|

|

市場調査レポート

商品コード

1437908

航空宇宙・防衛における人工知能・ロボット:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Artificial Intelligence and Robotics in Aerospace and Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空宇宙・防衛における人工知能・ロボット:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 92 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

航空宇宙・防衛における人工知能・ロボットの市場規模は、2024年に319億米ドルと推定され、2029年までに458億米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.5%のCAGRで成長します。

世界の航空宇宙および防衛製造部門は、COVID-19感染症のパンデミックにより、前例のない混乱に直面しています。また、民間航空業界では、COVID-19症の拡大を抑えるための国内外の旅行制限により、空港運営会社と航空会社の収益が2020年と2021年に減少しました。その結果、エンドユーザーの収益が減少するにつれて、航空宇宙および防衛分野の人工知能とロボット工学の市場はわずかに減少しました。

それにもかかわらず、一部の大手航空会社や空港当局は、COVID-19感染症のパンデミック下での安全性と効率性を高めるため、空港のさまざまな旅客プロセスに人工知能を導入することに投資しています。

A&D分野におけるAIベースのテクノロジーの応用が増え続けており、AIと機械学習(ML)の開発とエンドユーザー分野への統合に集中している投資の増加により、予測期間中に市場に注目が集まると予想されます。しかし、初期テクノロジーの開発および導入の初期段階でよく見られる、関連する技術的および運用上の課題が、AIベースのテクノロジーの導入を妨げています。

航空宇宙・防衛における人工知能・ロボットの動向

予測期間中は軍事用途セグメントが優勢になると予想される

より適切な意思決定のためのビッグデータ分析、無人地上車両(UGV)と無人航空機(UAV)の統合による物流の自動化、生物インスピレーションを受けたロボット(群AIとディープニューラル)など、軍事分野におけるAIの応用例が多数あります。ネットワーク、ニューラルネットワークを介した水中鉱山の位置、およびオブジェクトの位置は、予測期間中の市場の成長を促進すると予想されます。 AIとロボティクスの開発と統合への投資の増加、およびAIベースの機器の研究開発と取得に向けた国防予算の配分の強化も、市場の見通しを高めると予想されます。たとえば、2020年に中国人民解放軍(PLA)が発行した2万1000件の機器契約のうち、約350件の記録がAIシステムと機器に関連付けられていました。 2021年 10月、NATOは、AI業界内で競合に先んじるための最初の戦略として、10億米ドル相当のイノベーション基金を立ち上げる計画を発表しました。 2021年6月、国防総省は2022年国防総省予算でAIおよび機械学習テクノロジーに8億7,400万米ドルを支出する計画を発表し、これはAIベースのテクノロジーへの予算配分が前年比で50%増加することを意味しています。このような投資は、予測期間中に市場の軍事分野の成長を促進すると予想されます。

アジア太平洋は予測期間中に最高の成長を遂げると予想される

アジア太平洋では、OEMと通信事業者が同様にサプライチェーン全体にわたるAI統合プロセスへの投資を強化することが想定されており、人工知能と機械学習テクノロジーの導入が最も大きく成長すると予想されています。日本、韓国、中国などの国々が、AIの開発と統合の分野で主導的なイノベーターとして台頭しています。この地域の多くの研究機関は、航空業界におけるAIの高度な応用に関する調査活動に取り組んでいます。アジア太平洋の多くの航空機および関連部品の製造部門は、AIテクノロジーの導入による着実な利益を目の当たりにしています。たとえば、シンガポールのプラット・アンド・ホイットニー施設での適応加工と最先端の自動検査システムの使用により、近年、施設の生産量は着実に増加しています。中国は、人工知能技術を利用して人民解放軍(PLA)を強化することを構想しており、戦略家らはこれをクラウドコンピューティング、ビッグデータ分析、量子情報、無人システム、軍事用途向け。人民解放軍は、2035年までに完全な近代化を達成し、2050年までに米国軍と同等の近代化を達成することを目指しています。中国の新世代人工知能開発計画では、指揮と意思決定のサポート、軍事控除の提供など、防衛用途向けのAI開発戦略の概要が示されています。、防衛機器、その他の用途。このような発展は、予測期間中に焦点を当てている市場に大きなプラスの影響を与えると予想されます。

