|

市場調査レポート

商品コード

1689849

採血用チューブ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Blood Collection Tubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 採血用チューブ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 106 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

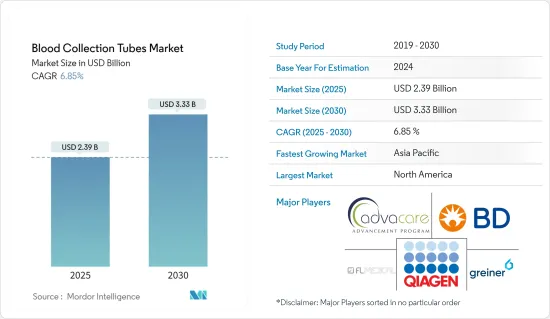

採血用チューブの市場規模は2025年に23億9,000万米ドルと予測され、2030年には33億3,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.85%です。

パンデミックは市場に影響を与えました。2021年2月、WHOは備えと迅速な対応の重要性を強調し、パンデミック時の血液供給の安全性と充足性に対する潜在的なリスクを軽減するために血液サービスが取るべき主要な行動と対策を概説しました。さらに、2022年4月にNational Library of Medicineに掲載された研究によれば、血液センターは、ウイルスが血液の安全性を直接脅かすことはないため、自国の血液供給量を増やすような取り組みや政策を開始することにもっと焦点を当てるべきです。同様に、採血家庭用チューブなどの製品発売を増やすなどの取り組みも、予測期間中の市場成長を高めると予想されます。例えば、2021年12月、Ethos Laboratories社は、COVID-19中和抗体検査用の指刺し自己採取キットTru-Immuneを発売しました。このような製品の発売により、家庭での安全な採血手順が提供されるため、このような製品の採用が増加すると予想されるが、現在、パンデミックは沈静化しているため、市場の牽引力は弱まっており、本調査の予測期間中は安定した成長が見込まれます。

市場成長の主な要因は、老人人口の増加と慢性疾患の罹患率の増加です。さらに、さまざまな疾患や事故による手術件数の増加が市場を押し上げています。炎症性疾患や感染性疾患の負担増に伴い、これらの疾患に対する認識も高まり、採血の需要も増加しているため、これらの疾患の負担増は市場に大きな影響を与えると予想され、このセグメントの成長に大きく好影響を与えると期待されます。例えば、世界保健機関(WHO)の2022年10月の更新によると、2021年の結核罹患者数は世界全体で約1,060万人と推定され、そのうち120万人は小児です。同様に、手術件数の増加が市場の成長を高めると予想されます。2022年8月に更新された経済協力開発機構によると、2021年にポルトガル、デンマーク、アイルランド、ノルウェーなどの欧州諸国で行われた手術件数(単位:千件)は、それぞれ94.87件、49.33件、32.84件、21.5件となっています。新興欧州諸国におけるこのような膨大な手術件数は、採血用チューブの需要増につながり、市場開拓の原動力となります。このように、上記の要因は市場成長を増加させると予想されます。

さらに、市場プレーヤー間の協定も市場成長の要因の一つです。例えば、2021年11月、Q-Sera Pty Ltdはテルモ株式会社と、Q-Seraの血清迅速採血用チューブ技術RAPClotを日本で製造・販売する独占契約を締結しました。このような契約により、市場における製品の入手可能性が高まり、予測期間中の市場成長が期待されます。

しかし、不衛生な輸血による感染症のリスクが市場成長の難点となっています。

採血用チューブ市場の動向

予測期間中、EDTAチューブセグメントが大きな市場シェアを占める見込み

EDTAチューブは臨床血液学や各種血球検査機器に広く使用されています。EDTAは血液中のカルシウムと結合し、血液を凝固させないようにすることで機能します。これらのチューブは、アブレーション治療や輸血など、ほとんどの血液学的処置に使用されます。主に全血球算定に使用されます。2021年10月にNational Library of Medicineに掲載された調査論文によると、血小板EVの濃度安定化に関して、EDTAはクエン酸塩よりも抗凝固剤として優れています。さらに、1回の凍結融解サイクルにおける血小板EVの安定性はどちらの抗凝固剤でも同等であるため、EV研究のためのバイオリポジトリーを確立するための抗凝固剤としてEDTAが推奨されています。

