|

市場調査レポート

商品コード

1689790

床用接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Floor Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 床用接着剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

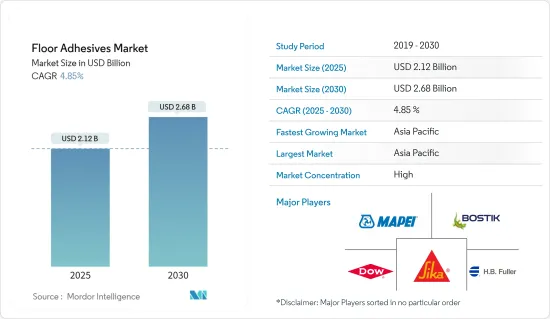

床用接着剤の市場規模は2025年に21億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.85%で、2030年には26億8,000万米ドルに達すると予測されます。

主なハイライト

- 急速に成長する世界の建設業界と、床用接着剤の汎用性、安全性、塗布の容易さが市場成長を牽引するとみられます。

- その反面、VOC排出による健康への悪影響が市場成長の妨げになる可能性があります。

- バイオベースの床用接着剤に対する需要の増加は、おそらく機会として機能すると思われます。

- アジア太平洋が世界市場を独占しており、最大の消費は中国、インド、日本によるものです。

床用接着剤市場の動向

住宅エンドユーザー産業セグメントからの需要の増加

- タイルおよび石材用接着剤は、住宅エンドユーザー産業セグメントで最も一般的に使用される接着剤タイプです。さらに、住宅セグメントは、調査した市場で最大かつ最も急成長しているセグメントです。

- 可処分所得の増加と相まって、中流階級の人口の増加は、中流階級の住宅セグメントの拡大を促進し、それによって床用接着剤の使用を増加しています。

- 世界銀行によると、世界の建設産業の価値は、2020年の22兆3,600億米ドルから2021年には27兆1,800億米ドルに増加しています。

- 中国とインドの住宅建設市場の拡大により、アジア太平洋地域で最も高い成長が見込まれています。この2つの地域は、2030年までに世界の中間層の43.3%以上を占めるようになると予想されています。インド政府は住宅にかかるGST税を12%から5%に引き下げました。この減税により、中間層向け住宅の建設市場が拡大する可能性があります。

- さらに、2021年10月、サンパウロ州住宅組合(Secovi-SP)は、ブラジルのサンパウロで5,555戸の新規住宅販売を記録しました。この数は、住宅に対する個人消費の増加により、増加する可能性が高いです。さらに、ブラジルの一戸建て住宅の動向は、今後の住宅建設業界を下支えすると思われます。

- メキシコの住宅着工件数と在庫水準は、連邦住宅補助金制度の大幅削減と、深刻な不況の引き金となったパンデミックにより、10年ぶりの低水準に達しました。社会的住宅プログラム(Programa de Vivienda Social)は、2021年には予算が179%増の2億米ドルとなり、建設支出を支えることになりました。さらに、利用しやすい融資制度や有利な住宅ローン制度は、同国の住宅建設に恩恵をもたらすと予想されます。

- 低価格住宅分野は、主に都市部や農村部の貧困層に手頃な価格の住宅を提供する政府の取り組みにより、着実に増加しています。

- 低価格住宅の建設における床用接着剤の消費量は、他のタイプの住宅に比べて比較的少ないです。世界中のさまざまな国が、他国からの難民にシェルターを提供しています。したがって、政府は難民に一時的または恒久的な低コストの住宅を提供しています。

市場を独占するアジア太平洋地域

- アジア太平洋地域は、床用接着剤の世界市場シェアを独占しています。中国、インド、ASEAN諸国などの国における建設活動の増加に伴い、床用接着剤の消費量は、この地域で増加しています。

- 中国政府は、経済をよりサービス指向の形態にリバランスする努力にもかかわらず、今後10年間で2億5,000万人が新たな巨大都市に移動するための準備を含む大規模な建設計画を展開しています。

- 中国国家統計局によると、中国の建設工事市場は2020年の23兆2,700億人民元(3兆3,400億米ドル)から2021年には25兆9,200億人民元(3兆7,200億米ドル)に増加します。

- 中国は世界最大の建設市場であり、世界の建設投資の20%を占めています。中国は、2030年までに約13兆米ドルを建築物に投じると予想されています。中国は継続的な都市化のプロセスを推進・進行中であり、2030年の目標率は70%です。

- インフラ・プロジェクトに対する政府の関心の高まりと、住宅・商業両セグメントに対する需要の急速な回復が予測されることから、建設部門は22年度に10.7%の成長が見込まれています。したがって、同国における建設活動の拡大は、床用接着剤の需要を増加させると予想されます。

- スマートシティプロジェクトや2022年までの万人向け住宅建設など、インド政府が実施する様々な政策は、低迷する建設業界に必要な刺激をもたらすと期待されています。さらに、不動産法、GST、REITといった最近の政策改革により、承認の遅れが減少し、今後数年間で建設セクターが強化されることが期待されます。

- 統計庁のデータによると、韓国の建設業者が2021年に獲得した建設受注は、堅調な国際需要により2桁増加しました。韓国統計庁によると、2021年に韓国内外の建設業者が集めた建設受注は総額2,459億米ドルとなり、2020年から31兆ウォン増加しました。

床用接着剤産業の概要

世界の床用接着剤市場は部分的に統合されています。主なプレーヤーは、シーカAG、MAPEI S.p.A、アルケマ・グループ(Bostik SA)、HBフラー・カンパニー、ダウなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 急成長する世界の建設業界

- 床用接着剤の汎用性、安全性、塗りやすさ

- 抑制要因

- VOC排出による健康への悪影響

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 樹脂タイプ

- エポキシ

- ポリウレタン

- アクリル

- ビニール

- その他の樹脂タイプ

- 技術

- 水性

- 溶剤型

- その他の技術

- 用途

- タイル&石材

- カーペット

- 木材

- ラミネート

- 弾性フローリング

- その他の用途

- エンドユーザー産業

- 住宅

- 商業

- 工業用

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema Group(Bostik SA)

- Ashland

- Dow

- Forbo Holding AG

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- LATICRETE International Inc.

