|

市場調査レポート

商品コード

1684007

米国の除草剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)US Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の除草剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

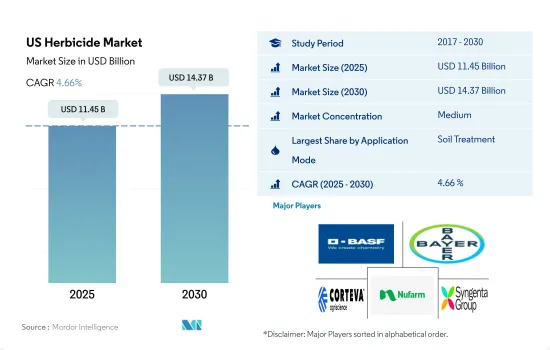

米国の除草剤市場規模は2025年に114億5,000万米ドルと推定され、2030年には143億7,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは4.66%で成長します。

米国では、土壌治療が除草剤散布の主要な手段として最も重要です。

- 米国では、農業で雑草を効率的に管理するために、さまざまな除草剤散布方法が採用されています。適切な散布方法を選択することで、農家は費用対効果の高い解決策を得ることができ、対象地域を正確にカバーし、無駄を最小限に抑えることができます。この効率向上により、除草剤の使用量が最適化され、最終的には農家の投入コストの削減につながります。

- 農業慣行では、土壌散布が除草剤使用の優勢なモードとして際立っており、2022年には除草剤散布セグメント全体の49.1%を占めました。この方法は主に穀物や穀類の栽培で採用されており、44.7%と最大の市場シェアを占めています。土壌処理除草剤が好まれるのは、雑草の生育を防止または最小限に抑えることで穀物や穀類の品質を保護する効果があるためです。土壌処理用除草剤は、雑草の発生前および生育初期の段階で雑草を防除するのに有効です。

- さらに、葉面散布法は金額ベースで第2位の市場シェアを確保し、2022年には29.2%を占めました。この散布技術は、雑草防除、特に正確なターゲティングが必要な作物、例えば対象植物の葉に直接散布する場合に有利であることが証明されています。この方法は地上部の雑草を防除するのに有効で、多くの農業・園芸分野で一般的に使用されています。

- 米国の農業分野では、除草剤の使用は作物の生産性を最適化し、全体的な収益性を高めることに重点が置かれています。アプリケーションのモードセグメントは、予測期間中に5.0%の予測CAGRを示すと予想されます。

米国の除草剤市場動向

除草剤耐性作物の普及が除草剤の消費を促進

- 米国における除草剤の使用は、いくつかの重要な要因によって推進されています。その要因のひとつは、除草剤が農業、園芸、造園などさまざまな分野で効果的な雑草管理に欠かせないツールとして認知されつつあることです。

- 雑草の持続性と適応性により、除草剤の散布量が増え、作用機序の異なる複数の除草剤が使用されるようになりました。集約農法の拡大も、除草剤使用量の増加に大きな役割を果たしています。増大する食糧需要を満たし、作物の収量を最大化するために、農家は農業経営を強化し、雑草防除のための除草剤への依存度を高めることになりました。

- 除草剤耐性の遺伝子組み換え(GM)作物の採用は、除草剤の消費を促進する上で重要な役割を果たしています。たとえば2020年には、遺伝子組み換え大豆が作付けされた大豆全体の94%を占め、遺伝子組み換え綿が作付けされた綿全体の96%を占め、作付けされたトウモロコシの92%が遺伝子組み換えトウモロコシでした。これらの遺伝子組み換え作物によって、農家は害を与えることなく除草剤を作物に直接散布できるようになり、目的の植物へのダメージを最小限に抑えながら、雑草を効果的に防除できるようになりました。

- 農薬規制の変更も、除草剤の消費パターンに影響を与える可能性があります。新しい農薬製剤や有効成分の承認や入手が、除草剤使用量の増加に寄与する可能性があります。2021年7月、環境保護庁(EPA)はパラコートの暫定的な再承認を発行し、これが除草剤市場の成長にさらに寄与しています。

- その結果、遺伝子組み換え除草剤耐性作物の採用増加や集約的農法の拡大が、予測期間中の米国における除草剤消費を促進すると予想されます。

トウモロコシ、小麦、サトウキビなどの主要作物における雑草蔓延の増加と、様々な雑草の防除における除草剤の必要性が市場を牽引する可能性

- 雑草の蔓延は依然として米国の農業における重要な課題であり、農家の収量損失と生産コストの増加を引き起こしています。米国ではアトラジン、パラコート、グリホサートが一般的に使用されている除草剤です。

- アトラジンは塩素化トリアジン系に属する浸透性除草剤で、一年生イネ科雑草や広葉雑草の出穂前対策に用いられます。アトラジンを含む農薬製剤は、トウモロコシ、スイートコーン、ソルガム、サトウキビ、小麦、マカデミアナッツ、グアバなど、さまざまな農作物への散布が承認されています。さらに、苗床/観葉植物や芝の管理にも使用されています。2022年の価格は1トン当たり1万3,800米ドルです。

- パラコート・ジクロライド、通称「パラコート」は、米国で広く使用されている除草剤のひとつです。また、一般的な最終用途製品名であるグラモキソン(Gramoxone)でも認識されています。パラコートは、多様な農業および非農業環境の雑草管理に重要な役割を果たしています。また、収穫前の綿花などの作物の乾燥にも使用されます。パラコートは2022年に1トン当たり4,600米ドルと評価されました。

