|

|

市場調査レポート

商品コード

1440355

メンタルヘルスアプリ:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Mental Health Apps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| メンタルヘルスアプリ:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

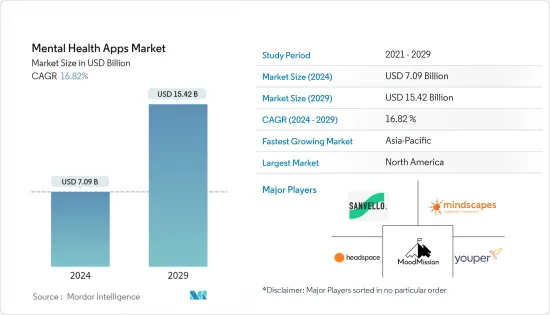

メンタルヘルスアプリの市場規模は、2024年に70億9,000万米ドルと推定され、2029年までに154億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に16.82%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)の発生はメンタルヘルスアプリ市場に大きな影響を与え、世界中のデジタルヘルス業界を大きく押し上げました。パンデミックの段階では、社会的距離の確保や孤立の限界や制限による状況に対処するためのメンタルヘルスアプリの使用が急増し、個人の精神状態に影響を及ぼしました。たとえば、PubMedが2021年12月に発表した記事によると、精神保健専門家からのサービスに対する需要の増加により、多くの人が対面サービスにアクセスするのに苦労しており、その結果、オンラインおよび遠隔医療サービスの需要が増大しました。オンラインのメンタルヘルスヘルプにアクセスする18~25歳のオーストラリアの若者の数が50%増加し、メンタルヘルスアプリのダウンロードが増加しました。さらに、2021年3月にPubMedに掲載された記事によると、最もダウンロードされた16のアプリのうち、10が瞑想系、13がダウンロード数の増加を示し、パンデミックが始まってから11のアプリがダウンロード数の10%増加を示しました。分析によると、メンタルヘルスに関する意識の高まりとm-healthサービスの技術進歩の増加により、市場はパンデミック後の段階で成長すると予想されています。

さらに、メンタルヘルスアプリの成長を後押ししている主な要因は、メンタルヘルスの重要性に対する意識の高まり、精神障害の急増、メンタルヘルスケア業界内で数社が実施する戦略的取り組みの増加、メンタルヘルスの利用の増加です。健康アプリケーション。たとえば、2022年のアメリカ精神衛生状況報告書によると、重度の大うつ病エピソード(MDE)を経験している若者の数は、2021年のデータセットから197,000人増加しました。したがって、うつ病性障害の発生率の増加はメンタルヘルスアプリの需要の急増につながり、それによって予測期間中の市場の成長を促進すると予想されます。

人々の意識の高まりを受けて、いくつかの企業、組織、政府機関がさまざまなプラットフォームでメンタルヘルスアプリの開発と立ち上げに取り組んでいます。たとえば、2021年4月、GOIは年齢層を超えた幸福を促進するために「MANAS」アプリを事実上立ち上げました。さらに、精神障害を持つ個人を支援するための新しいアプリの市場投入に多くの企業が関与しています。たとえば、2021年 10月に、Y Combinatorが支援するMentalHappyアプリは、アプリ内で低コストのピアサポートグループを開発し、メンタルヘルスケアを利用しやすく、手頃な価格で、偏見のないものにするという目標を開始しました。不安、離婚後の生活、黒人のメンタルヘルス。同様に、2021年 11月、Koo App &Fortisは世界メンタルヘルスデーに啓発キャンペーンを開始しました。さらに、2022年 4月、仮想行動健康サービスのプロバイダーであるTalkspaceは、経営陣、マネージャー、チームが心の知能指数(EQ)と精神的健康を優先順位付けし、構築できるように設計された雇用主向けの一連のサービスであるTalkspace Self-Guidedを開始しました。

したがって、メンタルヘルス問題の増加と新しいメンタルヘルスアプリケーションの発売の急増により、市場は予測期間中に大幅な成長を遂げると予想されます。ただし、データプライバシーと調査の懸念は、市場の成長を妨げる主要な要因です。

メンタルヘルスアプリ市場動向

うつ病および不安症の管理部門は、予測期間中に大幅な成長が見込まれる

うつ病と不安の管理部門は、うつ病と不安の負担の増大、うつ病と不安に関する取り組みの拡大、うつ病と不安を管理するためのいくつかのメンタルヘルスアプリの発売などの要因により、分析期間中に大幅な成長が見込まれると予想されます。