航空宇宙・防衛における人工知能・ロボットの概要

航空宇宙・防衛における人工知能・ロボットの市場は非常に細分化されており、航空宇宙および防衛のエンドユーザー向けにAIハードウェアおよびソフトウェアを組み込んだ製品やソリューションを提供するロボットメーカーやOEMなど、複数の企業が存在します。さらに、この市場には、OEM向けのAIおよびロボット技術プロバイダーが含まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- USDの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模と予測、世界、2018~2027年

- 提供物別の市場シェア、2021年

- アプリケーション別の市場シェア、2021年

- 地域別市場シェア、2021年

- 市場の構造と主要参加者

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 提供

- ハードウェア

- ソフトウェア

- サービス

- 用途

- 軍隊

- 民間航空

- 空間

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Airbus SE

- IBM Corporation

- The Boeing Comapny

- Nvidia Corporation

- GE Aviation

- Thales Group

- Lockheed Martin Corporation

- Intel Corporation

- Iris Automation Inc.

- SITA

- Raytheon Technologies Corporation

- General Dynamics Corporation

- Northrop Grumman Corporation

- Microsoft

- Spark Cognition

- Honeywell International Inc.

- Indra Sistemas SA

- T-Systems International GmbH

第7章 市場機会と将来の動向

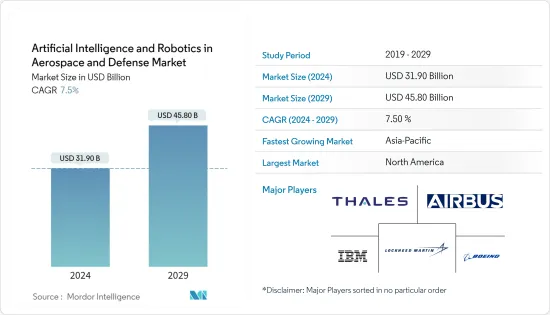

The Artificial Intelligence and Robotics in Aerospace and Defense Market size is estimated at USD 31.90 billion in 2024, and is expected to reach USD 45.80 billion by 2029, growing at a CAGR of 7.5% during the forecast period (2024-2029).

The global aerospace and defense manufacturing sector is undergoing an unprecedented disruption due to the COVID-19 pandemic. Also, in the commercial airline industry, the revenue of airport operators and airlines decreased in 2020 and 2021 due to the restrictions on domestic and international travel to attenuate the spread of COVID-19. Consequently, the market for artificial intelligence and robotics in aerospace and defense witnessed a slight decline as the revenues of end users declined.

Nevertheless, some of the major airlines and airport authorities have invested in the implementation of artificial intelligence in various passenger processes at airports to enhance their safety and efficiency during the COVID-19 pandemic.

The ever-increasing application of AI-based technologies in the A&D sector and increasing investments being funneled to develop and integrate AI and machine learning (ML) into the end-user sectors are anticipated to drive the market in focus during the forecast period. However, the associated technical and operational challenges that are often observed during the initial stages of development and adoption of a nascent technology are hindering the adoption of AI-based technologies.

AI and Robotics in Aerospace and Defense Market Trends

The Military Application Segment is Expected to Dominate During the Forecast Period

The plethora of applications of AI within the military segment, such as big data analytics for better decision-making, automated logistics through the integration of unmanned ground vehicles (UGV) and unmanned aerial vehicles (UAV), bioinspired robots (swarm AI and deep neural networks), underwater mines location through neural networks, and object location are expected to promote the market growth during the forecast period. The rise in investments in the development and integration of AI and robotics and the enhanced defense budget allocation toward the R&D and acquisition of AI-based equipment are also anticipated to augment market prospects. For instance, out of 21,000 equipment contracts published by the People's Liberation Army (PLA) China in 2020, approximately 350 records were aligned to AI systems and equipment. In October 2021, NATO announced plans to launch an innovation fund worth USD 1 billion as its initial strategy to stay ahead of the competition within the AI vertical. In June 2021, Pentagon announced plans to spend USD 874 million on AI and machine learning technologies under the DOD budget 2022, signifying a Y-o-Y increase of 50% in budget allocation toward AI-based technologies. Such investments are expected to drive the growth of the military segment of the market during the forecast period.

