|

|

市場調査レポート

商品コード

1438443

ポリプロピレン:市場シェア分析、産業動向、成長予測(2024~2029年)Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリプロピレン:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

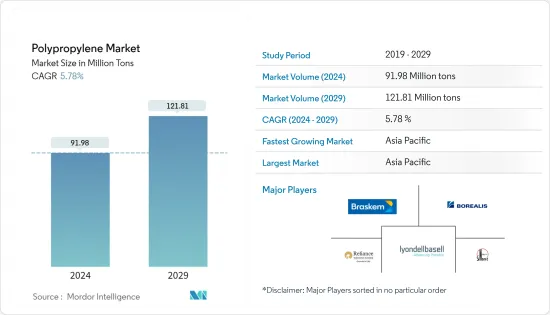

ポリプロピレンの市場規模は2024年に9,198万トンと推定され、2029年には1億2,181万トンに達すると予測され、予測期間(2024-2029年)のCAGRは5.78%で成長します。

ポリプロピレンの需要はCOVID-19により若干の減少が見られます。ポリプロピレンの需要が高い建設・自動車セクターでは大幅な減速が見られました。主要エンドユーザー産業の操業再開により、2022年には大幅に回復しました。

主なハイライト

- 短期的には、自動車の軽量化と燃費向上のためのプラスチック使用の増加、フレキシブル包装の需要拡大が市場を牽引する主な要因です。

- 一方、市場にはさまざまな代替製品が存在することが、予測期間中に対象業界の成長を抑制すると予想される主な要因です。

- 再生ポリプロピレンの動向の高まりは、将来的にはチャンスとして機能する可能性が高いです。

- アジア太平洋地域が世界全体の市場を独占しており、予測期間中も中国やインドなどの国々からの消費が最大で、市場を独占すると予想されます。

ポリプロピレン市場の動向

射出成形の需要増が用途別セグメントを支配

- ポリプロピレンは主に射出成形に使用され、この用途では主にペレットの形で入手できます。ポリプロピレンは成形が容易で、溶融粘度が低いため流動性に優れています。

- 射出成形技術は、電気および電子用途に広く使用されるプラスチックの製造に使用されます。これらのプラスチックは、電気・電子機器の製造に広く使用されています。

- ポリプロピレンは、その柔軟な用途の多さから、幅広い製品タイプに適しています。最も頻繁に使用される用途のひとつがリビング・ヒンジで、キャップなどの消費財によく使用される一体型のヒンジデザインです。このプロセスから作られる製品には、子供用玩具、スポーツ用品、クロージャー、自動車用途、食品トレイ、カップ、持ち帰り用容器、家庭用品、食器洗い機のような家電製品など、数え切れないほどあります。

- 世界有数の素材製造会社であるHUBS社によると、世界の射出成形生産量の35~40%をポリプロピレンが占め、ABS(25%)、ポリエチレン(15%)、ポリスチレン(10%)など他の素材がそれに続いています。

- 世界中で包装産業と化学加工産業が高成長していることから、射出成形にとって有利な市場シナリオが期待されています。急成長しているアジア太平洋地域への流通という地理的優位性により、射出成形パレットの消費量は大幅に増加する可能性があります。

- さらに、燃費を向上させるための自動車への軽量部品の採用は、予測期間中に調査された市場の需要に有利に働くと予想されます。

- 前述のすべての要因が市場の需要を押し上げると予想されます。

アジア太平洋地域が最速の成長を記録

- アジア太平洋地域のポリプロピレン市場は、中国やインドなどの国々が牽引して速いペースで成長しています。ポリプロピレンは自動車、消費者製品、エレクトロニクス、包装産業で広く使用されています。これらの産業の堅調な成長と政府の支援により、ポリプロピレンの需要は予測期間中に健全なペースで増加すると予測されます。

- 中国は世界最大の自動車市場であり、今後も年間販売台数と製造生産台数の両方で最大の市場となり、国内生産台数は2025年までに3,500万台に達すると予想されます。

