|

市場調査レポート

商品コード

1692105

ヘリコプターサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Helicopter Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘリコプターサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

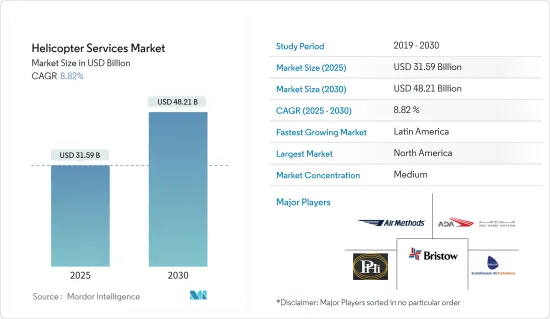

ヘリコプターサービス市場規模は2025年に315億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.82%で、2030年には482億1,000万米ドルに達すると予測されます。

ヘリコプターは、ホバリング、着陸、垂直離陸、限られた空間への出入りができるため、さまざまな分野で広く利用されています。用途と運航コストに応じて、オペレーターは特定のヘリコプター・モデルを選択します。現在、エアバス、ベル、ロビンソン・ヘリコプターが新規納入機数で市場を独占しています。また、軽量ヘリコプターに対する様々なエンドユーザーからの需要は、予測期間中に市場をプラスに牽引すると予想されます。

高度な飛行能力を持つ大型ドローンの導入は、ヘリコプター会社が現在の技術的制約を取り除くことができないことと相まって、いくつかの用途においてドローンサービスがヘリコプターサービスの代替となり続ける結果となりました。この要因は、予測期間中の市場の成長に課題を与える可能性があります。

しかし、深刻な道路渋滞や、特に新興諸国における救急医療サービスにおけるヘリコプターサービスの迅速な空中輸送の必要性などの要因が、ヘリコプターサービス市場に新たな機会を生み出しています。

ヘリコプターサービス市場の動向

予測期間中、最も高い成長が見込まれるのは航空救急車セグメント

航空救急車は、遠隔地へのアクセス制限や長時間の移動という問題を軽減することができるため、従来の道路救急車サービスよりも多くの利点があります。航空救急車にはさまざまな医療機器が装備され、医療クルーが搭乗し、患者に初期救急医療を提供します。救命率の向上、迅速で快適な搬送、短時間で広い範囲をカバーできるなど、いくつかの利点があるため、航空救急サービスの市場は増加の一途をたどっています。こうした利点から、ヘリコプターは救急医療搬送の有力な選択肢となっています。

例えば、2019年から2023年にかけて、世界全体で268機のヘリコプターが運航され、さまざまな救急・医療サービスを実施しています。航空救急サービス用のヘリコプターは、相手先ブランド製造業者(OEM)によって軽量化されています。この需要に対応するため、複数の国が新たな航空救急ヘリコプターを調達しています。例えば、2023年11月、ノルウェー航空救急隊は、デンマークでヘリコプターによる救急医療サービスを実施するため、H135を3機と5枚羽根のH145を2機納入する契約をエアバスに発注しました。同様に2023年12月、ガマ・アビエーションはウェールズ航空救急チャリティーのためにヘリコプター救急医療サービス(HEMS)を開始しました。7,000万米ドルの契約により、エアバスH145ヘリコプター4機が運用・保守され、その拠点は同慈善団体の既存施設となります。このように、相手先商標製品メーカー(OEM)によるこのような技術的進歩により、ロータークラフト分野は予測期間中に目覚ましい成長を見せると思われます。

予測期間中、北米が最大の市場シェアを占める

ヘリコプターサービス市場では、北米が最も高いシェアを占めています。この優位性は、ヘリコプター保有台数が最も多いことと、航空救急サービスにヘリコプターの利用が増加していることによる。米国のヘリコプター保有機数は約7,014機で、そのうち航空救急車は1,000機以上です。よりクリーンで持続可能なエネルギー需要への傾斜が強まる中、全米で増加する洋上風力発電所プロジェクトがヘリコプターサービスの需要を押し上げています。その結果、新たな契約やパートナーシップが市場価値を高めています。