Asia-Pacific is Expected to Witness the Highest Growth During the Forecast Period

Asia-Pacific is slated to witness the highest growth in the adoption of artificial intelligence and machine learning technologies as OEMs and operators alike are envisioned to enhance their investment in AI integration processes across the supply chain. Countries such as Japan, South Korea, and China have emerged as the leading innovators in the field of AI development and integration. Many institutes in the region are involved in research activities pertaining to advanced applications of AI in the aviation industry. Numerous aircraft and associated component manufacturing units in Asia-Pacific have witnessed steady benefits from the incorporation of AI technologies. For instance, the use of adaptive machining and cutting-edge automated inspection systems at the Pratt & Whitney facility in Singapore has caused steady growth in output volumes at the facility in recent years. China envisions to use AI technologies to strengthen the People's Liberation Army (PLA) by enabling it to engage in intelligent warfare, defined by strategists as the operationalization of AI and its enabling technologies, such as cloud computing, big data analytics, quantum information, and unmanned systems, for military applications. The PLA aims to achieve full modernization by 2035 and at par with the US military by 2050. China's New Generation Artificial Intelligence Development Plan outlines its strategy for the development of AI for defense applications such as providing support for command and decision-making, military deductions, defense equipment, and other applications. Such developments are anticipated to have a profound positive effect on the market in focus during the forecast period.

AI and Robotics in Aerospace and Defense Industry Overview

The market for artificial intelligence and robotics in aerospace and defense is highly fragmented, with the presence of several players, including robot manufacturers and OEMs that offer products and solutions incorporating AI hardware and software for aerospace and defense end users. In addition, the market comprises AI and robotic technology providers for OEMs. Some of the leading players in the artificial intelligence and robotics in aerospace and defense market are The Boeing Company, Lockheed Martin Corporation, Airbus SE, IBM Corporation, and Thales Group. To expand their presence in the market, companies are partnering with aerospace and defense OEMs to develop new and advanced AI-based solutions that will enhance the safety and efficiency of operations by streamlining mission effectiveness. On this note, in October 2021, IBM and Raytheon Technologies signed a partnership agreement to develop advanced AI, cryptographic, and quantum solutions for the aerospace, defense, and intelligence industries. The systems integrated with AI and quantum technologies are expected to have better-secured communication networks and improved decision-making processes for aerospace and government customers. Also, defense OEMs are collaborating on developing autonomous features and sophisticated acoustic and imaging sensors (like cameras, radar, sonar, GPS, etc.) to decrease the pilot involvement operation of systems in complex, variable, and communication-limited environments. Such partnerships and developments are anticipated to support the growth of the players in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by Offering, 2021

- 3.3 Market Share by Application, 2021

- 3.4 Market Share by Geography, 2021

- 3.5 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD billion)

- 5.1 Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Service

- 5.2 Application

- 5.2.1 Military

- 5.2.2 Commercial Aviation

- 5.2.3 Space

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Airbus SE

- 6.2.2 IBM Corporation

- 6.2.3 The Boeing Comapny

- 6.2.4 Nvidia Corporation

- 6.2.5 GE Aviation

- 6.2.6 Thales Group

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Intel Corporation

- 6.2.9 Iris Automation Inc.

- 6.2.10 SITA

- 6.2.11 Raytheon Technologies Corporation

- 6.2.12 General Dynamics Corporation

- 6.2.13 Northrop Grumman Corporation

- 6.2.14 Microsoft

- 6.2.15 Spark Cognition

- 6.2.16 Honeywell International Inc.

- 6.2.17 Indra Sistemas SA

- 6.2.18 T-Systems International GmbH