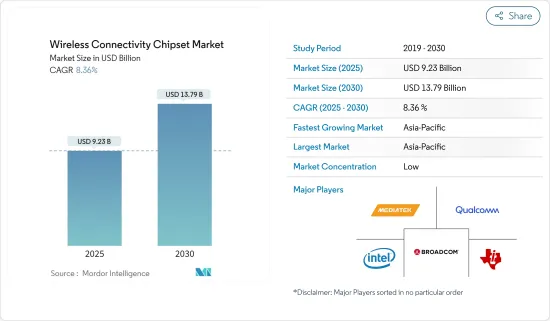

ワイヤレス接続チップセット市場は細分化されており、Broadcom Inc.、Qualcomm Incorporated、Mediatek Inc.、Intel Corporation、Texas Instruments Incorporatedなど多くの企業が参入しています。また、各社は新製品の投入、事業の拡大、戦略的合併、提携、買収を行うことで、市場での存在感を高めています。

- 2023年6月:Broadcomは第2世代Wi-Fi 7チップセットを発表しました。住宅用 Wi-Fi 7アクセスポイントチップのBCM6765、Bluetooth Low Energy(BLE)、Zigbee、Thread、Matterプロトコルの動作をサポートするデュアルIoT無線を搭載した企業向けWi-Fi 7アクセスポイントチップのBCM47722、モバイルデバイス用に設計された低電力Wi-Fi 7、Bluetooth、802.15.4コンボチップのBCM4390です。BCM47722エンタープライズWi-Fi 7アクセスポイントSoC仕様は、無線接続を可能にします。

- 2023年4月:Texas Instrumentsは、Wi-Fi 6コンパニオン集積回路(IC)のラインアップである最新のSimpleLinkファミリーを発表しました。これらのICは、設計者が堅牢で安全かつ効率的なWi-Fi接続を実現できるように設計されており、特に高密度または105 °Cに達する高温環境での用途に最適です。TIのCC33xxファミリーの最初の製品は、Wi-Fi 6とBluetooth Low Energy 5.3の両方に対応し、すべて1つのICで実現します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- マクロ経済動向の市場への影響評価

第5章 市場力学

- 市場の促進要因

- ホームオートメーションによるコネクテッドホーム需要の増加

- 家庭や企業へのインターネット普及率の増加

- 市場課題

- データのセキュリティとプライバシー、デバイスの接続性と相互運用性に関する問題

- 一部の携帯端末の需要低迷

第6章 市場セグメンテーション

- タイプ別

- Wi-Fiスタンドアロン

- Bluetoothスタンドアロン

- WifiとBluetoothコンボ

- 低消費電力ワイヤレスIC

- エンドユーザー用途別

- コンシューマー

- エンタープライズ

- 携帯端末

- 自動車

- 産業用

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Broadcom Inc.

- Qualcomm Incorporated

- Mediatek Inc.

- Intel Corporation

- Texas Instruments Incorporated

- STMicroelectronics NV

- NXP Semiconductors NV

- On Semiconductor Corporation

- Infineon Technologies AG

- Microchip Technology Inc.

- Qorvo Inc.

- Skyworks Solutions Inc.

- Hisilicon Technologies Co. Ltd

- Tsinghua Unigroup Co. Ltd(unisoc(Shanghai)Technologies Co. Ltd)

第8章 ベンダーの市場シェア分析

第9章 投資分析

第10章 投資分析市場の将来

The Wireless Connectivity Chipset Market size is estimated at USD 9.23 billion in 2025, and is expected to reach USD 13.79 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

Key Highlights

- With the growing penetration of high-speed internet, the adoption of connected devices and smart home applications is increasing, especially in regions such as Europe, North America, and Asia-Pacific. Some major solutions include voice assistants, smart thermostats, smart lighting, security cameras, and smart appliances.

- Further, in May 2024, MediaTek announced the debut of two new chipsets with powerful performance and support for the latest AI enhancements across multiple verticals. These included the Kompanio 838 SoC for premium Chromebooks and the Pentonic 800 SoC for 4K premium smart TVs and displays. The company highlighted major developments in product categories such as AI, automotive, IoT, TVs, Chromebooks, and wireless connectivity.

- For instance, the IMT-2030 (6G) Promotion Group was formed in China to speed up the R&D of 6G technology. Around 2030, the world is anticipated to witness the commercialization of 6G. China is leading the charge in supporting the commercialization of 5G, which will provide a solid basis for developing 6G.