このセグメントの主要なシェアは、糖尿病などの広範な疾患とともに高齢化人口が増加していることに起因しています。糖尿病の有病率は近年増加しており、有病率は今後さらに増加すると予測されています。例えば、国際糖尿病連合による2021年12月の報告によると、2021年には約5億3,700万人の成人(20~79歳)が糖尿病を患っています。糖尿病患者の総数は、2030年には6億4,300万人、2045年には7億8,300万人に増加すると予測されています。様々な慢性疾患を患う患者数の増加は、血液検査の需要を増加させ、研究セグメントの成長に貢献すると思われます。

同様に、主要市場プレーヤーによる発売も市場成長のもう一つの要因です。例えば、2022年5月、Tethis SpAは、リキッドバイオプシー分析用の初のユニバーサル血液サンプル調製装置See.dを発表しました。この革新的な技術は、採血の時点で血液サンプルの調製を完全に自動化・標準化します。細胞画分は、CTCを含む希少細胞検出のために、独自のナノコーティングされたSBSスライド上で穏やかに安定化され、一方、血漿は無細胞成分の分析に利用できるようになります。See.dは、EDTAチューブに採取された新鮮血液を、採取後すぐに(4~6時間以内)処理するため、サンプルの完全性が最大限に保たれます。このような開発により、EDTA採血用チューブの使用と需要が促進され、市場開拓に寄与することが期待されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は予測期間を通じて大きな成長が見込まれます。市場成長の要因としては、主要プレイヤーの存在、事故や慢性疾患の有病率の高さ、ヘルスケアインフラの確立などが挙げられます。米国は、支援的なヘルスケア政策、患者数の多さ、ヘルスケア市場の開拓により、この地域で最大のシェアを占めています。

さらに、米国では、糖尿病、甲状腺、血液検査を必要とするその他の疾患など、慢性疾患の負担が増加していることも、調査対象市場を押し上げると思われます。糖尿病の研究開発のためのカナダ政府からの投資の増加に準拠した糖尿病の発生率の増加は、同国における調査市場の成長を推進しています。例えば、2021年8月に発表されたカナダ政府のプレスリリースによると、糖尿病はカナダ人に影響を与える主要な慢性疾患の1つであり、人口の8.8%に当たる300万人以上のカナダ人が糖尿病と診断され、2021年8月現在、カナダ成人の6.1%が糖尿病を発症するリスクが高いです。糖尿病患者の増加問題を支援するため、カナダの2021年度予算は、糖尿病の研究、サーベイランス、予防、糖尿病の国家的枠組みの開発への新たな投資を提案しました。その一環として、カナダ保健研究所(CIHR)を通じてカナダ政府の広報担当者は、糖尿病を撲滅するためのJDRFとCIHRのパートナーシップに再投資する予定で、研究効果総額3,000万米ドルのために1,500万米ドルを上限に投資しました。このように、糖尿病の罹患率の増加と政府投資は、カナダにおける研究市場の成長を促進すると予想されています。

しかし、同国の主要市場プレーヤーが獲得した様々な戦略が市場成長を予想しました。例えば、2022年7月、Rhinostics社は、少量採血に特化した特許出願中のVERIstic採血デバイスの発売により、自動サンプル採取技術を導入しました。

したがって、上記のすべての要因を考慮すると、市場は予測期間中に健全な成長を示すと予想されます。

採血用チューブ業界の概要

採血用チューブ市場は適度な競争があり、複数の大手企業で構成されています。現在市場を独占している企業には、Becton, Dickinson and Company、Greiner AG、Qiagen NV、FL MEDICAL SRL、AdvaCare Pharma、Sarstedt AG &Co.、Narang Medical Limitedなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 手術件数と事故の増加

