|

市場調査レポート

商品コード

1689969

切除不能肝細胞がん:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Unresectable Hepatocellular Carcinoma - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 切除不能肝細胞がん:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 129 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

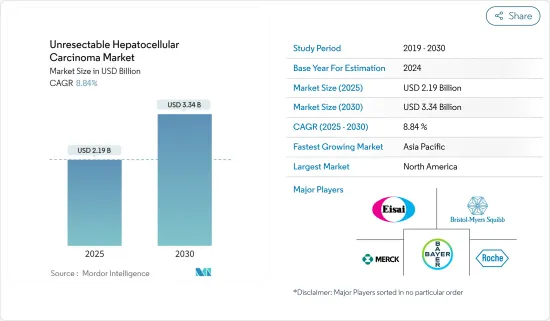

切除不能肝細胞がんの市場規模は2025年に21億9,000万米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは8.84%で、2030年には33億4,000万米ドルに達すると予測されます。

COVID-19の流行は切除不能肝細胞がん市場に大きな影響を与えています。COVID-19の肝がんへの影響」と題された調査によるものである:2020年5月にNational Library of Medicineに掲載された「パンデミック中およびパンデミック後」によると、肝細胞がん(HCC)患者は、SARS-CoV-2による肝障害が既存の肝炎ウイルス感染や肝硬変を合併させる可能性があるため、他のがん患者よりもCOVID-19の影響を受けやすいです。さらに、COVID-19パンデミックの間、抗がん剤へのアクセスに障壁があったため、医薬品サプライチェーンの安定性と完全性が損なわれ、ヘルスケア施設全体への医薬品の供給が制限されました。このように、COVID-19パンデミックはヘルスケアの優先順位を変化させ、HCC管理に悪影響を及ぼす可能性があります。

市場の成長を促す主な要因は、肝がんの罹患率の高さと新しい治療法の進歩です。

肝がんの罹患率の高さは、市場の成長を促す主な要因です。米国疾病予防管理センターによる2021年9月の最新情報によると、米国では毎年、男性約2万4500人、女性約1万人が肝臓がんに罹患し、男性約1万8600人、女性約9000人がこの病気で死亡しています。この統計によれば、患者数は大幅に増加しており、市場の成長を後押しすると予想されます。また、GLOBOCAN 2020によると、2020年の世界の新規肝がん患者数は90万6,000人と推定され、2040年には140万人に達すると予測されています。このように、肝がんの罹患率の増加は切除不能肝細胞がんの増加率を反映しており、切除不能肝細胞がん治療の需要を増大させています。

さらに、新しい治療法の進歩が市場の成長を後押ししています。例えば、Karger Journal誌に掲載された記事によると、2021年、様々な第3相試験で、チロシンキナーゼ阻害剤レンバチニブ、レゴラフェニブ、カボザンチニブのHCCにおける臨床的有用性が報告されました。さらに、The Reagents of the University of Californiaによる2022年の最新情報によると、肝細胞がん治療に関して51件の臨床試験が進行中です。2021年10月に発表された"Hepatic Arterial Infusion Chemotherapy Is a Feasible Treatment Option for Hepatocellular Carcinoma:A New Update "と題された論文によると、肝動脈注入化学療法(HAIC)は進行肝細胞がん患者において生存率が高いです。このように、肝細胞がんの治療において先進的な薬剤が利用できるようになったことで、予測期間中に市場が活性化すると予想されます。

しかし、診断件数が少なく、現在の治療薬の有効性が低いことが、市場の成長を抑制する主な要因となっています。

切除不能肝細胞がん市場の動向

化学療法が切除不能肝細胞がん市場で大きなシェアを占める

治療別では、化学療法分野が大きな成長を遂げると予測されています。同分野の成長を後押しする主な要因は、肝細胞がんの有病率の増加、薬剤承認の増加、新たな治療選択肢の進歩です。

例えば、米国臨床腫瘍学会(ASCO)による2021年の最新情報によると、化学塞栓療法は肝動脈注入に類似した化学療法の一種です。同じ情報源によると、この治療法では薬剤が肝動脈に注入され、動脈を通る血液の流れが短時間遮断されます。そのため、化学療法が腫瘍内に長く留まり、化学療法の治療効果が高くなります。したがって、このような要因が肝細胞がんに罹患している患者に対するより良い治療オプションとして化学療法の採用を後押しし、それによってこのセグメントの成長に寄与しています。

さらに、2022年2月に発表されたニュース記事には、中国の天津がん病院で実施された研究の詳細が記載されています。研究者らは、天津がん病院の中級/進行HCC患者35人を調査しました。この研究では、原発性肝がんの中で最も頻度の高い切除不能肝細胞がん(HCC)患者において、PD-1免疫チェックポイント抑制と経動脈的化学療法およびレンビマ(レンバチニブ)の併用が予後を改善すると結論づけた。このような要因は、患者集団における化学療法の採用を増加させ、このセグメントの成長を促進します。

