|

市場調査レポート

商品コード

1440438

カーボンフォーム:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Carbon Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| カーボンフォーム:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

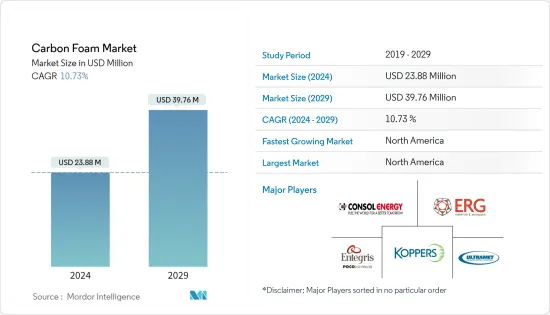

カーボンフォームの市場規模は、2024年に2,388万米ドルと推定され、2029年までに3,976万米ドルに達すると予測されており、予測期間(2024年から2029年)中に10.73%のCAGRで成長します。

COVID-19は、サプライチェーンと市場の混乱により、2020年の市場に大きな影響を与えました。パンデミックの間、カーボンフォームの生産を担う多くの工場が閉鎖されました。しかし、市場は急速に成長しており、パンデミック前のレベルに達しています。

主なハイライト

- 短期的には、航空宇宙および防衛産業におけるカーボンフォームの使用量の増加が、市場の需要を促進する重要な要因となります。

- カーボンフォームの製造プロセスの高コストが市場の成長を妨げています。

- 低コストのカーボンフォームの開発にますます注目が集まることで、今後数年間で市場にチャンスが生まれる可能性があります。

- 北米地域は市場を独占すると予想されており、予測期間中に最高のCAGRが見られる可能性もあります。

カーボンフォームの市場動向

航空宇宙および防衛産業での使用の増加

- カーボンフォームは、航空宇宙工具、耐火構造製品、エネルギー吸収構造、防爆システム、高温構造物など、さまざまな航空宇宙および防衛用途向けのエンジニアリング材料の製造に使用できます。航空機やロケットの断熱に広く使用されています。

- EMIシールドやレーダー吸収用途のための熱保護システムや構造パネルに使用できます。また、今後の第5世代航空機の重要な側面であるステルス技術にも使用できます。

- その軽量性、強度、優れた熱特性により、過酷な環境下でもロケットノズルシステムにも使用されます。固体ロケットモーターは、固体推進剤を燃焼させて高温ガスを生成し、ノズルから排出することで推力を生み出します。

- グラファイトカーボンフォームは、爆発エネルギー、指向性エネルギー兵器、電磁パルスの脅威から身を守ることができます。

- 2022年2月、中国空気力学研究開発センターは、極超音速兵器の性能を向上させるためにカーボンフォームベースのコーティングをテストしました。カーボンフォームベースのコーティングは衝撃波の衝撃を20%以上軽減し、空気力学的安定性を劇的に改善できることがわかりました。また、カーボンフォームは将来の極超音速飛行用のコーティング材料として大きな応用可能性があるとも述べた。

- 2021年10月、米国複合材料協会は空軍調査が行った調査の成果 の一部を認めました。この研究所では、カーボンフォーム技術と関連材料を開発し、ボーイング 787ドリームライナーや空軍、NASAの衛星などの重要なシステムや複合ツールを応用しました。

- ボーイングの商業見通し2022-2041によると、新型航空機の世界納入総数は2041年までに41,170機になると推定されています。このように膨大な納入が見込まれるため、カーボンフォームの需要は予測期間中に世界的に増加すると予想されます。

- さらに、ストックホルム国際平和調査(SIPRI)によると、昨年の世界の軍事支出総額は2020年と比較して0.7%増加し、2兆1,130億米ドルとなった。さらに、2021年の最大支出国5カ国は米国、中国、インド、英国とロシアが支出の62%を占めています。その結果、軍事費と防衛費の増加が防衛用途のカーボンフォームの需要を下支えすると予想されます。

