|

市場調査レポート

商品コード

1851203

医療用画像処理ワークステーション:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)Medical Imaging Workstations - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療用画像処理ワークステーション:市場シェア分析、産業動向&統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

概要

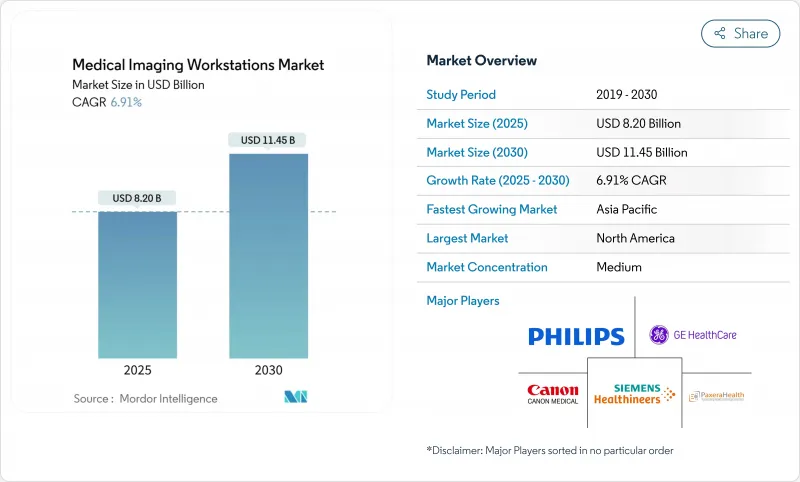

医療用画像処理ワークステーション市場規模は2025年に82億米ドルと推定・予測され、予測期間(2025-2030年)のCAGRは6.91%で、2030年には114億5,000万米ドルに達すると予測されます。

買い替えサイクルの高速化、企業向け画像アーカイブの移行、マルチモダリティ手技の複雑化などが、高度な可視化プラットフォームに対する需要を押し上げています。FDAによるコンピュータ支援検出ソフトウェアのクラスIIへの再分類などの規制の明確化により、技術革新のリードタイムが短縮され、参入障壁が低下しています。ベンダーは現在、AIに対応した設計と、オンプレミスのハードウェアコストを削減するクラウドホスト型の提供モデルを優先しており、このアプローチは病院の労働力不足への対応にも役立っています。北米は早期のAI導入と成熟した償還経路により優位を保っているが、アジア太平洋は大規模なデジタル化プロジェクトを背景に最速の利用拡大を記録しています。一方、半導体の供給制約がGPUの可用性を低下させ続け、ハイエンド構成のリードタイムを引き延ばし、一部のバイヤーはシンクライアントの代替を余儀なくされています。

世界の医療用画像処理ワークステーション市場動向と洞察

画像モダリティの急速な技術進化

フォトンカウンティングCT、全身MRIスクリーニング、コーンビーム乳房CT、自律超音波が、ワークステーションの更新サイクルごとに計算の上限を引き上げています。フォトンカウンティングスキャナは、放射線被ばくを80%も削減する一方で、生データ量を4倍に増加させ、リアルタイムの3D再構成をサポートするGPUを要求しています。GEヘルスケアとNVIDIAのコラボレーションは、ベンダーがいかにAI推論を画像取得層に組み込んでいるかを示しています。PrenuvoのAI対応全身MRIプラットフォームは、多臓器解析へのシフトを強化し、より高いスループット、より大きなキャッシュ、マルチモニター人間工学を備えたワークステーションの設計をベンダーに迫っています。

新興市場における画像処理件数の増加

アジア太平洋地域におけるCTおよびMRIの継続的な導入プログラムにより、視覚化のアップグレードに対する後続需要が発生。人口動態の高齢化により、特に高度な後処理に依存する腫瘍や心臓の画像処理において、一人当たりのスキャン率が上昇。キヤノンメディカル社のインド戦略は、中所得国へのメーカー各社の広範な軸足を示すものであり、保健省はハードウェアの更新サイクルと並行して、画像アーカイブの展開に資金を提供しています。エチオピアでは、Teleradiologyの導入後、患者の待ち時間が71%短縮されたことから、シンクライアント・ワークステーションが遠隔地の病院と不足している放射線科医をいかに結びつけるかが明らかになりました。そのため、スケーラブルなクラウドアクセスは、現場のITチームが不足している施設にとって、中心的な購入基準となります。

高価なワークステーションの初期費用とライフサイクルコスト

資本予算は依然として、サポート・インフラよりも直接患者をケアする機器を優先しています。総所有コストは、複数年のサービス契約やソフトウェアの更新を含めると、初期価格の2倍になることが多いです。小規模な施設では、認定整備済ハードウェアに目を向けるが、そのような掘り出し物には最新のGPUが搭載されていないことが多く、AIのパフォーマンスが低下します。サブスクリプション・ソフトウェアは、資本の高騰を平準化することができるが、7年間の累積料金は永久ライセンスを上回ることがあります。放射線治療における診療報酬の低下は、財務的な精査を拡大し、調達サイクルを引き延ばします。