たとえば、WHOによる2021年9月の最新情報によると、うつ病は世界中で一般的な精神疾患であり、成人の5.0%と60歳以上の成人の5.7%を含む人口の3.8%が罹患していると推定されています。さらに、Mental Health America 2022レポートによると、テキサス州の精神疾患に罹患する人の数は、2022年に360万人であることが判明しています。うつ病や不安症などの精神疾患の症例数が増加するにつれて、医療サービスを利用する可能性が高まります。メンタルヘルスアプリの人気が高まり、市場セグメントの成長が促進されます。したがって、統計によれば、根底にある精神的ストレス要因を追跡するための人工知能や機械学習などの先進技術へのアクセスと統合が容易になったことにより、これらの精神状態に対処するためのメンタルヘルスアプリの使用が今後数年間で急増すると予想されています。

さらに、いくつかの市場プレーヤーがメンタルヘルスアプリを立ち上げており、この分野の成長に貢献しています。たとえば、2021年 8月、ヘッドスペースとオンデマンドのメンタルヘルスケアアプリのジンジャーは、不安からうつ病、より複雑な診断に至るまでのメンタルヘルス症状のサポートを提供し、消費者や消費者に直接販売するために、ヘッドスペースヘルスという単一の会社に合併すると報告しました。雇用主。同様に、2021年 9月に、デリーAIIMSは、不安やうつ病に対処する患者を支援するために、ShakshamとDishaという2つのモバイルアプリを開発しました。

したがって、うつ病と不安の問題の増加と新しいメンタルヘルスアプリケーションの発売の急増により、うつ病と不安セグメントは予測期間中に成長すると予想されます。

北米は市場で重要なシェアを保持すると予想されており、予測期間にも同様のシェアを獲得すると予想されます

北米では、確立されたヘルスケアIT産業、高度な技術インフラ、モバイルアプリケーションの使用量の増加、ストレス、うつ病、不安の負担の増大などの要因により、メンタルヘルスアプリ市場の成長が見込まれています。市場の成長を後押しする他の要因には、メンタルヘルスに関する意識の高まりや市場参加者による取り組みが含まれます。

たとえば、National Alliance on Mental Illness(NAMI)による2022年 2月の最新情報によると、米国では合計 2,630万人の成人がバーチャルメンタルヘルスサービスを受けています。同じ情報源によると、米国では成人の5人に1人が精神疾患を経験しており、米国の成人の20人に1人が重篤な精神疾患を経験しています。したがって、これはアメリカ人の間でメンタルアプリの使用を大いに刺激し、最終的に市場の成長を促進しました。

同様に、2021年 8月に、手頃な価格でパーソナライズされたヘルスケアを提供する米国のデータ主導の仮想プライマリケアプラットフォームであるK Healthが、メンタルヘルスを統合するためのオンデマンドのテキストベースの治療で人々と医療提供者を結び付けるメンタルヘルスアプリであるTrustを買収しました。そして身体の健康は、従来のヘルスケア制度では別々に扱われることが多い分野です。さらに、2021年4月、米国に拠点を置くLife Clips, Inc.は、子会社のCognitive Apps Softwareがメンタルヘルスの理解と管理のためのゆる3-in-1ツールの立ち上げに成功したと報告しました。さらに、2022年 2月には、メンタルヘルスに焦点を当てた革新的な新しい企業であるNobleが新しいアプリを立ち上げ、セッション間の自動サポートとセラピストが作成した研究に裏付けられたコンテンツをクライアントに提供しました。このような発展は、国内でメンタルヘルスアプリの需要が高まっていることを示しており、それが市場の成長に貢献しています。

したがって、精神疾患の増加と膨大な数の新しいメンタルヘルスアプリのリリースの結果、北米では予測期間中にメンタルヘルスアプリ市場の成長が見られると予想されます。

メンタルヘルスアプリ業界の概要

メンタルヘルスアプリ市場は細分化されており、世界および国内の複数のプレーヤーが存在します。主要企業は、パートナーシップ、協定、コラボレーション、新製品の発売、地理的拡大、合併、買収など、市場での存在感を高めるためにさまざまな成長戦略を採用しています。市場の主要企業としては、CVS Health Corporation、Sanvello Health, Inc.、Mindscapes、Headspace, Inc.、Youper, Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