例えば、OrstedとEversourceは2022年4月、HeliService International Inc.が両社の合弁事業である米国北東部の洋上風力発電プロジェクトのヘリコプター乗組員交代業務を受注したと発表しました。同社はレオナルドAW169ヘリコプターを使用し、日常業務をサポートします。同国では石油・ガス部門からの収入が増加しており、そのためヘリコプターサービス業界のオフショア分野におけるヘリコプターサービスの必要性に直接影響を与えています。

さらに、プライベート・エクイティ投資家が航空救急市場の維持・運営に参入しているため、より良いサービスを提供できる可能性は高まっているもの、運航コストの増大が顧客に課されるリスクもあります。同様に、救急医療サービス、捜索救助、レジャー用チャーター便など、さまざまな用途のヘリコプターに対する需要がカナダの運航会社から高まっていることも、同地域全体の市場成長を後押ししています。

ヘリコプターサービス産業の概要

ヘリコプターサービス市場は半固体化しており、複数の事業者が様々なヘリコプターサービスを提供しているのが特徴です。長年にわたり、航空規制機関はヘリコプター運航会社に対して厳しく厳格な規則や規制を導入してきました。しかし現在では、さまざまな政府がヘリコプターや固定翼機の運航を奨励する支援法を導入し、一般航空部門の発展に努めています。このため、地元プレーヤーの流入が増え、既存プレーヤーの新市場への進出も拡大しています。さらに、主要企業は戦略的パートナーシップ、合併、買収を通じて事業拡大に注力しています。このような戦略は、予測期間中のプレーヤーの成長に役立つと期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 航空救急車

- ビジネス・企業旅行

- 捜索と救助

- レジャーチャーター

- 輸送

- メディアとエンターテイメント

- 測量

- オフショア

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- インドネシア

- マレーシア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- トルコ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Acadian Air Med Services(Acadian Companies)

- Air Methods Corporation

- Heli-union

- Abu Dhabi Aviation

- Emsos Medical Pvt. Ltd.

- Bristow Group Inc

- LUXEMBOURG AIR RESCUE ASBL

- PHI Group, Inc.

- Babcock Scandinavian Air Ambulance(Babcock International Group)

- CHC Group LLC

第7章 市場機会と今後の動向

The Helicopter Services Market size is estimated at USD 31.59 billion in 2025, and is expected to reach USD 48.21 billion by 2030, at a CAGR of 8.82% during the forecast period (2025-2030).

Helicopters are widely used in several sectors because they can hover, land, take off vertically, and enter and exit confined spaces. Depending upon the application and cost of operation, operators select a particular helicopter model. Airbus, Bell, and Robinson helicopters are currently dominating the market in terms of new deliveries. In addition, the demand from various end users for lightweight helicopters is expected to drive the market positively during the forecast period.

The introduction of large drones with advanced flight capabilities, coupled with the inability of helicopter companies to eliminate current technology limitations, resulted in drone services continuing to be a substitute for helicopter services in several applications. This factor might challenge the market's growth during the forecast period.

However, factors such as severe road congestion and the need for quicker aerial transportation for helicopter services in emergency medical services, especially in developing countries, create new opportunities for the helicopter services market.

Helicopter Services Market Trends

Air Ambulance Segment is Projected to Show the Highest Growth During the Forecast Period

Air ambulance offers numerous advantages over conventional road ambulance services, as the former helps mitigate the issue of limited access to remote areas and prolonged travel durations. Air ambulances are equipped with different medical equipment and have an onboard medical crew that provides initial emergency medical care to patients. The market for air ambulance services is on the rise owing to several benefits, such as increased survival rates, swift and comfortable transportation, and a vast coverage range in a shorter time. These advantages make helicopters a compelling choice for emergency medical transportation.