- 疾病の蔓延に伴う高齢化人口の増加

- 世界の採血・献血プログラムの増加

- 市場抑制要因

- 不衛生な輸血による感染症のリスク

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 血清分離チューブ

- EDTAチューブ

- 血漿分離チューブ

- 迅速血清チューブ

- その他の製品タイプ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Becton, Dickinson and Company

- Greiner AG

- Qiagen NV

- F.L. Medical SRL

- AdvaCare Pharma

- Narang Medical Limited

- Sarstedt AG & Co KG

- Hindustan Syringes & Medical Devices Ltd

- Terumo Corporation

- DWK Life Sciences

- RAM Scientific

第7章 市場機会と今後の動向

The Blood Collection Tubes Market size is estimated at USD 2.39 billion in 2025, and is expected to reach USD 3.33 billion by 2030, at a CAGR of 6.85% during the forecast period (2025-2030).

The pandemic had an effect on the market. In February 2021, the WHO emphasized the importance of being prepared and responding quickly and outlined key actions and measures that the blood services should take to mitigate the potential risk to the safety and sufficiency of blood supplies during the pandemic. Additionally, as per an April 2022 study published in the National Library of Medicine blood centers should focus more on launching initiatives and policies that would increase their countries' blood supply as the virus has no direct threat to blood safety. Similarly, initiatives such as increasing product launches such as blood collection home tubes are expected to increase market growth during the forecast period. For instance, in December 2021, Ethos Laboratories launched Tru-Immune, a finger prick, self-collection kit for its COVID-19 neutralizing antibody test. Such product launches provide a safe procedure of blood collection at home which is expected to increase the adoption of such products, however, currently as the pandemic has subsided the market has lost some traction, thus the market is expected to have a stable growth during the forecast period of the study.

The major factor attributing to the growth of the market is the increase in the geriatric population and the increasing incidence of chronic diseases. Furthermore, the rising number of surgeries due to various conditions and accidents boosts the market. The rising burden of these diseases is expected to have a significant impact on the market as with the rising burden of inflammatory and infectious diseases, the awareness about these diseases is also increasing in demand for blood collection which is expected to have a significant and positive impact on the segment's growth. For instance, as per the October 2022 update of the World Health Organization, the incidence of tuberculosis (TB) was estimated to be around 10.6 million people in 2021, globally, of which 1.2 million were children. Similarly, the increasing number of surgeries is expected to increase the market growth. According to the Organization for Economic Co-operation and Development updated in August 2022, the number of surgeries (in thousand) performed in some European countries such as Portugal, Denmark, Ireland, and Norway in 2021 include 94.87, 49.33, 32.84, 21.5., respectively. Such a huge number of surgeries in developed European countries will lead to increased demand of blood collection tubes, driving market growth. Thus, the abovementioned factors are expected to increase the market growth.

Furthermore, agreements between market players are another factor in market growth. For instance, in November 2021, Q-Sera Pty Ltd entered an exclusive agreement with Terumo Corporation to manufacture and market Q-Sera's RAPClot rapid serum blood collection tube technology in Japan. Such agreements are expected to increase the availability of products in the market which is expected to increase market growth over the forecast period.

However, the risk of acquiring infections due to unhygienic blood transfusion is a drawback of market growth.

Blood Collection Tubes Market Trends

EDTA Tubes Segment is Expected to Hold a Significant Market Share Over the Forecast Period

EDTA Tube is widely used in clinical hematology and various kinds of blood cell test instruments. EDTA functions by binding calcium in the blood and keeping the blood from clotting. These tubes are used for most hematology procedures like ablation therapy, blood transfusions, etc. It is majorly used for a complete blood count. A research article published in the National Library of Medicine in October 2021, shows that EDTA is superior to citrate as an anticoagulant concerning stabilization of the concentration of platelet EVs. Moreover, because the stability of platelet EVs is comparable for both anticoagulants during a single freeze-thaw cycle, EDTA is recommended as an anticoagulant to establish biorepositories for EV research.

