|

|

市場調査レポート

商品コード

1638834

航空宇宙・防衛分野におけるAIとロボティクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測AI and Robotics in Aerospace and Defense Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 航空宇宙・防衛分野におけるAIとロボティクス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年11月12日

発行: Global Market Insights Inc.

ページ情報: 英文 230 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

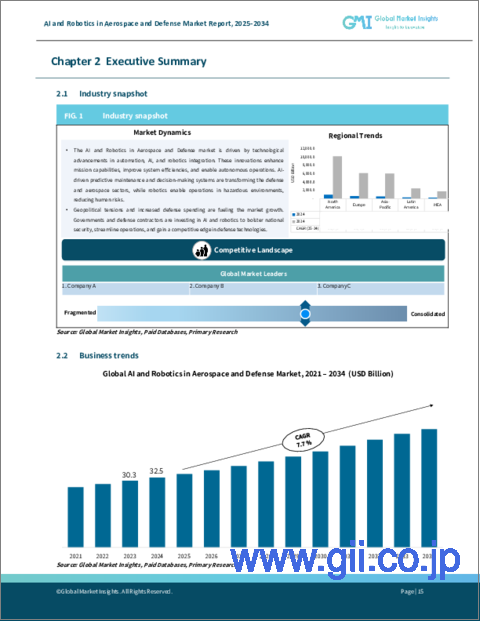

航空宇宙・防衛分野におけるAIとロボティクスの世界市場は2024年に325億米ドルに達し、2032年までのCAGRは7.7%と予測されています。

AIの進歩は航空宇宙システムを変革し、無人航空機(UAV)や自律型航空機の自律性を強化しています。機械学習、コンピューター・ビジョン、センサー・フュージョンを含むAIの中核技術により、航空宇宙アプリケーションは、人間が関与することなく、より高い精度、信頼性、高度な意思決定を達成することができます。

大きな可能性があるにもかかわらず、市場は、主に研究開発、技術統合の高コストといった障害に直面しています。それにもかかわらず、自律型ドローン、AI駆動型軍事ロボット、運用効率の向上を約束する高度な監視システムに対する需要は拡大しています。安全基準、データ保護、防衛コンプライアンスをめぐる規制要件は成長を制限する可能性があるが、進化する防衛政策と国境を越えた協力関係がこうした制限の緩和に役立っています。

市場はコンポーネント別にハードウェア、ソフトウェア、サービスに区分され、2024年にはハードウェア分野が46.7%と最大の市場シェアを占める。ハードウェアの革新、特にセンサー、プロセッサー、アクチュエーターは、自律走行能力の開発に不可欠です。データ収集の強化、リアルタイム分析、ドローン、ロボット、その他の無人車両の操縦性の向上は、高性能AIチップとエッジコンピューティング技術によって推進されており、重要なミッションのためのデータ処理の高速化と低遅延を可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 325億米ドル |

| 予測金額 | 679億米ドル |

| CAGR | 7.7% |

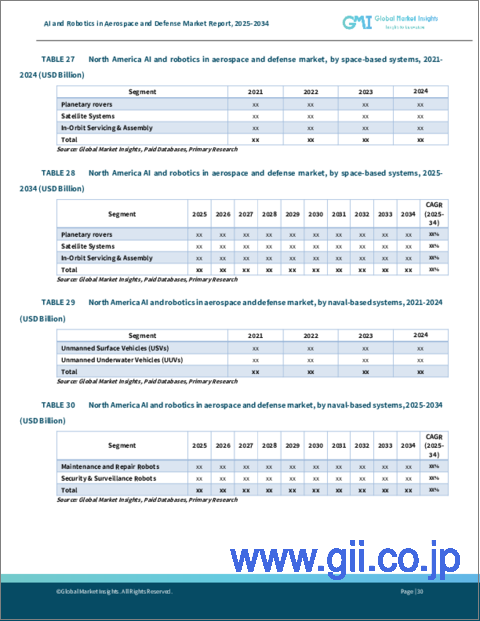

航空宇宙・防衛分野におけるAIとロボティクスの導入は、航空、地上、宇宙、海軍の各システムに分類されます。宇宙ベースのセグメントは、予測期間のCAGRが10.4%と予測され、成長が見込まれています。これらのシステムは、監視、通信、ナビゲーションにますます不可欠になっており、自律的な意思決定、AI主導のデータ分析、異常検知は、厳しい環境での作戦に不可欠です。人工衛星や宇宙探査機におけるロボティクスはミッション効率をさらに高め、メンテナンス、資源収集、惑星探査などのタスクをサポートします。

北米は2024年に34.5%のシェアを獲得して航空宇宙・防衛分野におけるAIとロボティクス市場をリードし、今後もその優位性を維持すると予想されています。同地域の成長は、自律防衛技術、AIで強化された監視、軍事用ロボットへの旺盛な投資によるところが大きいです。米国政府、特に国防総省は、防衛インフラの近代化のために技術革新を優先しています。防衛請負業者との戦略的パートナーシップは、AIとロボット工学の進歩を加速させ、航空宇宙・防衛技術における北米の主導的地位を強化しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 促進要因

