|

市場調査レポート

商品コード

1910514

脱毛治療製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Hair Loss Treatment Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 脱毛治療製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 146 Pages

納期: 2~3営業日

|

概要

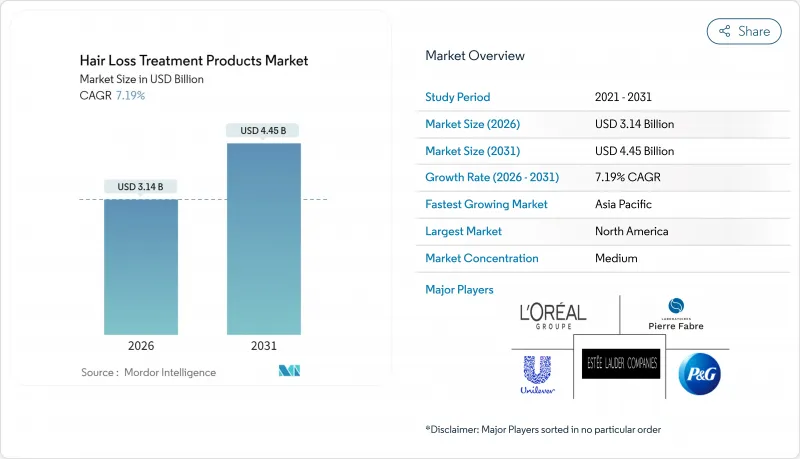

脱毛治療製品の市場規模は、2026年には31億4,000万米ドルに達すると予測されております。

2025年の29億3,000万米ドルから成長し、2031年には44億5,000万米ドルに達する見込みで、2026年から2031年にかけてCAGR7.19%で拡大すると見込まれております。

この拡大は、消費者セグメント全体で治療パラダイムを再構築している人口動態的圧力と技術的ブレークスルーの相乗効果を反映しています。2024年7月にFDAが重度の円形脱毛症治療薬としてデュルクソリチニブ(Leqselvi)を承認したことは、先進的な治療アプローチに対する制度的信頼の高まりを示す重要な規制上のマイルストーンとなりました。北米は先行者優位性を保持していますが、アジア太平洋地域は若年層人口、デジタル活用、革新能力を背景に、最も成長が著しい地域クラスターとしての地位を確立しています。競争の激しさは中程度であり、確立された消費者向けヘルスケア大手企業と、高度に標的化されたデリバリーシステムや個別化治療計画を導入するベンチャー資本支援のバイオテック新興企業が共存しています。成長機会は、オムニチャネル流通、複合療法キット、90日以内に目に見える効果を約束するプレミアム美容液を中心に集中しつつあります。

世界の脱毛治療製品市場の動向と洞察

高齢化人口

先進国市場における人口動態の変化は、治療需要のパターンを根本的に変えつつあり、50歳以上が最も急速に成長する消費者層となっています。MedlinePlus.govによれば、男性では男性型脱毛症、女性では女性型脱毛症として広く認識されているアンドロゲン性脱毛症は、男女双方にとって一般的な脱毛原因です。高齢層の可処分所得の増加と医療費支出傾向の高まりが、特に北米においてプレミアム製品の採用を促進しています。同地域では55歳以上の消費者が脱毛治療費の40%を占めています。最近の研究では、加齢に伴うホルモン変化が毛包の微小化を加速させ、従来の美容的アプローチを超えた標的治療介入の需要を生み出していることが示されています。この人口動態の変化は、寿命の延長期待と相まって、治療期間の延長とメーカーにとっての生涯顧客価値の向上につながっています。

科学技術の発展

バイオテクノロジーの飛躍的進歩により、精密な送達メカニズムと再生医療アプローチを通じて治療効果が革新されています。ナノテクノロジープラットフォームは毛包への標的浸透を可能にし、最近の臨床試験では従来の外用製剤と比較して3倍の生物学的利用能向上が実証されています。特定の脱毛経路を標的とするsiRNA治療薬の開発は、症状管理から根本原因への介入へとパラダイムシフトをもたらしています。ペラージュ・ファーマシューティカルズのPP405(現在第II相a試験中)は、新規シグナル伝達経路を通じて休眠状態の毛包幹細胞を活性化させることで、このアプローチを体現しています。成長因子を封入したマイクロニードルパッチやエクソソームベースの治療法を含む先進的な送達システムは、毛髪密度や太さの指標において測定可能な改善効果を示しています。こうした技術的進歩は特許出願の増加によって支えられており、2024年には韓国が世界の脱毛治療関連特許の相当なシェアを占めるなど、バリューチェーン全体での集中的な研究開発投資が反映されています。

偽造品および安全でない製品の蔓延

規制されていない製剤の市場拡散は、消費者の信頼を損ない、安全上の懸念を生み出し、正当な市場成長を阻害しています。特にオンラインマーケットプレースで蔓延する偽造製品には、非開示の有効成分や有害物質が含まれていることが多く、有害な反応を引き起こす可能性があります。規制当局は偽造脱毛治療薬の押収件数増加を報告しており、FDA(米国食品医薬品局)は処方薬レベルの成分を含みながら適切な表示がなされていない未承認製品について複数の警告を発しています。規制監視が限定的で価格感応度の高さから消費者が未検証の代替品に流れる新興市場では、この課題が特に深刻です。市場健全性の維持と正規メーカー全体のブランド評判保護のため、消費者教育の取り組みとサプライチェーン検証の強化が極めて重要となっています。