このように、上記の要因が予測期間中の同分野の成長を後押しすると予想されます。

北米が切除不能肝細胞がん市場を独占

北米では米国が市場の主要シェアを占めています。同国における肝がんの有病率の増加、薬剤開発における技術進歩、研究開発投資の増加、高齢者人口の増加などの要因が、予測期間中に米国の切除不能肝細胞がん市場を牽引すると予想されます。GLOBOCAN 2020のデータによると、2020年の同国における肝・肝内胆管がん推定患者数は42,284人でした。2040年には52,703人に達すると予測されています。切除不能な肝細胞がんは、肝がんの中で最も多いタイプです。同国ではがん患者の増加が見込まれており、市場の成長を牽引する可能性があります。

複数の市場プレーヤーが戦略的イニシアチブの実施に取り組んでおり、それによって市場の成長に寄与しています。例えば、2022年2月、固形がんを治療する新規T細胞療法を開発する臨床段階のバイオテクノロジー企業であるEureka Therapeutics Inc.は、米国食品医薬品局(FDA)が肝がんの中で最も一般的な肝細胞がん(HCC)の治療薬としてET140203とECT204に希少疾病用医薬品指定(ODD)を付与したことを報告しました。2020年1月には、アストラゼネカのデュルバルマブ(イムフィンジ)とトレメリムマブが、肝細胞がん(HCC)の治療薬として米国FDAの希少疾病用医薬品指定を受けました。

このように、上記の要因により、予測期間中、同地域の市場は大きく成長すると予想されます。

切除不能肝細胞がん産業の概要

切除不能肝細胞がん市場の競争は中程度で、少数の主要企業で構成されています。AstraZeneca PLC、Bayer AG、Bristol-Myers Squibb Company、Celgene Corporation、Eisai、F. Hoffmann-La Roche Ltd、Merck &Co.Inc.、ファイザーInc.がかなりの市場シェアを占めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 肝がんの罹患率の高さ

- 新しい治療法の進歩

- 市場抑制要因

- 診断の少なさと現行治療薬の有効性の低さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 治療別

- 化学療法

- 分子標的治療

- 免疫療法

- その他の治療

- エンドユーザー別

- 病院

- がんセンター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Astrazeneca PLC

- Bayer AG

- Bristol-Myers-Squibb Company

- Celgene Corporation

- Eisai Co. Ltd

- F. Hoffmann-La Roche Ltd

- Merck & Co. Inc.

- Pfizer Inc.

- Chugai Pharmaceutical Co. Ltd

- Pharmaxis

- Eli Lilly

- BeiGene

第7章 市場機会と今後の動向

The Unresectable Hepatocellular Carcinoma Market size is estimated at USD 2.19 billion in 2025, and is expected to reach USD 3.34 billion by 2030, at a CAGR of 8.84% during the forecast period (2025-2030).

The COVID-19 pandemic has significantly impacted the unresectable hepatocellular carcinoma market. As per a research study titled "Impacts of COVID-19 on Liver Cancers: During and after the Pandemic", published in the National Library of Medicine in May 2020, hepatocellular carcinoma (HCC) patients are more vulnerable to the effects of COVID-19 than other cancer patients as the hepatic injury caused by SARS-CoV-2 could complicate the existing hepatitis virus infection and cirrhosis. Further, barriers to accessing cancer drugs during the COVID-19 pandemic endangered the stability and integrity of pharmaceutical supply chains, thus limiting the supply of drugs across healthcare facilities. Thus, the COVID-19 pandemic has altered healthcare priorities, which may adversely impact HCC management.

The major factors fueling the market's growth are the high incidence rate of liver carcinoma and the advancement in new treatment options.

The high incidence rate of liver carcinoma is a major factor driving the market's growth. According to a September 2021 update by the Centers for Disease Control and Prevention, each year, about 24,500 men and 10,000 women in the United States get liver cancer, and about 18,600 men and 9,000 women die from the disease. As per the statistics, there is a significant rise in the patient pool, which is expected to boost the market's growth. Additionally, according to GLOBOCAN 2020, the estimated number of new liver cancer cases worldwide in 2020 was 906,000, and the number is expected to reach 1.40 million by 2040. Thus, the increasing incidence rate of liver cancer reflects the growing rate of unresectable hepatocellular carcinoma, which is augmenting the demand for unresectable HCC treatment.

