|

市場調査レポート

商品コード

1910540

消防車:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Fire Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 消防車:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

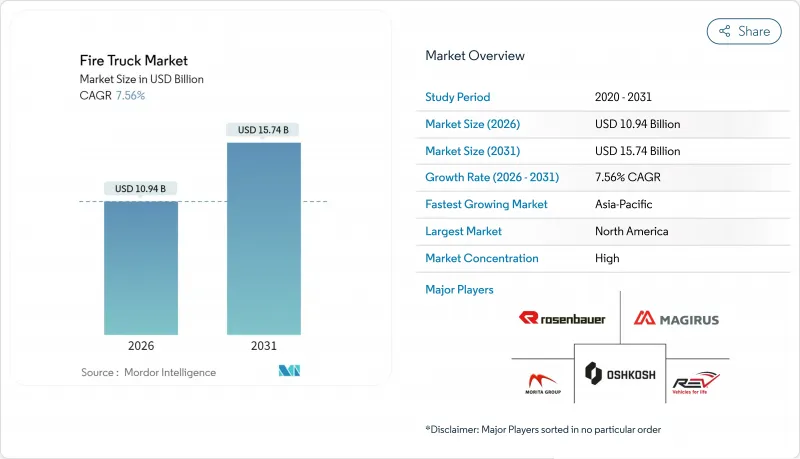

消防車市場は、2025年の101億7,000万米ドルから2026年には109億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR7.56%で推移し、2031年までに157億4,000万米ドルに達すると予測されています。

車両更新サイクル、電動化の進展、気候変動に伴う山火事リスクの増大が相まって、供給網のボトルネックが継続する中でも調達予算は増加傾向にあります。18~33ヶ月に及ぶ長い納期により、消防部門は新規納入を待つ間に整備プログラムの近代化を進めています。一方で、安全性と性能の向上は必須要件となり、消防車市場は高単価化を吸収し続けています。北米および欧州では、クリーン車両導入義務化と燃料・保守コストの削減効果を背景に、バッテリー式電気消防車の試作段階から量産段階への移行が進んでいます。一方、大規模山火事の増加により、山林火災対応の特殊仕様車への需要が高まっており、米国では主要メーカーの統合が進む中、規制当局による監視が強化されています。

世界の消防車市場の動向と洞察

厳格化する世界・地域の防火安全規制

新たなNFPA 1900規格は従来の消防車両規則を統合し、後方監視カメラ、LED照明、電気自動車対応の義務化を導入しました。規制当局は規定チェックリストから性能基準への移行により、OEMメーカーにイノベーションの余地を与えつつ、安全基準の底上げを図っています。調和された要件は国境を越えた消防車両の配備も支援し、世界の物流網を持つメーカーにとっての利点となります。しかしながら、コンプライアンスコストの増加により、中小メーカー間の統合が加速しており、消防車市場の高い集中傾向がさらに強まっています。

山火事の頻度と深刻度の増加

2024年の米国における山火事の延焼面積は770万エーカーに達し、総発生件数は減少したもの、過去10年間の平均を上回りました。規模が大きく、より激しい火災の発生により、走行中に補助ポンプを作動させることができるタイプ1の森林火災対応消防車(Wildland-Urban Interface)の受注が増加しています。山火事への備えを目的とした連邦および州の助成金は、専門機器への資金を投入し、需要を自治体の予算サイクルから切り離しています。火災シーズンはほぼ1年通年となり、消防署は年間を通じて準備態勢を維持する必要があり、消防車両の利用基準が引き上げられています。

次世代プラットフォームの高額な初期費用

RTXのような電動ポンプ車は100万米ドル近くと、同等のディーゼルエンジン車の約2倍の価格です。運用コスト削減により総所有コストは改善されますが、初期資本の障壁がボランティア消防署や地方消防署の導入を遅らせています。助成プログラムが費用を一部相殺します(ボルダー市は2台目の電動車両に相当額の外部資金を確保しました)が、資金力のある大都市圏以外では資金調達ギャップが依然として存在します。バッテリーコストは低下傾向にありますが、2027年以降に生産規模が大幅に拡大するまではディーゼル車との価格差が解消される見込みは薄いです。この二極化した状況は発展途上地域での移行を遅らせ、短期的には世界の消防車市場成長を抑制する要因となります。

セグメント分析

ポンプ車セグメントは2025年に消防車市場の36.28%を占め、2031年までCAGR7.62%で拡大が見込まれます。ポンプ車の進化により圧縮空気泡消火システムやモジュール式車体が追加され、消防署に多目的能力を提供しています。セグメント収益は早期電動化の恩恵も受けており、ローゼンバウアー社のRTXプラットフォームはディーゼルモデルと同等のポンプ性能を実現しています。消火栓ネットワークが未整備な地域ではタンク車が依然不可欠であり、はしご車プラットフォームは高層化が進む都市景観に対応しています。ブロント・スカイリフト社の230フィート(約70メートル)到達能力は20階建てビルをカバーします。