- Adding several devices, such as in IoT, increases the surface area of a network, creating more potential attack vectors in the process. Even a single unsecured device connected to a network may serve as a point of entry for an active attack on the network.

- According to the Organisation for Economic Co-operation and Development survey, by 2025, the number of households with computers is anticipated to increase to 1,262.47 million. Homes with at least one computer are referred to as computer households. Such a massive boost in computer adoption will create an opportunity for the market players to expand their Wi-Fi chipset product portfolio, expand their presence in different regions, and advance their market share.

- Various players in the market are developing new products to stay competitive, which may further propel market growth. For instance, in November 2023, MediaTek, an early pioneer in Wi-Fi 7 technology, solidified its position as a market leader with the launch of its latest offerings, the Filogic 860 and Filogic 360. These additions significantly expanded MediaTek's cutting-edge product line, emphasizing the latest connectivity technologies for superior performance and unwavering reliability.

- The Filogic 860 chipsets, featuring a dual-band access point and an advanced network processor, are tailored for enterprise access points, service provider gateways, mesh nodes, and various retail and IoT router applications. On the other hand, the Filogic 360 facilitates Wi-Fi 7 2x2 capabilities and dual Bluetooth 5.4 radios in a single chip. This design is specifically crafted to bring next-gen Wi-Fi 7 connectivity to edge and streaming devices, as well as a wide range of consumer electronics.

- High costs associated with developing and producing advanced Wi-Fi chipsets pose a significant challenge in the market. The sophisticated and expensive technology needed for manufacturing these chipsets inflates the final product's cost, potentially hindering adoption, especially among price-sensitive consumers.

- Post-COVID-19, there was a shift to opting for digital modes for relevant meetings and discussions while focusing more on adopting collaborative tools. Furthermore, emerging use cases for 5G, including the need to support increasing numbers of individuals schooling and working from home, are expected to drive 5G investment. In addition, many workplaces have adopted a hybrid model of working, for which 5G connections can be deployed for better connectivity. Such cases have positively driven the market despite the disruptions caused due to shortages in the supply chain.

Wireless Connectivity Chipset Market Trends

Wi-Fi Standalone Holds the Maximum Share of the Market

- The evolution of Wi-Fi network technology allows users to experience faster speeds and lower latency. It boosted the use of data-heavy services and applications. The significant rise in the volume of data carried by Wi-Fi networks has been primarily driven by customer demand for video and business and consumer moves to cloud services. This factor is expected to drive the need for a wireless 5G connection with fast and high-capacity networks.

- Internet penetration has scaled up in the modern world. According to the International Telecommunication Union, as of 2023, the estimated number of internet users worldwide was 5.4 billion, up from 5.1 billion in the previous year. This share represented 67% of the global population.

- According to a report from Snapchat, by 2025, around 75% of the global population and almost all smartphone users will be frequent AR technology users, out of which more than 1.5 billion are anticipated to be millennials. According to GSMA's Mobile Economy China, China will add around 340 million smartphone connections by 2025, with adoption rising to 9 in 10 connections, 1.5 billion in Mainland China, 12.3 million in Hong Kong, 1.9 million in Macao, and 25.7 million in Taiwan.

- In February 2024, Stage X, a South Korean company, announced that it was awarded a spectrum that will enable it to be the nation's fourth mobile carrier and planned to launch nationwide mobile network services in the first half of 2025. The company invested USD 462 million (KRW 612.8 billion) to deploy its 28 GHz 5G network across South Korea with a plan to build 6,000 base stations; it also involved the mandated installation standard for the 28 GHz frequency network.

- According to Ericsson's Mobility Report, the monthly average usage of mobile data in North America is expected to reach 49 GB per month for smartphones in 2026. A smartphone-savvy consumer base, video-rich applications, and large data plans will drive traffic growth. While there may be robust growth in traffic per smartphone in the near term, the adoption of immersive consumer 5G connections utilizing AR and VR is expected to lead to an even better growth rate in the long term.

- Lower latency is also poised to enable high-speed virtual and augmented reality video without glitches or delays. Mobile connectivity can be strengthened with small cell infrastructure, densifying 5G wireless signals and improving their movement through concrete buildings and walls. Small-cell antennas will also enhance wireless connection, supporting more devices on the same network simultaneously. Such developments are expected to drive the market.

Asia-Pacific is Expected to be the Fastest-growing Market

- The advent of 5G in the Asia-Pacific region accelerated wireless connectivity chipset deployment for high-speed network connectivity. Japan's government granted permission to install 5G base stations on 208,000 traffic lights across the country. Local administrations and operators shared the costs of using the traffic lights for 5G deployments. This will help with more solution deployment in less time, thereby circulating 5G connectivity faster throughout the country.