The major share of the segment can be attributed to the increase in the aging population along with widespread diseases, such as diabetes. The prevalence of diabetes has increased in recent years, and it is predicted that prevalence will increase further in the future. For instance, as per the December 2021 report by the International Diabetes Federation, approximately 537 million adults (20-79 years) lived with diabetes in 2021. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The rising number of patients suffering from various chronic disorders will increase the demand for blood testing, which will help grow the studied segment.

Similarly, launches by key market players are another factor in market growth. For instance, in May 2022, Tethis SpA released See.d, the first universal blood sample preparator for liquid biopsy analysis. This innovative technology performs a completely automated and standardized preparation of a blood sample at the point of blood collection. Cellular fraction is gently stabilized on proprietary, nanocoated SBS slides for rare cell detection, including CTCs, while plasma is made available for the analysis of cell-free content. See.d processes fresh blood collected in EDTA tubes shortly after collection (within 4 to 6 hours), favoring maximum sample integrity. Such developments are expected to fuel the usage and demand for EDTA blood collection tubes, thereby contributing to market growth.

North America is Expected to Have a Significant Market Share Over the Forecast Period

North America is expected to witness significant growth throughout the forecast period. The market growth is due to the factors such as the presence of key players, the high prevalence of accidents and chronic diseases in the region, and established healthcare infrastructure are some of the key factors accountable for its large share in the market. The United States has the maximum share in this region due to supportive healthcare policies, the high number of patients, and a developed healthcare market.

Furthermore, the rising burden of chronic diseases in the United States, such as diabetes, thyroid, and other diseases requiring blood tests, will boost the studied market. The increasing incidence of diabetes in compliance with the rising investment from the Canadian government for diabetes research and development is propelling the growth of the studied market in the country. For instance, as per a press release by the government of Canada published in August 2021, diabetes is one of the major chronic diseases affecting Canadians where over 3 million Canadians, or 8.8% of the population were diagnosed with diabetes and 6.1% of Canadian adults were at high risk of developing diabetes as of August 2021. To aid the issue of increasing cases of diabetes, Canada's Budget 2021 proposed new investments in diabetes research, surveillance, prevention, and the development of a national framework for diabetes. As part of this, the spokesperson of the government of Canada through the Canadian Institutes of Health Research (CIHR) is planning to recommit to the JDRF-CIHR partnership to Defeat Diabetes and invested up to USD 15 million for a total research impact of USD 30 million. Thus, the increasing incidence of diabetes and government investments are anticipated to drive the studied market growth in Canada.

However, various strategies acquired by the key market players in the country anticipated market growth. For instance, in July 2022, Rhinostics introduced automated sample collection technologies with the launch of the patent-pending VERIstic collection device focused on small volume blood collection.

Thus, considering all the factors mentioned above, the market is expected to witness healthy growth over the forecast period.

Blood Collection Tubes Industry Overview

The blood collection tube market is moderately competitive and consists of several major players. Some companies currently dominating the market are Becton, Dickinson and Company, Greiner AG, Qiagen NV, FL MEDICAL SRL, AdvaCare Pharma, Sarstedt AG & Co., Narang Medical Limited, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in the Number of Surgical Procedures and Accidents

- 4.2.2 Increase in Aging Population Coupled with Widespread of Diseases

- 4.2.3 Increasing Blood Collection and Blood Donation Programs Globally

- 4.3 Market Restraints

- 4.3.1 Risks of Acquiring Infections Due to Unhygienic Blood Transfusion

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Serum Separating Tubes

- 5.1.2 EDTA Tubes

- 5.1.3 Plasma Separation Tubes

- 5.1.4 Rapid Serum Tubes

- 5.1.5 Other Product Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Becton, Dickinson and Company

- 6.1.2 Greiner AG

- 6.1.3 Qiagen NV

- 6.1.4 F.L. Medical SRL

- 6.1.5 AdvaCare Pharma

- 6.1.6 Narang Medical Limited

- 6.1.7 Sarstedt AG & Co KG

- 6.1.8 Hindustan Syringes & Medical Devices Ltd

- 6.1.9 Terumo Corporation

- 6.1.10 DWK Life Sciences

- 6.1.11 RAM Scientific