- MAPEI SpA

- Pidilite Industries Limited

- Sika AG

- Tesa SE

第7章 市場機会と今後の動向

- バイオベースの床用接着剤に対する需要の増加

目次

Product Code: 68260

The Floor Adhesives Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 2.68 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030).

Key Highlights

- The rapidly growing global construction industry and the versatility, safety, and ease of application of floor adhesives, are likely to drive market growth.

- On the flip side, hazardous health effects due to VOC emissions may hinder the market's growth.

- Increasing demand for bio-based floor adhesives will likely act as an opportunity.

- Asia-Pacific dominates the global market, with the largest consumption coming from China, India, and Japan.

Floor Adhesives Market Trends

Increasing Demand from Residential End-user Industry Segment

- Tile and stone adhesives are the most commonly used adhesive type in the residential end-user segment. Additionally, the residential segment is the largest and fastest-growing segment in the market studied.

- The rising middle-class population, coupled with the increasing disposable incomes, has facilitated an expansion in the middle-class housing segment, thereby increasing the use of flooring adhesives.

- According to the World Bank, the value of the global construction industry has increased from USD 22.36 trillion in 2020 to USD 27.18 in 2021.

- The highest growth is expected to be registered in the Asia-Pacific region, owing to China and India's expanding housing construction markets. These two regions are expected to represent over 43.3% of the global middle class by 2030. The Government of India reduced the GST taxes for housing from 12% to 5%. This tax redemption may increase the construction market for middle-class housing.

- Furthermore, in October 2021, Sao Paulo State Housing Union (Secovi-SP) recorded 5,555 new residential units sold in Sao Paulo, Brazil. The number is likely to rise, owing to the increase in consumer spending on residential housing units. Moreover, the growing trend for single-family housing in Brazil is likely support the residential construction industry in the upcoming period.

- Mexico's housing starts and inventory levels reached a 10-year low due to a sharp cut in the federal housing subsidy program and the pandemic that triggered a severe recession. The Programa de Vivienda Social, or social housing program, had a budget increase of 179% to USD 200 million in 2021, thus, supporting construction spending. Moreover, accessible loan facilities and favorable mortgage schemes are expected to benefit residential construction in the country.

- The low-cost housing segment is rising steadily, primarily due to government initiatives to provide affordable housing to the poor in urban and rural regions.

- The consumption of flooring adhesives in constructing low-cost houses is comparatively less than other types of houses. Various countries across the world are providing shelter to refugees from other countries. Hence, governments offer temporary or permanent low-cost housing to refugees.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominates the global floor adhesives market share. With growing construction activities in countries such as China, India, and ASEAN Countries, the consumption of floor adhesives is increasing in the region.

- The Chinese government has rolled out massive construction plans, including making provisions for the movement of 250 million people to its new megacities, over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

- The National Bureau of Statistics of China reports that the market for construction works in China increased from CNY 23.27 trillion (USD 3.34 trillion) in 2020 to CNY 25.92 trillion (USD 3.72 trillion) in 2021.

- The country has the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030.

- Because of the government's increased attention to infrastructure projects and the predicted rapid rebound in demand for both residential and commercial segments, the construction sector was expected to grow by 10.7% in FY22. Hence, the growing construction activities in the country are expected to increase the demand for floor adhesives.

- Various policies implemented by the Indian government, such as Smart City projects, Housing for All by 2022, etc., are expected to bring the needed impetus to the slowing construction industry. Moreover, recent policy reforms, such as the Real Estate Act, GST, and REITs, are expected to reduce approval delays and strengthen the construction sector over the next few years.

- According to statistical office data, construction orders won by South Korean builders in 2021 increased by double digits due to robust international demand. According to Statistics Korea, construction orders collected by local builders both at home and overseas totaled USD 245.9 billion in 2021, up by 31 trillion won from 2020.

Floor Adhesives Industry Overview

The global floor adhesives market is partially consolidated. The major players include Sika AG, MAPEI S.p.A, Arkema Group (Bostik SA), HB Fuller Company, and Dow.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Growing Global Construction Industry

- 4.1.2 Versatility, Safety, and Ease of Application of Floor Adhesives

- 4.2 Restraints

- 4.2.1 Hazardous Health Effects Due to VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Vinyl

- 5.1.5 Other Resin Types

- 5.2 Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Other Technologies

- 5.3 Application

- 5.3.1 Tile & Stone

- 5.3.2 Carpet

- 5.3.3 Wood

- 5.3.4 Laminate

- 5.3.5 Resilent Flooring

- 5.3.6 Other Applications

- 5.4 End-user Industry

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group (Bostik SA)

- 6.4.3 Ashland

- 6.4.4 Dow

- 6.4.5 Forbo Holding AG

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Jowat SE

- 6.4.9 LATICRETE International Inc.

- 6.4.10 MAPEI SpA

- 6.4.11 Pidilite Industries Limited

- 6.4.12 Sika AG

- 6.4.13 Tesa SE

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Bio-based Floor Adhesives