- 航空宇宙システムにおける自律性を高めるAIの進歩

- 軍事ロボット工学と防衛への投資の急増

- AIを活用した予知保全による操業停止時間の短縮

- 監視・偵察におけるドローン需要の増加

- 宇宙探査ミッションにおけるロボット工学の利用拡大

- 業界の潜在的リスク&課題

- 航空宇宙分野での高い研究開発・導入コスト

- 市場成長を妨げる規制上のハードルと安全性への懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- ソフトウェア

- サービス

第6章 市場推計・予測:展開別、2021-2034年

- 主要動向

- 空中システム

- 地上システム

- 宇宙ベースシステム

- 艦艇搭載型システム

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府/軍事

- 商用

- 宇宙機関、研究機関

第8章 市場推計・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Airbus SE

- Bae Systems

- GE Aviation

- General Dynamics Corporation

- Honeywell International Inc.

- IBM Corporation

- Intel Corporation

- Iris Automation Inc.

- L3 Harris Technologies

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Microsoft

- Northrop Grumman Corporation

- Nvidia Corporation

- Raytheon Technologies Corporation

- Rheinmatall AG

- SAAB AB

- Safran SA

- Sheild AI

- SITA

- Thales Group

- The Boeing Company

The Global AI And Robotics In Aerospace And Defense Market reached USD 32.5 billion in 2024, with projections for a 7.7% CAGR through 2032. AI advancements are transforming aerospace systems, enhancing autonomy in unmanned aerial vehicles (UAVs) and autonomous aircraft. Core AI technologies, including machine learning, computer vision, and sensor fusion, enable aerospace applications to achieve higher precision, reliability, and sophisticated decision-making without human involvement.

Despite significant potential, the market faces obstacles, primarily the high costs of research, development, and technology integration. Nonetheless, demand is growing for autonomous drones, AI-driven military robots, and advanced surveillance systems that promise increased operational efficiency. Regulatory requirements surrounding safety standards, data protection, and defense compliance can limit growth, but evolving defense policies and cross-border collaborations are helping to alleviate these restrictions.

The market is segmented by component into hardware, software, and services, with the hardware sector holding the largest market share at 46.7% in 2024. Hardware innovations-particularly in sensors, processors, and actuators-are crucial for developing autonomous capabilities. Enhanced data collection, real-time analytics, and improved maneuverability in drones, robots, and other unmanned vehicles are being driven by high-performance AI chips and edge computing technology, allowing faster data processing and low latency for critical missions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.5 Billion |

| Forecast Value | $67.9 Billion |

| CAGR | 7.7% |

Deployment in AI and robotics in aerospace and defense market is categorized across airborne, ground-based, space-based, and naval systems. The space-based segment is expected to grow, with a projected 10.4% CAGR over the forecast period. These systems are increasingly vital for surveillance, communication, and navigation, where autonomous decision-making, AI-driven data analysis, and anomaly detection are essential for operations in challenging environments. Robotics in satellites and space exploration vehicles further enhance mission efficiency, supporting tasks such as maintenance, resource collection, and planetary exploration.

North America led the AI and robotics in aerospace and defense market with a 34.5% share in 2024 and is expected to retain its dominance. Growth in the region is largely attributed to robust investments in autonomous defense technologies, AI-enhanced surveillance, and military robotics. The U.S. government, particularly the Department of Defense, is prioritizing technological innovation to modernize its defense infrastructure. Strategic partnerships with defense contractors accelerate advancements in AI and robotics, reinforcing North America's leading position in aerospace and defense technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in AI enhancing autonomy in aerospace systems

- 3.6.1.2 Surge in investment for military robotics and defense

- 3.6.1.3 AI-driven predictive maintenance reducing downtime in operations

- 3.6.1.4 Increasing demand for drones in surveillance and reconnaissance

- 3.6.1.5 Expanding use of robotics in space exploration missions

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High research, development, and implementation costs in aerospace

- 3.6.2.2 Regulatory hurdles and safety concerns hindering market growth

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Airborne systems

- 6.3 Ground-based systems

- 6.4 Space-based systems

- 6.5 Naval-based systems

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Government/Military

- 7.3 Commercial

- 7.4 Space agencies and research institutes

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Airbus SE

- 9.2 Bae Systems

- 9.3 GE Aviation

- 9.4 General Dynamics Corporation

- 9.5 Honeywell International Inc.

- 9.6 IBM Corporation

- 9.7 Intel Corporation

- 9.8 Iris Automation Inc.

- 9.9 L3 Harris Technologies

- 9.10 Leonardo S.p.A.

- 9.11 Lockheed Martin Corporation

- 9.12 Microsoft

- 9.13 Northrop Grumman Corporation

- 9.14 Nvidia Corporation

- 9.15 Raytheon Technologies Corporation

- 9.16 Rheinmatall AG

- 9.17 SAAB AB

- 9.18 Safran SA

- 9.19 Sheild AI

- 9.20 SITA

- 9.21 Thales Group

- 9.22 The Boeing Company