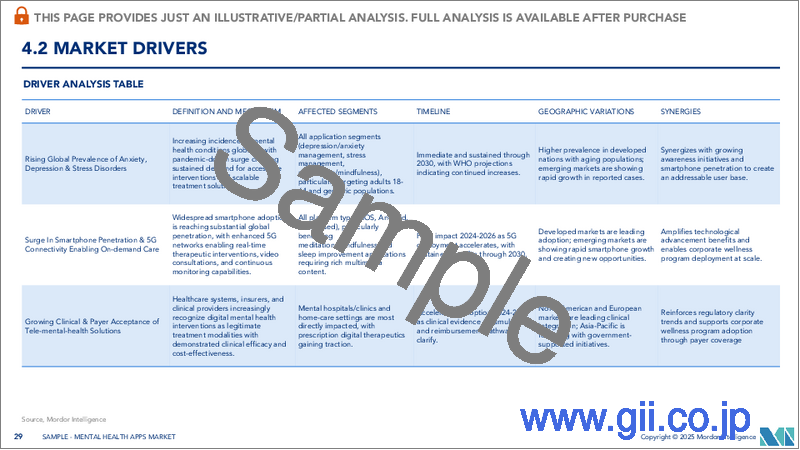

- メンタルヘルスの重要性に対する意識の高まり

- 世界中で精神状態が急増

- 市場抑制要因

- プライバシーと調査の懸念

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- プラットフォームタイプ別

- Android

- iOS

- その他のプラットフォームタイプ

- 用途別

- うつ病と不安症の管理

- ストレスマネジメント

- 瞑想管理

- その他の用途タイプ

- エンドユーザー別

- 在宅ケア環境

- 精神病院

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- MoodMission

- Sanvello Health, Inc.

- Mindscapes

- Headspace Inc.

- Youper Inc.

- K Health Inc.

- Calm

- Happify Health

- MoodTools

- CVS Health Corporation

- Zavfit

- Talkspace

- Real

- Wysa

第7章 市場機会と将来の動向

The Mental Health Apps Market size is estimated at USD 7.09 billion in 2024, and is expected to reach USD 15.42 billion by 2029, growing at a CAGR of 16.82% during the forecast period (2024-2029).

The COVID-19 outbreak substantially impacted the mental health apps market and greatly boosted the digital health industry worldwide. The pandemic phase witnessed an upsurge in the usage of mental health apps for coping with conditions due to the limitations and restrictions on social distancing and isolation, affecting individuals' mental states. For instance, as per the article published in December 2021 by PubMed, due to the increased demand for services from mental health professionals, many people struggled to access in-person services, which led to an augmented demand for online and telehealth services, including a 50% increase in the number of Australian young people aged 18-25 who were accessing online mental health help and increased the downloads of mental health apps. Additionally, as per the article published in March 2021 in PubMed, among the 16 most downloaded apps, 10 were meditational, 13 showed increased downloads, and 11 apps showed a 10% increase in downloads after the pandemic started. As per the analysis, the market is anticipated to witness growth in the post-pandemic phase due to the rise in awareness regarding mental health and the increase in technological advancements in m-health services.

Furthermore, the major factors boosting the growth of mental health apps are the increasing awareness of the importance of mental health, the surge in mental disorders, the rise in strategic initiatives undertaken by several companies within the mental healthcare industry, and the growing usage of mental health applications. For instance, as per the State of Mental Health in America 2022 report, the number of youths experiencing a severe major depressive episode (MDE) increased by 197,000 from the 2021 dataset. Thus, the rise in the incidence of depressive disorders leads to a surge in demand for mental health apps, which is thereby expected to boost market growth over the forecast period.

Owing to the increasing awareness among the population, several companies, organizations, and governmental bodies are engaged in developing and launching mental health apps across various platforms. For instance, in April 2021, the GOI virtually launched the "MANAS" app to promote well-being across age groups. Furthermore, numerous companies are involved in launching newer apps into the market to help individuals with mental disorders. For instance, in October 2021, the Y Combinator-backed MentalHappy app initiated the goal of making mental health care accessible, affordable, and stigma-free by developing low-cost peer support groups within the app to boost access to conditions such as coping with anxiety, life after divorce, and black mental health. Similarly, in November 2021, Koo App & Fortis launched an awareness campaign on World Mental Health Day. Furthermore, in April 2022, Talkspace, a provider of virtual behavioral health services, launched Talkspace Self-Guided, a suite of offerings for employers designed to help executives, managers, and teams prioritize and build emotional intelligence (EQ) and mental wellness in and out of the workplace.

Thus, due to the rise in mental health issues and the surge in new mental health application launches, the market is expected to witness significant growth over the forecast period. However, data privacy and research concerns are major factors hindering the market's growth.