現代の救助車両には油圧救出工具やバッテリー駆動切断装置が組み込まれ、現場準備時間を短縮します。ポンプ車・タンク車・救助機能を統合した複合車両の需要も高まっており、調達予算と消防署の敷地面積を節約します。山林火災対応車両には、走行中に給水可能な補助ポンプが追加装備されており、急速に拡大する火災現場において極めて重要な機能です。空港消防車両(ARFF)は、厳格な加速性能と泡消火剤供給基準を義務付けるFAAパート139規格により、高価格帯が維持されています。漸進的な技術革新により、消防ポンプ車の市場シェアは予測期間を通じて3分の1以上を維持する見込みです。

2025年の売上高に占める住宅・商業施設向け防火設備の割合は56.90%で、消防車市場内最大の単一用途となりました。密集した都市中心部における消防サービスの義務化により受注は安定しており、新たな建築基準により、より高いポンプ能力と統合型除染システムを備えた設備への需要が継続的にシフトしています。

一方、山林火災分野は気候変動による火災シーズンの深刻化・長期化に伴い、CAGR7.86%で拡大しています。車両設計では、地上高の向上、車体下部の強化、走行中ポンプ作動機能(ポンプ・アンド・ロール)が採用され、隊員が停止せずに迫りくる炎に対処できるようになっています。山火事軽減プログラムに連動した連邦政府の補助金により、地方自治体の歳入が減少する時期でも調達予算は維持されています。産業用途では耐薬品性シールやクラスB危険物対応消火剤が求められ、空港ではFAAのフッ素フリー泡消火剤移行イニシアチブに基づくARFF車両の需要が継続しています。これらの変化は、多様なリスクプロファイルが消防車市場の進化を形作っていることを示しています。

地域別分析

北米は2025年の収益の33.95%を占め、成熟した緊急サービス資金と先進技術試験の恩恵を受けています。同地域は初期段階の電気消防車導入の大半を担い、将来の世界の普及パターンにおける指標としての役割を強化しています。進行中の連邦インフラプログラムは、20年以上経過した車両の代替に補助資金を提供し、発注パイプラインの持続性を維持しています。

アジア太平洋地域は7.72%のCAGRを記録し、中国・インド・東南アジアにおける都市化に対応すべく、自治体消防サービスを急速に拡充中です。中国の地方都市では、密集した高層地区向けに設計されたポンプ車や高所作業車への投資、消防署ネットワークの拡充に資金を配分しています。インドでは現地組立を優先する定期的な入札を実施し、世界のOEMと国内シャーシ供給業者との合弁事業を促進しています。バッテリー式商用車への関心が高まり、堅調なCAGRを示していることから、充電インフラが成熟すればゼロエミッション消防車両の市場が芽生える可能性が示唆されています。

欧州は依然として規模が大きいもの成長ペースは鈍化しており、車両増強よりも環境規制対応と更新需要が中心です。排出ガス規制の強化とNFPA準拠基準が調達基準に影響を与え、ユーロ6エンジンやハイブリッド駆動の採用を促進しています。中東・アフリカ地域では都市圏拡大と産業メガプロジェクトに連動した安定した受注が見られますが、南米の需要はマクロ経済の変動により抑制されています。これらの地域動向は、消防車市場を支える地理的多様性を浮き彫りにしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 厳格な世界的・地域的な防火安全規制

- 山火事の頻度と深刻度の増加

- 電気消防車の普及拡大

- 欧州における老朽化した自治体車両の急速な更新

- 都市部の高層建築増加が空中作業車需要を促進

- フリート最適化のためのIoTテレマティクス統合

- 市場抑制要因

- 次世代(EV/ハイブリッド)プラットフォームの高額な初期費用

- 半導体及びシャーシのサプライチェーン混乱

- 熟練した緊急車両オペレーターの不足

- 新興国における自治体の厳しい予算状況

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- ポンプ車

- タンカー

- 救助車両

- 高所作業車/プラットフォームトラック

- マルチタスク対応モジュラー式トラック

- 森林消防車

- 空港緊急対応車両(ARFF)

- 用途別

- 住宅・商業

- 産業・製造

- 空港

- 軍事

- 山林火災・森林火災

- 推進力別

- 内燃機関(ICE)

- ハイブリッド

- バッテリー電気自動車

- 燃料電池電気自動車

- エンドユーザー別

- 自治体消防署

- 産業施設消防隊

- 空港当局

- 防衛・軍事

- 契約・民間消防サービス

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Rosenbauer International AG

- Oshkosh Corporation(Pierce)

- REV Group

- Morita Holdings Corporation

- Magirus GmbH

- W.S. Darley & Co.

- KME(Kovatch Mobile Equipment)

- Sutphen Corporation

- Gimaex GmbH

- Albert Ziegler GmbH

- Bronto Skylift Oy

- NAFFCO

- Emergency One UK Ltd

- Weihai Guangtai

- Iturri Group

- Zhongtian Heavy Industry

- Sides S.A.

- BAI Brescia Antincendi International

- Fouts Bros Fire Equipment

- Alexis Fire Equipment