- さらにOICAによると、中国の自動車メーカーは2021年に2,608万2,220台を生産し、2020年比で3%の成長を記録します。

- インドでは、インド包装産業協会(PIAI)によると、このセクターは年率22%から25%で成長しており、2025年には2,048億1,000万米ドルに達すると予想されています。インドの包装産業は輸出と輸入で実績を上げ、国内の技術と技術革新の成長を牽引し、様々な製造業に付加価値を与えています。

- 包装産業は、インドのポリプロピレン市場の巨大な成長を促進する触媒の役割を果たしています。さらに、同国では過去数年間、包装食品に対する大きな需要があり、これは予測期間中も続くと予想されるため、調査対象市場の需要を押し上げています。

- National Investment Promotion &Facilitation Agencyによると、自動車産業はインドのGDPの7.1%、製造業GDPの49%に寄与しています。さらに、Organisation Internationale des Constructeurs d'Automobilesによると、インドの自動車産業は439万9,112台を生産し、2020年に比べて30%近く増加しています。

- このような様々な産業の成長は、予測期間中、アジア太平洋地域のポリプロピレン市場を牽引すると予想されます。

ポリプロピレン産業の概要

世界のポリプロピレン市場は細分化されています。上位5社が生産能力で世界市場シェアの約35%を占めています。市場の主要企業には、China Petroleum &Chemical Corporation(SINOPEC)、LyondellBasell Industries Holdings BV、Borealis AG、Braskem、Reliance Industries Limitedなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車の軽量化と燃費向上のためのプラスチック利用の増加

- フレキシブル包装の需要拡大

- 抑制要因

- 代替製品の入手可能性

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 価格動向

- 輸出入動向

- 原料分析

- 技術スナップショット

第5章 市場セグメンテーション

- タイプ

- ホモポリマー

- コポリマー

- 用途

- 射出成形

- 繊維

- フィルム・シート

- その他の用途(押出コーティング、ブロー成形)

- エンドユーザー産業

- 包装

- 自動車

- 消費者製品

- 電気・電子

- その他のエンドユーザー産業(繊維、建設)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)分析

- 主要企業の戦略

- 企業プロファイル

- Borealis AG

- Braskem

- China National Petroleum Corporation

- China Petrochemical Corporation(SINOPEC)

- Daelim Co. Ltd

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- INEOS

- LG Chem

- Lotte Chemical Corporation

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.(Prime Polymer Co. Ltd)

- Reliance Industries Limited

- SABIC

- SIBUR International GmbH

- Sumitomo Chemical Co. Ltd

- Total Energies

第7章 市場機会と今後の動向

The Polypropylene Market size is estimated at 91.98 Million tons in 2024, and is expected to reach 121.81 Million tons by 2029, growing at a CAGR of 5.78% during the forecast period (2024-2029).

A slight decline in the demand for polypropylene has been observed due to COVID-19. A drastic slowdown was witnessed in the construction and automotive sector, where polypropylene is in high demand. With the resumption of operations in major end-user industries, it significantly recovered in 2022.

Key Highlights

- Over the short term, major factors driving the market studied are the increasing usage of plastics to reduce vehicle weight and enhance fuel economy and the growing demand for flexible packaging.

- On the other hand, the presence of different substitute products in the market is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- The increasing trends of recycled polypropylene are likely to act as an opportunity in the future.

- The Asia-Pacific dominated the market across the world and is expected to dominate in the forecast period, with the largest consumption from countries such as China and India.

Polypropylene Market Trends

Increasing Demand for Injection Molding to Dominate the Application Segment

- Polypropylene is majorly used for injection molding and is mostly available for this application in the form of pellets. Polypropylene is easy to mold, and it flows very well because of its low melt viscosity.

- Injection molding technology is used to produce plastics that are used extensively in electrical and electronic applications. These plastics are widely used in the manufacturing of electrical and electronic devices.

- Polypropylene is well-suited to a wide range of product types due to its numerous flexible uses. One of the most frequent applications is the living hinge, a one-piece hinged design typically used in consumer items such as caps. Innumerable products made from the process include children's toys, sporting goods, closures, automotive applications, food trays, cups, to-go containers, household goods, and appliances like dishwashers.