- Various Indian multinational educational technology companies, such as Byju's, provide their students with a tablet as a part of their educational curriculum to educate the students via digital methods along with the traditional methods of teaching. Such initiatives by the companies in the market are expected to promote further the demand for tablets, smartphones, and other consumer electronics in the market, thereby driving the market for wireless connectivity chipsets for tablets in the region during the forecast period.

- The increasing demand for internet services in the Asia-Pacific region is also expected to promote the adoption of wireless connectivity chipsets in the region. As per the prime minister of India, the launch of 5G internet services in India is expected to bring new economic possibilities and societal benefits to the nation.

- In addition, China is leading 5G development on a worldwide scale. More than 2.54 million 5G base stations have been built nationwide, and more than 575 million people now own 5G smartphones. The country further plans to invest CNY 1.2 trillion (USD 174.2 billion) in 5G network construction by 2025. This growing demand for a 5G stable network is accelerating the deployment of small-cell solutions in the country.

- Due to the increasing availability and affordability of 5G smartphones and the rapid adoption of smartphones in metropolitan and rural areas, 5G subscriptions are expected to rapidly increase to reach approximately 50 million in the region by the end of 2023.

- In February 2023, Network operators M1 and StarHub in Singapore formed an alliance named Antina. They extended their contract with Nokia to improve indoor and outdoor 5G coverage nationwide. To provide a better 5G user experience with high bandwidth, breakneck speeds, and minimal latency, Nokia will install its small cell solution called airscale indoor radio (ASiR), covering new buildings with multiple input, multiple outputs (MIMO) adaptive antennas.

Wireless Connectivity Chipset Industry Overview

The wireless connectivity chipset market is fragmented, with many players like Broadcom Inc., Qualcomm Incorporated, Mediatek Inc., Intel Corporation, and Texas Instruments Incorporated. The companies are also increasing their market presence by introducing new products, expanding their operations, and entering strategic mergers, partnerships, and acquisitions.

- June 2023: Broadcom unveiled its second-generation Wi-Fi 7 chipsets: the BCM6765 residential Wi-Fi 7 access point chip, the BCM47722 enterprise Wi-Fi 7 access point chip with dual IoT radios that support operation for Bluetooth Low Energy (BLE), Zigbee, Thread, and Matter protocols, and the BCM4390 low-power Wi-Fi 7, Bluetooth, and 802.15.4 combo chip designed for use in mobile devices. BCM47722 enterprise Wi-Fi 7 access point SoC specifications allow wireless connectivity.

- April 2023: Texas Instruments unveiled its latest SimpleLink family, a line of Wi-Fi 6 companion integrated circuits (ICs). These ICs are designed to empower designers to create robust, secure, and efficient Wi-Fi connections, particularly for applications in high-density or high-temperature settings, reaching up to 105 °C. The initial offerings from TI's CC33xx family cater to both Wi-Fi 6 and Bluetooth Low Energy 5.3, all within a single IC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Connected Homes Through Home Automation

- 5.1.2 Increasing Internet Penetration into Homes and Enterprises

- 5.2 Market Challenges

- 5.2.1 Issues Related to Security and Privacy of Data and Connectivity of Devices and Interoperability

- 5.2.2 Slow Demand for Some Mobile Handset Types

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wi-Fi Standalone

- 6.1.2 Bluetooth Standalone

- 6.1.3 Wifi and Bluetooth Combo

- 6.1.4 Low-power Wireless IC

- 6.2 By End-user Application

- 6.2.1 Consumer

- 6.2.2 Enterprise

- 6.2.3 Mobile Handsets

- 6.2.4 Automotive

- 6.2.5 Industrial

- 6.2.6 Other End-user Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Qualcomm Incorporated

- 7.1.3 Mediatek Inc.

- 7.1.4 Intel Corporation

- 7.1.5 Texas Instruments Incorporated

- 7.1.6 STMicroelectronics NV

- 7.1.7 NXP Semiconductors NV

- 7.1.8 On Semiconductor Corporation

- 7.1.9 Infineon Technologies AG

- 7.1.10 Microchip Technology Inc.

- 7.1.11 Qorvo Inc.

- 7.1.12 Skyworks Solutions Inc.

- 7.1.13 Hisilicon Technologies Co. Ltd

- 7.1.14 Tsinghua Unigroup Co. Ltd (unisoc (Shanghai) Technologies Co. Ltd