For instance, globally, from 2019 to 2023, 268 helicopters were in operation, performing various emergency and medical services. Helicopters for air ambulance services have been made lightweight by original equipment manufacturers (OEMs). Multiple countries are procuring new air ambulance helicopters to cater to this demand. For instance, in November 2023, the Norwegian Air Ambulance awarded a contract to Airbus to deliver three H135s and two five-bladed H145s to carry out helicopter emergency medical service missions in Denmark. Similarly, in December 2023, Gama Aviation launched its Helicopter Emergency Medical Services (HEMS) for the Wales Air Ambulance Charity. Under a USD 70 million contract, a fleet of four Airbus H145 helicopters will likely be operated and maintained, with their base of operations being the charity's existing sites. Thus, such technological advancements made by the original equipment manufacturers (OEMs) will lead to the rotor-craft segment showing impressive growth during the forecast period.

North America to Exhibit the Largest Market Share During the Forecast Period

North America held the highest shares in the helicopter services market. This dominance is owing to the presence of the largest helicopter fleet and the rising use of helicopters for air ambulance services. The US has a total fleet of around 7,014 helicopters, with air ambulances recorded at more than 1000 units. With the increase in inclination toward cleaner, more sustainable energy demands, the increasing offshore wind farm projects across the country have driven the demand for helicopter services. As a result, new contracts and partnerships have increased market value.

For instance, Orsted and Eversource announced in April 2022 that HeliService International Inc. had been awarded the contract for helicopter crew change operations for the two companies' joint venture of offshore wind projects in the Northeast United States. The company will use Leonardo AW169 helicopters to support its everyday operations. The country's increasing revenue from the oil and gas sector has been witnessing an increasing demand, which has thus directly impacted the need for helicopter services in the offshore segment of the helicopter services industry.

Furthermore, the growing influx of private equity investors into maintaining and operating the air ambulance market, despite improving the chances for better services, poses a risk of the increased cost of operations that could be levied on the customers. Similarly, the growing demand for helicopters for various applications such as emergency medical services, search and rescue, leisure charters, and others from Canadian operators drives the market growth across the region.

Helicopter Services Industry Overview

The helicopter services market is semi-consolidated and is characterized by several operators providing various helicopter services. Some of the major players in the market are Babcock Scandinavian Air Ambulance (Babcock International Group), Abu Dhabi Aviation, Air Methods Corporation, Bristow Group Inc., and PHI Group, Inc. Over the years, the aviation regulatory bodies introduced tough and rigid rules and regulations for helicopter operators. However, various governments are now introducing supportive laws encouraging helicopter and fixed-wing aircraft operations to develop the general aviation sector. This leads to increased influx of local players and expanding existing players into new markets. Furthermore, the key players focus on business expansion through strategic partnerships, mergers, and acquisitions. Such strategies are expected to help the players' growth during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Air Ambulance

- 5.1.2 Business and Corporate Travel

- 5.1.3 Search and Rescue

- 5.1.4 Leisure Charter

- 5.1.5 Transport

- 5.1.6 Media and Entertainment

- 5.1.7 Surveying

- 5.1.8 Offshore

- 5.1.9 Other Applications

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Indonesia

- 5.2.3.6 Malaysia

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Turkey

- 5.2.5.5 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Acadian Air Med Services (Acadian Companies)

- 6.2.2 Air Methods Corporation

- 6.2.3 Heli-union

- 6.2.4 Abu Dhabi Aviation

- 6.2.5 Emsos Medical Pvt. Ltd.

- 6.2.6 Bristow Group Inc

- 6.2.7 LUXEMBOURG AIR RESCUE ASBL

- 6.2.8 PHI Group, Inc.

- 6.2.9 Babcock Scandinavian Air Ambulance (Babcock International Group)

- 6.2.10 CHC Group LLC