- グリホサートは、浸透性、広域スペクトラム、ポスト出芽性除草剤です。グリホサートの使用はここ数十年で拡大し、現在米国で最も使用されている除草剤のひとつです。グリホサートを含む製品は、濃縮液剤、固形剤、すぐに使える液剤など、さまざまな製剤で販売されています。グリホサートは、農業と非農業の両方で雑草を防除する製品に使用されています。2022年には、1トン当たり1万6,600米ドルと評価されました。

米国の除草剤産業の概要

米国の除草剤市場は適度に統合されており、上位5社で48.82%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 適用モード

- 薬剤散布

- 葉面散布

- 燻蒸

- 土壌治療

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベルの概要、市場レベルの概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- ADAMA Agricultural Solutions Ltd

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- Upl Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50001709

The US Herbicide Market size is estimated at 11.45 billion USD in 2025, and is expected to reach 14.37 billion USD by 2030, growing at a CAGR of 4.66% during the forecast period (2025-2030).

In the United States, soil treatment holds the utmost importance as the primary mode of herbicide application

- In the United States, various modes of herbicide application are employed to efficiently manage weeds in agriculture. By selecting appropriate application methods, farmers can achieve cost-effective solutions, ensuring precise coverage of targeted areas and minimizing wastage. This enhanced efficiency optimizes herbicide usage, ultimately leading to reduced input costs for farmers.

- In agricultural practices, soil application stands out as the predominant mode of herbicide usage, which represented 49.1% of the total herbicide application segment in 2022. This method is majorly employed in the cultivation of grains and cereals, which holds the largest market share at 44.7%. The preference for soil treatment herbicides is driven by their efficacy in protecting the quality of grains and cereals by preventing or minimizing weed growth. They are effective in controlling weeds during their pre-emergent and early growth stages.

- Furthermore, the foliar application method secured the second-largest market share by value, which accounted for 29.2% in 2022. This application technique has proven to be advantageous for weed control, particularly in crops that require accurate targeting, for instance, when applied directly onto the leaves of the target plants. This method is effective for controlling above-ground weeds and is commonly used in many agricultural and horticultural settings.

- In the agricultural sector of the United States, herbicide usage is focused on optimizing crop productivity and enhancing overall profitability. The mode of application segment is expected to witness a projected CAGR of 5.0% during the forecast period.

US Herbicide Market Trends

The increasing adoption of herbicide-tolerant crops is driving the consumption of herbicides

- The usage of herbicides in the United States is driven by several key factors. One contributing factor is the growing recognition of herbicides as essential tools for effective weed management in various sectors, including agriculture, horticulture, and landscaping.

- The persistence and adaptability of weeds have led to higher herbicide application rates and the use of multiple herbicides with different modes of action. The expansion of intensive farming practices has also played a significant role in boosting herbicide usage. To meet the increasing demand for food and maximize crop yields, farmers have strengthened their farming operations, leading to a greater reliance on herbicides for weed control.

- The adoption of herbicide-tolerant genetically modified (GM) crops has played a significant role in driving the consumption of herbicides. For instance, in 2020, GMO soybeans made up 94% of all soybeans planted, GMO cotton made up 96% of all cotton planted, and 92% of corn planted was GMO corn. These GM crops allow farmers to apply herbicides directly to the crop without causing harm, effectively controlling weeds while minimizing damage to desired plants.

- Changes in pesticide regulations can also influence patterns of herbicide consumption. The approval and availability of new pesticide formulations or active ingredients may contribute to increased herbicide usage. In July 2021, the Environmental Protection Agency (EPA) issued an interim re-approval for paraquat, which has further contributed to the growth of the herbicide market.

- As a result, the increasing adoption of genetically modified herbicide-tolerant crops and the expansion of intensive farming practices are expected to drive the consumption of herbicides in the United States during the forecast period.

Increasing weed infestation in major crops like corn, wheat, and sugarcane and need of herbicides in controlling various weeds may drive the market

- Weed infestation remains a significant challenge in agriculture in the United States, causing yield losses and increased production costs for farmers. Atrazine, paraquat, and glyphosate are commonly used herbicides in the United States.

- Atrazine, a systemic herbicide belonging to the chlorinated triazine group, is utilized for targeted control of annual grasses and broadleaf weeds prior to their emergence. Pesticide formulations containing atrazine are approved for application on various agricultural crops, such as corn, sweet corn, sorghum, sugarcane, wheat, macadamia nuts, and guava. In addition, it is also used in nursery/ornamental and turf management. It is priced at USD 13.8 thousand per metric ton in 2022.

- Paraquat dichloride, commonly known as "paraquat," stands as one of the extensively employed herbicides in the United States. It is also recognized by its popular end-use product name, Gramoxone. Paraquat plays a crucial role in managing weeds across diverse agricultural and non-agricultural environments. It is also used for the desiccation of crops, like cotton, prior to harvest. Paraquat was valued at a price of USD 4.6 thousand per metric ton in 2022.

- Glyphosate is a systemic, broad-spectrum, and post-emergent herbicide. The use of glyphosate has grown over the last decades, and it is currently one of the most used herbicides in the United States. Products containing glyphosate are sold in various formulations, including liquid concentrate, solid, and ready-to-use liquid. Glyphosate is used in products to control weeds in both agricultural and non-agricultural settings. In 2022, it was valued at a price of USD 16.6 thousand per metric ton.

US Herbicide Industry Overview

The US Herbicide Market is moderately consolidated, with the top five companies occupying 48.82%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Nufarm Ltd and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 Upl Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms