|

市場調査レポート

商品コード

1439808

眼圧計:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Global Tonometer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 眼圧計:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

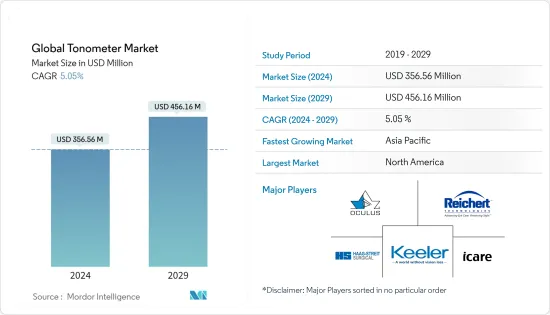

眼圧計の世界市場規模は2024年に3億5,656万米ドルと推定され、2029年には4億5,616万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5.05%で成長する見込みです。

眼圧計市場はCOVID-19の大流行による影響を受けており、その主な原因はいくつかの国による封鎖にあります。眼科センターや病院への受診は激減し、緊急処置のみが行われています。さらに、パンデミックのために各社が機器の生産を縮小または一時停止しているため、新しい機器の供給が一時的に滞っています。こうした状況は、すでに市場プレイヤーの企業収益に影響を及ぼしています。例えば、世界的リーダーの一社であるアルコン社は、2020年第2四半期の報告書で減収を報告しています。同社の2020年第2四半期の企業収益は報告ベースで36%減少しました。また、2020年6ヶ月間の企業収益は、2019年6ヶ月間の36億4,000万米ドルに対し、30億2,000万米ドルでした。なお、British Journal of Surgeryに掲載された研究によると、2020年5月、COVID-19による病院サービスの混乱がピークとなる12週間を基準にすると、全世界で約2,840万件の選択手術がキャンセルまたは延期されました。国際コンソーシアムが2020年5月に実施した調査によると、COVID-19の流行により、インドで予定されていた58万件以上の手術がキャンセルまたは延期される可能性があります。上記の要因により、眼圧計の市場開拓は今後数カ月でマイナスに転じる可能性があります。

調査された市場の成長をもたらす主な要因は、緑内障の発生率の増加、緑内障を発症しやすい老人人口と糖尿病患者の増加です。

Glaucoma Research Foundation(2020)によると、約300万人のアメリカ人が緑内障を患っており、アフリカ系アメリカ人の失明の19%は開放隅角緑内障に関連しています。2020年6月にARVOジャーナルに掲載されたGabriela Thomassinyらの調査によると、緑内障はラテンアメリカにおける失明の主な原因の1つです。ラテンアメリカ人は緑内障を発症するリスクが高いです。この地域では、罹患人口の約75%が診断されていないです。メキシコはラテンアメリカで2番目に人口の多い国です。研究結果によると、メキシコでは2030年には緑内障患者数は250万人になり、2040年には300万人、2050年には340万人に増加する可能性が高いです。回避可能な視力低下を防ぐための早期診断と眼圧の定期的なモニタリングに対する患者の意識の高まりが、近い将来の市場を牽引すると予想されます。

したがって、緑内障の発生率の高さが眼圧計の需要を促進すると予想されます。眼圧計に有利な償還政策を提供することで、病院や診療所での採用率が高まると期待されています。

眼圧計の市場動向

市場セグメンテーションは予測期間中に大きな市場シェアを占める見込み

アプラナシオン・トノメトリー検査は眼圧を測定します。この検査では、額と顎を支え、患者の角膜に静かに接触する小さな先端の平らなコーンを備えたスリットランプを使用します。この検査では基本的に、角膜の一部を一時的に平らにするのに必要な力の大きさを測定します。緑内障の診断に用いられます。

アプラネーション・トノメトリーでは、角膜を平らにし、アプラネーションする力または平らにする面積を変化させて眼圧を測定します。眼圧計には、ゴールドマン眼圧計、非接触眼圧計、眼反応分析装置の3種類があります。拍動眼圧計の利点には、眼圧評価の臨床標準法としてほぼ普遍的に受け入れられていること、検査技師の立場から使いやすいこと、ほとんどの患者に受け入れられることなどがあります。

さらに、Carl Zeissなどの企業は、ゴールドマン教授が導入した原理に基づいて設計された眼圧計(AT 020およびAT 030)を提供しており、眼圧の正確な測定が可能で、眼圧測定のゴールドスタンダードとなっています。眼圧測定は、複数の眼疾患、特に緑内障の診断と管理において極めて重要な要素です。

市場プレーヤーは、市場シェアを拡大するために、製品の発売や新興国開拓など様々な戦略を採用しています。例えば、2021年11月、タカギはスリットランプと併用する機能を持ち、有意な均一感を提供するアプラネーション眼圧計AT-2を発売しました。このアプラナシオン眼圧計は、迅速、安全、正確な眼圧測定を提供すると期待されています。拍動眼圧計の使用頻度の増加は、市場開拓を積極的に支援すると期待されています。

拍動眼圧計の利点とは別に、このセグメントの成長を後押しする要因は、緑内障の有病率の増加であり、これは緑内障になりやすい老人人口と糖尿病人口の増加に後押しされています。

北米が市場を独占し、予測期間も同様と予測される

北米は予測期間を通じて市場全体を支配すると予想されます。市場成長の要因は、主要プレイヤーの存在、同地域における緑内障の高い有病率、確立されたヘルスケアインフラなどです。

米国では、COVID-19パンデミックの間、緑内障研究財団は、パンデミックの間、視力を保護するための措置を講じることがより困難であったと述べています。さらに、COVID-19パンデミックは、通常の診察予約のキャンセルや遅延など、多くの課題を提示しました。米国では、眼科医療従事者が患者を安全に診察できるよう、診察室や処置に多大な工夫を凝らしています。

さらに、政府の有益な取り組みや研究提携の増加が、市場の成長を促進すると予想される要因の一部です。この地域では、ヘルスケア政策への支援、患者数の多さ、ヘルスケア市場の発展により、米国が最大のシェアを占めています。Brighfocus.orgによると、緑内障は米国経済に毎年28億6,000万米ドルの損害を与えており、12万人以上が緑内障で失明しており、失明症例全体の9~12%を占めています。さらに、最近の製品発売、検眼医の増加、利用可能な治療オプションに関する認知度の向上が市場の成長を後押ししています。例えば、2020年1月、Revenio Groupの眼圧検査用次世代眼圧計Icare ic200が米国で販売承認を取得しました。

米国労働統計局の2020年の統計によると、米国における検眼士の雇用は43,300人でした。視能訓練士の雇用は2020年から2030年にかけて9%増加すると予測されており、これは全職種の平均よりも速いです。これは、様々な治療法の採用が増加していることを意味します。この統計は、この国における患者数の増加と可処分所得の増加が、この地域の市場成長を後押ししていることを示しています。

眼圧計産業の概要

眼圧計市場は適度に統合されています。主要企業は、世界市場での地位を確保するために、M&Aなど様々な戦略的提携を行っています。現在市場を独占している企業には、Keeler Ltd、Carl Zeiss、Icare Finland Oy、Ametek Inc.、Oculus、Kowa American Corporation、Nidek、Rexxam、Canon、Haag-Streit Groupなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 緑内障罹患率の増加

- 老年人口および糖尿病人口の増加

- 眼科検診キャンプや緑内障啓発プログラムの増加

- 市場抑制要因

- 接触型眼圧計の感染リスクと非接触型眼圧計の精度不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術別

- アプラネーショントノメトリー

- インデンテーショントノメトリー

- リバウンドトノメトリー

- その他の技術

- 携帯タイプ別

- 卓上型

- ハンドヘルド

- エンドユーザー別

- 病院

- 眼科センター

- タイプ別

- 直接

- 間接

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Halma plc(Keeler Ltd)

- Carl Zeiss Meditec AG

- Revenio Group PLC(iCare Finland OY)

- AMETEK Inc.(Reichert Technologies)

- Oculus Inc.

- Kowa American Corporation

- Nidek Co. Ltd

- Rexxam Co. Ltd

- Canon Medical Systems Corporation

- Metall Zug Group(Haag-Streit Group)

- Belrose Refracting Equipment

- Tomey Corporation

- 66 Vision Tech Co. Ltd

- Topcon Corporation

第7章 市場機会と今後の動向

The Global Tonometer Market size is estimated at USD 356.56 million in 2024, and is expected to reach USD 456.16 million by 2029, growing at a CAGR of 5.05% during the forecast period (2024-2029).

The tonometer market has been impacted by the COVID-19 outbreak, which is majorly attributed to the lockdown placed by several countries. The visits to ophthalmic centers or hospitals have reduced drastically, and only emergency procedures are being performed. Moreover, the supply of newer devices is temporarily obstructed due to the pandemic, as companies have reduced or paused the production of devices. The situation is already affecting the company revenues of the market players. For instance, one of the global leaders in the world, Alcon Inc., reported decreased revenue in the Q2 2020 report. The company's revenue decreased by 36% on a reported basis in Q2 2020. Also, for the six months ended 2020, the company revenue was USD 3,020 million compared to the USD 3,640 million in the six months ended 2019. In addition, according to the study published in the British Journal of Surgery, in May 2020, based on a 12-week period of peak disruption to hospital services due to COVID-19, around 28.4 million elective surgeries worldwide were canceled or postponed. More than 580,000 planned surgeries in India may be canceled or delayed as a result of the COVID-19 pandemic, according to a study conducted by an international consortium in May 2020. The above factors can lead to negative market development for tonometers in the next few months.

The major factor attributing to the growth of the studied market is the increasing incidence of glaucoma and the rising geriatric population and diabetic patients who are more prone to developing glaucoma.

According to Glaucoma Research Foundation (2020), about 3 million Americans are living with glaucoma, and 19% of all blindness among African Americans is associated with open-angle glaucoma. According to a research study by Gabriela Thomassiny et al., published in ARVO Journal in June 2020, glaucoma is one of the leading causes of blindness in Latin America. Latin Americans have an increased risk of developing glaucoma. In this region, around 75% of the affected population is undiagnosed. Mexico is the second most populated country in Latin America. The study results found that in Mexico, in 2030, the number of people with glaucoma will likely be 2.5 million, increasing to 3 million in 2040 and 3.4 million in 2050. Increasing awareness among patients about early diagnosis and regular monitoring of intraocular pressure (IOP) to prevent avoidable vision loss is anticipated to drive the market in the near future.

Therefore, the high incidence of glaucoma is expected to drive the demand for tonometer devices. Providing favorable reimbursement policies for tonometers is expected to aid its adoption rate in hospitals and clinics.

Tonometer Market Trends

The Applanation Tonometry Segment is Expected to Hold a Significant Market Share Over the Forecast Period

The applanation tonometry test measures the fluid pressure in the eye. The test involves using a slit lamp equipped with forehead and chin supports and a tiny, flat-tipped cone that gently comes into contact with the patient's cornea. The test essentially measures the amount of force needed to flatten a part of the cornea temporarily. It is used in the diagnosis of glaucoma.

In applanation tonometry, the cornea is flattened, and the IOP is determined by varying the applanating force or the area flattened. There are three types of applanation tonometers, Goldmann applanation tonometer, non-contact tonometer, and ocular response analyzer. The advantages of applanation tonometry include its almost universal acceptance as the clinical standard method of IOP assessment, ease of use from the technician's perspective, and acceptability for most patients.

Moreover, companies, such as Carl Zeiss, offer applanation tonometers (AT 020 and AT 030) that were designed on the principle introduced by Professor Goldmann, which provide precise measurements of intraocular pressure (IOP) and represents the gold standard in tonometry. Measurement of IOP forms a crucial component in the diagnosis and management of multiple ocular conditions, especially glaucoma.

Market players are adopting various strategies such as product launches and developments to increase their market shares. For instance, in November 2021, Takagi launched AT-2 Applanation Tonometer, which has the capability to be used with slit lamps and provides a significant sense of uniformity. This applanation tonometer is expected to provide rapid, safe, and accurate intraocular pressure measurement. Increased usage of applanation surface is expected to aid the market development in a positive manner.

Apart from the advantages of the applanation tonometer, the factor boosting the segment growth is the increasing glaucoma prevalence, fueled by the increasing geriatric population and the diabetic population who are more prone to glaucoma.

North America Dominates the Market and is Expected to do the Same in the Forecast Period

North America is expected to dominate the overall market throughout the forecast period. The market growth is due to the factors such as the presence of key players, the high prevalence of glaucoma in the region, and the established healthcare infrastructure.

During the COVID-19 pandemic, in the United States, the Glaucoma Research Foundation stated that taking steps to protect vision was more challenging during the pandemic. Moreover, the COVID-19 pandemic has presented many challenges, including cancelation or delay of regular medical appointments. In the United States, eye care professionals have gone to great lengths to make modifications to their offices and procedures to allow them to see patients safely.

Furthermore, beneficial government initiatives and an increase in the number of research partnerships are some of the factors expected to drive market growth. In this region, the United States has the maximum share due to supportive healthcare policies, the high number of patients, and a developed healthcare market. According to Brighfocus.org, glaucoma costs the United States economy USD 2.86 billion every year, and more than 120,000 are blind from glaucoma, accounting for 9% to 12% of all cases of blindness. Moreover, recent product launches, a growing number of optometrists, and increasing awareness regarding available treatment options are fueling the market growth. For instance, in January 2020, Revenio Group's Icare ic200, the next-generation tonometer for intraocular pressure screening, was granted marketing authorization in the United States.

According to the United States Bureau of Labor Statistics 2020, there were 43,300 optometrist jobs in the United States. Employment of optometrists is projected to grow 9% from 2020 to 2030, faster than the average for all occupations. This signifies the increasing adoption of various treatments. The statistics indicate that the increasing patient pool and increasing disposable revenue in this country are boosting the market growth of the region.

Tonometer Industry Overview

The tonometer market is moderately consolidated. The key players have been involved in various strategic alliances such as mergers and acquisitions to secure their positions in the global market. Some of the companies currently dominating the market are Keeler Ltd, Carl Zeiss, Icare Finland Oy, Ametek Inc., Oculus, Kowa American Corporation, Nidek Co. Ltd, Rexxam Co. Ltd, Canon, Haag-Streit Group, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Glaucoma

- 4.2.2 Increasing Geriatric and Diabetic Populations

- 4.2.3 Increasing Number of Eye Checkup Camps and Glaucoma Awareness Programs

- 4.3 Market Restraints

- 4.3.1 The Risk of Infection with Contact Tonometers and Lack of Accuracy in Non-contact Tonometers

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Technology

- 5.1.1 Applanation Tonometry

- 5.1.2 Indentation Tonometry

- 5.1.3 Rebound Tonometry

- 5.1.4 Other Technologies

- 5.2 By Portability Type

- 5.2.1 Desktop

- 5.2.2 Handheld

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ophthalmic Centers

- 5.4 By Type

- 5.4.1 Direct

- 5.4.2 Indirect

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.6 Brazil

- 5.5.7 Argentina

- 5.5.8 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Halma plc (Keeler Ltd)

- 6.1.2 Carl Zeiss Meditec AG

- 6.1.3 Revenio Group PLC (iCare Finland OY)

- 6.1.4 AMETEK Inc.(Reichert Technologies)

- 6.1.5 Oculus Inc.

- 6.1.6 Kowa American Corporation

- 6.1.7 Nidek Co. Ltd

- 6.1.8 Rexxam Co. Ltd

- 6.1.9 Canon Medical Systems Corporation

- 6.1.10 Metall Zug Group (Haag-Streit Group)

- 6.1.11 Belrose Refracting Equipment

- 6.1.12 Tomey Corporation

- 6.1.13 66 Vision Tech Co. Ltd

- 6.1.14 Topcon Corporation