Moreover, advancements in new treatment options are boosting the market's growth. For instance, according to an article published in Karger Journal, in 2021, various phase 3 trials reported a clinical benefit for the tyrosine kinase inhibitors lenvatinib, regorafenib, and cabozantinib in HCC. Additionally, as per a 2022 update by The Reagents of the University of California, 51 clinical trials are in progress for hepatocellular carcinoma treatment. As per an October 2021 published article titled "Hepatic Arterial Infusion Chemotherapy Is a Feasible Treatment Option for Hepatocellular Carcinoma: A New Update", hepatic arterial infusion chemotherapy (HAIC) has greater survival in patients with advanced HCC. Thus, the availability of advanced drugs in the treatment of hepatocellular carcinoma is expected to boost the market over the forecast period.

However, fewer diagnoses and poor efficacy of current therapeutic agents are major factors restraining the market's growth.

Unresectable Hepatocellular Carcinoma Market Trends

Chemotherapy Holds Significant Share in the Unresectable Hepatocellular Carcinoma Market

By treatment, the chemotherapy segment is expected to witness significant growth. The major factors fueling the segment's growth are the increasing prevalence of hepatocellular carcinoma, the growing number of drug approvals, and advancements in new treatment options.

For instance, as per a 2021 update by the American Society of Clinical Oncology (ASCO), chemoembolization is a type of chemotherapy treatment similar to hepatic arterial infusion. The same source also reported that drugs are injected into the hepatic artery during this procedure, and the flow of blood through the artery is blocked for a short time. Thus, the chemotherapy stays in the tumor for a longer period, making chemotherapy treatment more effective. Therefore, such factors are boosting the adoption of chemotherapy as a better treatment option for patients suffering from HCC, thereby contributing to the segment's growth.

Furthermore, a news article published in February 2022 detailed a study conducted at Tianjin Cancer Hospital in China. The researchers examined 35 patients with intermediate/advanced HCC at Tianjin Cancer Hospital. The study concluded that in patients with unresectable hepatocellular carcinoma (HCC), the most frequent kind of primary liver cancer, combining PD-1 immune checkpoint suppression with transarterial chemotherapy and Lenvima (lenvatinib) improved prognosis. Such factors increase the adoption of chemotherapy among the patient population, thus driving the segment's growth.

Thus, the factors mentioned above are anticipated to boost the segment's growth over the forecast period.

North America Dominates the Unresectable Hepatocellular Carcinoma Market

Within North America, the United States holds the major share of the market. Factors such as the increasing prevalence of liver cancer in the country, technological advancements in drug development, increasing R&D investments, and the growing geriatric population are expected to drive the US unresectable hepatocellular carcinoma market during the forecast period. According to data by GLOBOCAN 2020, the estimated number of liver and intrahepatic bile duct cancer cases in the country was 42,284 in 2020. The number is expected to reach 52,703 by 2040. Unresectable hepatocellular carcinoma is the most common type of liver cancer. The expected increase in cancer cases in the country may drive the market's growth.

Several market players are engaged in implementing strategic initiatives, thereby contributing to the market's growth. For instance, in February 2022, Eureka Therapeutics Inc., a clinical-stage biotechnology company developing novel T-cell therapies to treat solid tumors, reported that the US Food and Drug Administration (FDA) granted Orphan Drug Designation (ODD) to ET140203 and ECT204 for the treatment of hepatocellular carcinoma (HCC), the most common form of liver cancer. In January 2020, AstraZeneca's durvalumab (Imfinzi) and tremelimumab were granted the US FDA Orphan Drug Designation to treat hepatocellular carcinoma (HCC).

Thus, due to the above-mentioned factors, the market is expected to grow significantly in the region over the forecast period.

Unresectable Hepatocellular Carcinoma Industry Overview

The unresectable hepatocellular carcinoma market is moderately competitive and consists of a few major players. Companies like AstraZeneca PLC, Bayer AG, Bristol-Myers Squibb Company, Celgene Corporation, Eisai Co. Ltd, F. Hoffmann-La Roche Ltd, Merck & Co. Inc., and Pfizer Inc. hold a substantial market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Incidence Rate of Liver Carcinoma

- 4.2.2 Advancement in New Treatment Options

- 4.3 Market Restraints

- 4.3.1 Less Diagnosis and Poor Efficacy of Current Therapeutic Agents

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Treatment

- 5.1.1 Chemotherapy

- 5.1.2 Molecularly Targeted Therapy

- 5.1.3 Immunotherapy

- 5.1.4 Other Treatments

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Cancer Centers

- 5.2.3 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Astrazeneca PLC

- 6.1.2 Bayer AG

- 6.1.3 Bristol-Myers-Squibb Company

- 6.1.4 Celgene Corporation

- 6.1.5 Eisai Co. Ltd

- 6.1.6 F. Hoffmann-La Roche Ltd

- 6.1.7 Merck & Co. Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Chugai Pharmaceutical Co. Ltd

- 6.1.10 Pharmaxis

- 6.1.11 Eli Lilly

- 6.1.12 BeiGene