セグメント分析

可視化ソフトウェアが2024年の売上高の57.83%を占め、特注のハードウェアではなくコードに機能が集約されていることを示しました。この優位性は、ベンダーがアルゴリズムのライセンスをディスプレイの購入から切り離し、迅速な無線アップデートを可能にすることで拡大します。サブスクリプションのAIセグメンテーション・プラグインは、継続的な収益源を生み出し、機能のリードタイムを短縮します。一方、ディスプレイユニットは、4Kと8Kの解像度が微小石灰化と肺結節のレビューにおける診断の不確実性を低減するため、CAGR最速の7.85%を記録します。EIZOのRadiForce RX670は、600万画素の解像度とUSB-Cドッキングを備え、ケーブルの散乱を最小限に抑える人間工学的な利点を備えています。

コンポーネントの収束も調達の指針となっています。シンクライアント・セットアップはローカルGPUから集中処理ノードへと価値をシフトさせ、自動キャリブレーションと快適な照明機能はディスプレイのASPを引き上げます。より多くの施設が遠隔読影を目指す中、病院情報システムに組み込まれたゼロフットプリント・ビューアは、プロプライエタリなグラフィック・カードへの最後の依存を取り除きます。その結果、医療用画像処理ワークステーション市場に占めるソフトウェアの割合は、どのハードウェア品目よりも急速に成長し続けると思われます。

コンピュータ断層撮影ワークステーションは、多臓器ユーティリティとフォトンカウンティングのアップグレードを背景に、2024年の売上高の30.73%を占める。この分野は、1台のCTビューワで外傷、腫瘍、心臓の症例に対応できるため、企業標準化の恩恵を受けています。しかし、マンモグラフィプラットフォームは、国の検診プログラムが拡大し、3Dトモシンセシスが一般的になるにつれて、CAGR最速の8.13%を記録します。コーンビーム乳房CTでは乳房圧迫がなくなるため、データ負荷がさらに高まり、ワークステーションの更新投資が正当化されます。

MRIワークステーションは、設置場所の制約を緩和するヘリウムフリー磁石の発売により勢いを増します。これまでハードウェアコンソールに取り付けられていた超音波検査は、生のシネループから自動計測値を抽出するクラウドベースの後処理を活用するようになります。核医学ワークステーションの技術革新はデジタル検出器にかかっており、リコン時間を短縮し、線量を削減すると同時に、全身PET撮影を可能にします。

地域分析

北米は、米国とカナダの医療機関がAIトリアージツールと自律的画像収集の早期導入者であり続けたため、2024年の売上高の37.81%を占めました。この地域は、高度な手技を償還するCPTコードが明確に定義されているため、病院はワークステーションへの投資を迅速に回収できるというメリットがあります。成熟したベンダーエコシステムはイノベーションサイクルを加速させ、300以上のFDA認可AIアルゴリズムがすでに統合可能です。

アジア太平洋地域は、現在進行中の病院建設、政府のクラウドヘルス・プログラム、急速な高齢化に牽引され、CAGR見通し8.33%を記録しました。中国は、県立病院と3次センターを結ぶ地方の遠隔画像診断ハブの規模を拡大し続けており、インドのアユシュマン・バラート計画は2次都市での診断量を増加させています。多くの新しい施設はレガシーPACSを回避し、初日からクラウドネイティブアーカイブを導入し、現地のITスタッフを最小限に抑えるシンクライアントアーキテクチャを好んでいます。

欧州では、European Health Data Spaceイニシアチブが国境を越えた画像交換を奨励し、病院を相互運用可能なビューアへと誘導しており、着実な拡大を見せています。ドイツとフランスでは、乳房検診の全国的な拡大が3Dマンモグラフィ・ワークステーションの採用を促し、英国NHSの近代化資金はAI支援CT肺検診の試験運用を支援しています。中東とアフリカでは、官民パートナーシップによって主要な画像診断センターに資金が供給されているが、政治的変動や為替レートの変動によって調達が遅れることがあります。ラテンアメリカでは、地域貿易協定によって診断用ハードウェアの輸入関税が引き下げられ、牽引力を増しているが、ブロードバンドの普及率が安定していないため、農村部でのシンクライアント導入には限界があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 画像モダリティの急速な技術進化

- 新興市場における画像処理件数の増加

- 医療費の増大と疾病負担の増加

- 加速するヘルスケアのデジタル化ー企業向けPACS/VNAの移行

- 新興経済国における病院・診断センターインフラの継続的イノベーション

- SaaS視覚化プラグインを可能にするベンダーニュートラルAPIエコシステム

- 市場抑制要因

- プレミアム・ワークステーションの高額な初期費用とライフサイクル費用

- 放射線科医/高度視覚化専門医の不足

- ゼロトラスト・サイバーセキュリティとHIPAAコンプライアンス費用の増大

- GPU鋳造能力の制約とサプライチェーンショック

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- 可視化ソフトウェア

- 表示ユニット

- その他

- モダリティ別

- コンピュータ断層撮影(CT)

- 磁気共鳴画像装置(MRI)

- 超音波

- マンモグラフィー

- その他

- 使用モード別

- シッククライアント・ワークステーション

- シンクライアント/ウェブ・ストリーミング・ワークステーション

- エンドユーザー別

- 病院

- 画像診断センター

- 専門クリニック

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- GE HealthCare

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Koninklijke Philips N.V.

- Hologic Inc.

- Carestream Health

- Sectra AB

- PaxeraHealth

- Agfa HealthCare

- Barco NV

- Fujifilm Healthcare

- Esaote SpA

- Intelerad Medical

- Aycan Medical

- EIZO Corp.

- Viztek

- eRAD Inc.