Mental Health Apps Market Trends

Depression and Anxiety Management Segment is Expected to Witness Significant Growth Over the Forecast Period

The depression and anxiety management segment is expected to witness significant growth over the analysis period owing to factors such as the increasing burden of depression and anxiety, growing initiatives about depression and anxiety, and the launch of several mental health apps for managing depression and anxiety.

For instance, as per the September 2021 update by the WHO, depression is a common mental disorder worldwide, with an estimated 3.8% of the population affected, including 5.0% of adults and 5.7% of adults older than 60 years. Moreover, as per the Mental Health America 2022 report, the number of people affected by mental illness in Texas is found to be 3.6 million in 2022. As the number of mental illness cases, such as depression or anxiety, increases, the chance of utilizing mental health apps rises, thereby boosting market segment growth. Thus, the statistics indicate that the use of mental health apps for coping with these mental conditions is anticipated to surge over the coming years owing to the ease of access and integration of advanced technologies such as artificial intelligence and machine learning for tracking the underlying mental stressors.

Additionally, several market players are launching mental health apps, contributing to the segment's growth. For instance, in August 2021, Headspace and the on-demand mental healthcare app Ginger reported merging into a single company, called Headspace Health, to offer support for mental health symptoms ranging from anxiety to depression to more complex diagnoses and sell directly to consumers and employers. Similarly, in September 2021, Delhi AIIMS developed two mobile apps, Shaksham and Disha, to assist patients dealing with anxiety and depression.

Thus, due to the rise in depression and anxiety issues and the surge in new mental health application launches, the depression and anxiety segment is expected to witness growth over the forecast period.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same in the Forecast Period

North America is anticipated to witness growth in the mental health apps market owing to factors such as the well-established healthcare IT industry, sophisticated technological infrastructure, the rising usage of mobile applications, and the increasing burden of stress, depression, and anxiety. Some other factors boosting the market's growth include the rising awareness about mental health and the initiatives undertaken by the market players.

For instance, as per a February 2022 update by the National Alliance on Mental Illness (NAMI), in the United States, a total of 26.3 million adults received virtual mental health services. As per the same source, 1 in 5 adults in the United States experiences mental illness, whereas 1 in 20 adults in the United States experiences serious mental illness. Thus, this has greatly stimulated the use of mental apps among Americans, ultimately augmenting the market's growth.

Likewise, in August 2021, K Health, a United States-based data-driven virtual primary care platform providing affordable, personalized healthcare, acquired Trust, the mental health app that connects people and providers for on-demand text-based therapy to integrate mental and physical health, disciplines that are often treated separately in the traditional healthcare system. Additionally, in April 2021, Life Clips, Inc., based in the United States, reported that its subsidiary Cognitive Apps Software had successfully launched its Yuru 3-in-1 tool for understanding and managing mental health. Moreover, in February 2022, Noble, a new innovative, mental health-focused company, launched its new app, offering automated between-session support and therapist-created, research-backed content for clients. Such developments indicate the growing demand for mental health apps in the country, thereby contributing to market growth.

Thus, as a result of the rise in mental illness and the huge number of new mental health app launches, North America is expected to witness growth in the mental health app market over the forecast period.

Mental Health Apps Industry Overview

The mental health apps market is fragmented, with several global and domestic players. The key players are adopting different growth strategies to enhance their market presence, such as partnerships, agreements, collaborations, new product launches, geographical expansions, mergers, and acquisitions. Some key players in the market are CVS Health Corporation, Sanvello Health, Inc., Mindscapes, Headspace, Inc., and Youper, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Awareness Pertaining to the Importance of Mental Health

- 4.2.2 Upsurge in Mental Conditions Worldwide

- 4.3 Market Restraints

- 4.3.1 Privacy and Research Concerns

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Platform Type

- 5.1.1 Android

- 5.1.2 iOS

- 5.1.3 Other Platform Types

- 5.2 By Application

- 5.2.1 Depression and Anxiety Management

- 5.2.2 Stress Management

- 5.2.3 Meditation Management

- 5.2.4 Other Application Types

- 5.3 By End User

- 5.3.1 Home Care Settings

- 5.3.2 Mental Hospitals

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 MoodMission

- 6.1.2 Sanvello Health, Inc.

- 6.1.3 Mindscapes

- 6.1.4 Headspace Inc.

- 6.1.5 Youper Inc.

- 6.1.6 K Health Inc.

- 6.1.7 Calm

- 6.1.8 Happify Health

- 6.1.9 MoodTools

- 6.1.10 CVS Health Corporation

- 6.1.11 Zavfit

- 6.1.12 Talkspace

- 6.1.13 Real

- 6.1.14 Wysa