米国が北米地域を制覇へ

- 北米地域が市場を独占すると予想されています。米国は、この地域で最大かつ最も強力な経済国の一つです。

- 2021年7月、農務省森林局の森林製品研究所とLigsteel LLCの科学者は、Domtar Inc.と協力して、カーボンフォームを硬くする植物の細胞壁に含まれる物質であるリグニンから高価値のカーボンフォームを製造しました。リグニンは安価で広く入手可能であり、紙パルプ産業では年間7,000万トンが生産されています。

- 米国は中国に次いで電気自動車の第2位の市場です。 EVの販売台数によると、昨年の国内のプラグイン電気自動車の総台数は約65万6,900台で、2020年と比較して約100%の成長率を記録しました。

- IEAによると、米国では、2030年までに販売される新車の乗用車と小型トラックの50%を電気自動車(EV)が占めることを連邦政府の目標としています。さらに、国際クリーン輸送評議会によると、2020年には、カリフォルニア州政府は、2035年までにカリフォルニア州で販売されるすべての新車と乗用トラックをBEVやPHEVを含むゼロエミッション車にすることを州に義務付ける大統領令を発表しました。

- さらに、連邦航空局(FAA)によると、2020年の同国の民間航空機の数は5,882機で、前年比22.9%の減少率を記録しました。商用艦隊は2041年に8,756隻に増加し、CAGRは2%になると予測されています。これにより、航空宇宙産業の複数の用途からの市場需要が増加すると予想されます。

カーボンフォーム業界の概要

カーボンフォーム市場は現在本質的に統合されており、主要企業が調査対象市場の過半数のシェアを占めています。市場の主要なプレーヤーには、CONSOL Energy Inc.、Entegris、Koppers Inc.、Ultramet、ERG Aerospaceなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 航空宇宙および防衛産業での使用の増加

- 抑制要因

- カーボンフォームの製造プロセスの高コスト

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベースの市場規模)

- タイプ

- グラファイト

- 非グラファイト

- エンドユーザー産業

- 航空宇宙と防衛

- 建築と建設

- 自動車

- 電気

- 産業

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- その他欧州

- 世界のその他の地域

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- American Elements

- Carbon-Core Corporation

- CONSOL Energy Inc.

- ERG Aerospace

- Firefly International Energy

- Koppers Inc.

- Entegris Inc.

- Ultramet

- Xiamen Zopin New Material Limited

第7章 市場機会と将来の動向

- 低コストカーボンフォームの開発

- その他の機会

The Carbon Foam Market size is estimated at USD 23.88 million in 2024, and is expected to reach USD 39.76 million by 2029, growing at a CAGR of 10.73% during the forecast period (2024-2029).

COVID-19 highly impacted the market in 2020 because of supply chain and market disruption. During the pandemic, many factories responsible for carbon foam production were shut down. However, the market is growing rapidly and has reached pre-pandemic levels.

Key Highlights

- Over the short term, increasing usage of carbon foam in the aerospace and defense industry is a key factor driving market demand.

- The high cost of the production process of carbon foam is hindering the market's growth.

- Increasing focus on developing low-cost carbon foam will likely create opportunities for the market in the coming years.

- The North American region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Carbon Foam Market Trends

Increasing Usage in the Aerospace and Defense Industry

- Carbon foam can be used to manufacture engineering material for various aerospace and defense applications, including aerospace tooling, fireproof structural products, energy-absorbing structures, blast protection systems, and hot structures. It is widely used to insulate aircraft and rockets.

- It can be used in thermal protection systems and structural panels for EMI shielding and radar-absorbing applications. It can also be used for stealth technology, an essential aspect of the upcoming fifth-generation aircraft.

- Due to its lightweight nature, strength, and excellent thermal properties, it is also used in rocket nozzle systems, even in harsh environments. Solid rocket motors generate their thrust by burning a solid propellant to generate hot gases, which are exhausted through a nozzle.