セグメント分析

シャンプーおよびコンディショナー製品は、2025年に87.65%の市場シェアを占めており、髪の健康維持を求める消費者にとって入門レベルの治療法であり、日常的に使いやすい利便性を反映しています。この優位性は、確立された流通ネットワーク、消費者の親しみやすさ、行動変容を必要とせずに既存のヘアケアルーティンに組み込める点に起因しています。しかしながら、美容液は2031年までCAGR8.02%で最も急速に成長するセグメントです。これは、治療効果を重視する消費者層に訴求する、ターゲットを絞った治療処方とプレミアムなポジショニングが牽引しています。美容液カテゴリーは、ナノテクノロジープラットフォームや、従来処方と比較して測定可能な効果改善を示す生物活性化合物など、先進的なデリバリー技術の恩恵を受けています。

その他の製品カテゴリー(オイル、グミ、錠剤など)は、多様な治療法や併用療法を求める消費者の嗜好に支えられ、着実な成長軌道を維持しています。経口製剤にはFDAの「栄養補助食品健康教育法」に基づく規制枠組みが適用される一方、外用オイルは天然成分動向と最小限の加工プロセスが評価されています。オーソモル・ヘアソリューションがバイカピル複合体を配合しドイツの薬局で導入されたなど、最近の製品導入は従来製品カテゴリーにおける継続的な革新を示しています。カプセル化技術や徐放性製剤の製造進歩は全カテゴリーで製品効果を高めており、経口サプリメントと専門的外用治療の両方に影響を及ぼしています。

2025年時点で女性消費者が市場シェアの70.45%を占め、2031年までCAGRが9.12%という最も高い成長可能性を示しています。これは美容基準の進化と、脱毛治療を求めることへの偏見の減少を反映しています。ソーシャルメディアの影響力は女性セグメントの拡大に特に強く作用しており、美容インフルエンサーが脱毛に関する議論を日常化し、予防的ケアアプローチを促進しています。女性セグメントは、化粧品的に洗練された製剤や、髪の健康と他の美容上の懸念を同時に解決する多機能製品など、より幅広い製品バリエーションの恩恵を受けています。臨床調査によれば、女性型脱毛症は50歳までにほとんどの女性に影響を及ぼしており、認知度向上に伴い大きな市場拡大の機会が生まれています。

男性消費者は成長率は低いもの、確立された治療パターンと医薬品介入への高い受容性により、依然として重要な市場存在感を維持しています。男性セグメントは、FDA承認医薬品や機器ベースの治療法など、臨床的に実証された治療法への強い選好を示しています。最近の動向として、ソーシャルメディアコンテンツや身だしなみ基準の変化の影響を受け、男性による包括的なヘアケアルーティンの採用が増加しています。TikTokやInstagramなどのプラットフォームにおけるユーザー生成コンテンツが、男性の脱毛関連トピックへの関与を促進しており、ブランドが男性向け製品ラインやマーケティング手法を拡大する機会を生み出しています。

地域別分析

北米地域は2025年に35.62%の市場シェアを占めており、先進的な医療インフラ、高い可処分所得、確立された治療受容パターンに支えられています。同地域は、製品の安全性を確保しつつイノベーションを促進する強固な規制枠組みの恩恵を受けており、FDAの承認プロセスは医薬品と医療機器ベースの治療の両方を支援しています。円形脱毛症治療薬デュルクソリチニブのFDA承認を含む最近の動向は、処方治療における継続的な革新を示しています。医療従事者への教育や治療受診行動を正常化する消費者向け直接マーケティングにより、消費者の認知度は高い水準を維持しています。

アジア太平洋地域は、可処分所得の増加、美容意識の高まり、医療アクセスの拡大を背景に、2031年までCAGR8.78%で最も急速に成長する地域として浮上しています。同地域は技術導入に強みを見せており、韓国は2024年に脱毛治療イノベーションの特許出願で世界をリードし、大きなシェアを占めています。アジア太平洋市場の消費者嗜好は天然成分と伝統医療の統合を好み、現代技術と植物性有効成分を組み合わせた製品に機会を生み出しています。中国とインドは都市化の動向と、髪の健康・見た目を重視する美容基準の進化に支えられ、地域内で最大の成長機会を提示しています。

欧州は、確立された医療システムと欧州医薬品庁による規制調和により、着実な成長を維持しております。同地域では臨床的に検証された治療法と持続可能な製品処方に強い嗜好が示され、環境に配慮した包装や原料調達への需要が高まっております。南米および中東・アフリカ地域は、中産階級人口の増加と医療費支出の拡大により新興市場としての機会を秘めておりますが、一部地域では経済的要因や流通インフラの制約により市場発展が制限されております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 高齢化

- 科学技術の発展

- ソーシャルメディアと美容インフルエンサーの影響

- 非侵襲的代替療法の普及が進んでいます

- 高まる美的意識

- 近代的な小売業とeコマースの拡大

- 市場抑制要因

- 偽造品および安全でない製品の蔓延

- 規制上の障壁と承認遅延

- 潜在的な副作用

- 製品効果のばらつき

- 消費者行動分析

- 規制情勢

- 技術的進歩

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- シャンプーおよびコンディショナー

- 美容液

- その他

- 性別

- 男性

- 女性

- カテゴリー別

- 局所的

- 経口

- 流通チャネル別

- スーパーマーケット/ハイパーマーケット

- 健康・美容専門店

- オンライン小売店

- その他流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- The Procter & Gamble Company

- L'Oreal S.A.

- Unilever

- Pierre Fabre Laboratories

- Estee Lauder Inc

- Freedom Laser Therapy

- Cipla Ltd.

- Dr. Reddy's Laboratories

- Sun Pharmaceutical Industries

- Merck & Co., Inc.

- Shiseido Company Limited

- Himalaya Wellness Company

- Natura & Co

- Taisho Pharmaceutical Holdings

- Capillus LLC

- Theradome Inc.

- iRestore

- Aclaris Therapeutics

- Fagron NV

- iGrow/Apira Science