- According to HUBS, a globally leading material manufacturing company, polypropylene accounts for 35-40% of worldwide injection molding output, followed by other materials such as ABS (25%), polyethylene (15%), and polystyrene (10%).

- The high growth of the packaging and chemical processing industries across the world is expected to offer a favorable market scenario for injection molding. Owing to the geographical advantage of distribution to the rapidly growing Asia-Pacific region, the consumption of injection-molded pallets may increase drastically.

- Moreover, the adoption of lightweight components for the automobile to increase fuel efficiency is expected to favor the demand for the market studied in the forecast period.

- All the aforementioned factors are expected to boost the market's demand.

Asia-Pacific to Register the Fastest Growth

- The Asia-pacific polypropylene market is growing at a fast pace, driven by countries like China and India. Polypropylene is widely used in the automotive, consumer products, electronics, and packaging industries. With robust growth in these industries and government support, the demand for polypropylene is projected to increase at a healthy pace during the forecast period.

- China is the world's largest vehicle market and will continue to be the largest market by both annual sales and manufacturing output, with domestic production expected to reach 35 million vehicles by 2025.

- Moreover, as per the OICA, Chinese automotive manufacturers manufactured 26,082,220 vehicles in 2021, registering a growth of 3% compared to 2020.

- In India, according to the Packaging Industry Association of India (PIAI), the sector is growing at 22% to 25% per annum and is expected to reach USD 204.81 billion by 2025. The Indian packaging industry made a mark with its exports and imports, driving technology and innovation growth in the country and adding value to the various manufacturing sectors.

- The packaging industry is enacting the role of catalyst in promoting the huge growth of the polypropylene market in India. Furthermore, the country has been exhibiting a significant demand for packed foods in the past few years, which is expected to continue during the forecast period, thus boosting the demand for the market studied.

- As per the National Investment Promotion & Facilitation Agency, the automobile industry contributes 7.1% of India's GDP and 49% of its manufacturing GDP. Moreover, according to Organisation Internationale des Constructeurs d'Automobiles, the Indian automotive industry manufactured 4,399,112 vehicles, which is almost 30% more than in 2020.

- Such growth in various industries is expected to drive the market for polypropylene in the Asia-Pacific region during the forecast period.

Polypropylene Industry Overview

The global polypropylene market is fragmented in nature. The top five companies hold around 35% of the global market share in terms of production capacities. Some of the major players in the market include China Petroleum & Chemical Corporation (SINOPEC), LyondellBasell Industries Holdings BV, Borealis AG, Braskem, and Reliance Industries Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Plastics to Reduce Vehicle Weight and Enhance Fuel Economy

- 4.1.2 Growing Demand for Flexible Packaging

- 4.2 Restraints

- 4.2.1 Availability of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trends

- 4.6 Import-Export Trends

- 4.7 Feedstock Analysis

- 4.8 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Homopolymer

- 5.1.2 Copolymer

- 5.2 Application

- 5.2.1 Injection Molding

- 5.2.2 Fiber

- 5.2.3 Film and Sheet

- 5.2.4 Other Applications (Extrusion Coating, Blow moulding)

- 5.3 End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Consumer Products

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user industries (Textiles, Construction)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Borealis AG

- 6.4.2 Braskem

- 6.4.3 China National Petroleum Corporation

- 6.4.4 China Petrochemical Corporation (SINOPEC)

- 6.4.5 Daelim Co. Ltd

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 INEOS

- 6.4.9 LG Chem

- 6.4.10 Lotte Chemical Corporation

- 6.4.11 LyondellBasell Industries Holdings BV

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Mitsui Chemicals Inc. (Prime Polymer Co. Ltd)

- 6.4.14 Reliance Industries Limited

- 6.4.15 SABIC

- 6.4.16 SIBUR International GmbH

- 6.4.17 Sumitomo Chemical Co. Ltd

- 6.4.18 Total Energies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Recycled Polypropylene