- Graphitic carbon foam can protect against blast energy, directed energy weapons, and electromagnetic pulse threats.

- In February 2022, the China Aerodynamics Research and Development Centre tested carbon foam-based coatings on hypersonic weapons to enhance their performance. It found that carbon foam-based coatings could reduce the impact of shock waves by more than 20% and dramatically improve aerodynamic stability. It also mentioned that carbon foam has great application potential as a coating material for future hypersonic flight.

- In October 2021, the American Society for Composites acknowledged some of the research work done by the Air Force Research Laboratory. The laboratory developed carbon foam technology and related materials and applied significant systems, such as those in the Boeing 787 Dreamliner and Air Force and NASA satellites, and composite tooling.

- According to the Boeing Commercial Outlook 2022-2041, the total global deliveries of new airplanes are estimated to be 41,170 by 2041. Due to such huge expected deliveries, the demand for carbon foam is expected to rise globally during the forecast period.

- Furthermore, according to the Stockholm International Peace Research Institute (SIPRI), the total global military expenditure increased by 0.7% to USD 2,113 billion last year compared to 2020. Moreover, the five largest spenders in 2021 were the United States, China, India, the United Kingdom, and Russia, accounting for 62% of expenditure. As a result, rising military and defense spending is expected to support the demand for carbon foam for defense applications.

United States to Dominate the North American Region

- The North American region is expected to dominate the market. The United States is one of the region's largest and most powerful economies.

- In July 2021, scientists from the USDA Forest Service's Forest Products Lab and Ligsteel LLC collaborated with Domtar Inc. to produce high-value carbon foam from lignin, a material found in plant cell walls that makes carbon foam hard. Lignin is inexpensive and widely available, with the pulp and paper industry producing 70 million tons per year.

- The United States is the second-largest market for electric vehicles after China. According to the EV volumes, the country's total plug-in electrical vehicles accounted for around 656,900 units last year, registering a growth rate of ~100% compared to 2020.

- According to the IEA, in the United States, the federal aim is for electric vehicles (EVs) to make up 50% of new passenger cars and light trucks sold by 2030. Moreover, as per the International Council on Clean Transportation, in 2020, the California Government announced an executive order which directs the state to require that, by 2035, all new cars and passenger trucks sold in California be zero-emission vehicles, including BEV and PHEV.

- Moreover, according to the Federal Aviation Administration (FAA), the number of aircraft in the country's commercial fleet accounted for 5,882 in 2020, witnessing a decline rate of 22.9% compared to the previous year. The commercial fleet is forecasted to increase to 8,756 in 2041, with an average annual growth rate of 2% per year. This is expected to increase the market demand from multiple applications in the aerospace industry.

Carbon Foam Industry Overview

The carbon foam market is currently consolidated in nature, where the top players hold the majority share of the market studied. Some of the major players in the market include CONSOL Energy Inc., Entegris, Koppers Inc., Ultramet, and ERG Aerospace (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage in the Aerospace and Defense Industry

- 4.2 Restraints

- 4.2.1 The High Cost of the Production Process of Carbon Foam

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Graphitic

- 5.1.2 Non-graphitic

- 5.2 End-user Industry

- 5.2.1 Aerospace and Defense

- 5.2.2 Building and Construction

- 5.2.3 Automotive

- 5.2.4 Electrical

- 5.2.5 Industrial

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Elements

- 6.4.2 Carbon-Core Corporation

- 6.4.3 CONSOL Energy Inc.

- 6.4.4 ERG Aerospace

- 6.4.5 Firefly International Energy

- 6.4.6 Koppers Inc.

- 6.4.7 Entegris Inc.

- 6.4.8 Ultramet

- 6.4.9 Xiamen Zopin New Material Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Low-cost Carbon Foam

- 7.2 Other Opportunities