|

市場調査レポート

商品コード

1437611

ターボプロップエンジン:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Turboprop Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ターボプロップエンジン:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

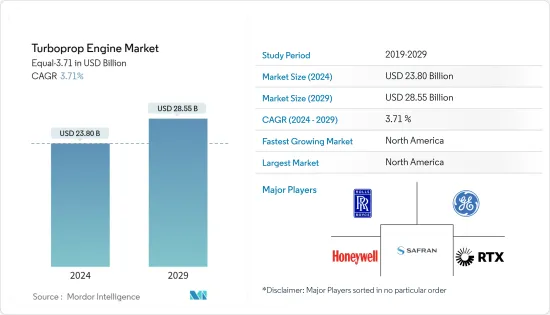

ターボプロップエンジンの市場規模は、2024年に238億米ドルと推定され、2029年までに285億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.71%のCAGRで成長します。

新しい地方路線のイントロダクション伴い、民間航空におけるターボプロップエンジン搭載機への関心が高まっています。ターボプロップエンジンは短距離および低空飛行において効率が高く、民間航空分野の成長に貢献しています。軍用および一般航空分野における需要の増加は、主にターボプロップエンジンを搭載した新しい航空機モデルのイントロダクションよるものです。

ターボプロップ航空機の需要が高まっているのは、新たに開発された短いルートのイントロダクションと低高度での飛行能力、そしてコスト効率のおかげです。ターボプロップエンジン市場では、民間航空分野での人気の高まりにより、ハイブリッドタイプが優位性を保っています。さらに、古い航空機にこれらのハイブリッドエンジンが改装されるため、ターボプロップエンジンの導入が広範囲に行われています。さらに、新しい航空機にはすでにこの最新のターボプロップエンジンが搭載されています。

ターボプロップエンジンは、低空飛行や短距離移動において効率が高く、離陸と着陸に最小限の滑走路スペースしか必要とせず、燃料効率も向上することが証明されています。これらの要因は、個人にとって空の旅をよりアクセスしやすく便利にすることに貢献し、それによってターボプロップエンジンに対する市場の需要が促進されます。

ターボプロップエンジン市場動向

一般航空部門は予測期間中に大幅な成長が見込まれる

最新のアビオニクスと性能面での技術的進歩を備えた新しい航空機モデルに対する需要の増加に伴い、いくつかのターボプロップ航空機メーカーが新しい航空機を開発しています。世界の富裕層と超富裕層の人口の増加は、個人旅行の需要増加の触媒として機能しており、その後、世界中でターボプロップ航空機の調達が促進されています。たとえば、2017年から2022年にかけて、世界の富裕層人口は83%増加しました。 2022年 7月、プラット&ホイットニーカナダはPT6 Eシリーズエンジンファミリの新しいエンジンモデルを発表しました。 PT6E-66XTエンジンは、ダーハー社の最新の単発ターボプロップ飛行機TBM 960専用に設計されています。

2022年1月、カナダのプラット・アンド・ホイットニーは、ダイヤモンド・エアクラフトが新型DART-750航空機にPT6A-25Cエンジンを選択したと発表しました。 DART-750航空機は、オールカーボンファイバー製のタンデムターボプロップ練習機です。したがって、特に一般航空部門における新型ターボプロップ航空機の需要の増加は、ターボプロップエンジンの技術革新を促進すると予想され、予測期間中の市場の成長を促進すると予想されます。

北米が予測期間中に市場を独占すると予測される

北米は、2022年のターボプロップエンジンの最大の市場です。また、この地域は、米国からのターボプロップ航空機に対する大規模な需要により、予測期間中に最高のCAGRで成長すると予想されます。一般航空分野では、2022年のターボプロップ航空機納入台数の約56%を北米だけで占め、そのうち米国が約79%を占めています。この地域は、地域航空機の需要の増加に伴い、民間航空機セグメントにおける新しいターボプロップ航空機の需要も生み出しています。

2039年までに、北米地域のビジネス航空および民間ヘリコプター部門では79,000人のパイロットが必要になると予想されています。経済の前向きな回復傾向と飛行訓練機関の機材拡張計画は、予測期間中に他のカテゴリーの成長を促進すると予想されます。北米では2023年から2028年の間に約1,400機のターボプロップ機が納入されると予想されています。

2023年 11月、RTXのプラット&ホイットニーは、米国国防兵站庁からB-52およびE-3に動力を供給するTF33エンジンについて、最大8億7,000万米ドル相当の契約を受け取りました。この種の開発は、2023年の間にターボプロップエンジン市場の需要を促進するでしょう。北米の予測期間。

ターボプロップエンジン業界の概要

ターボプロップエンジン市場は統合されており、数社のターボプロップエンジンOEM企業が市場シェアの大部分を占めています。市場の著名なプレーヤーには、RTX Corporation、Rolls-Royce plc、Safran、General Electric Company、Honeywell International, Inc.などがあります。エンジンメーカーとOEMは、製品とそのサービスを提供するために長期契約を結んでいます。新規参入者が市場に参入し、維持することは困難です。積層造形などの先進技術の研究開発への多額の投資や、エンジンの生産率を高めるための自動化やAIの導入は、プレーヤーの生産能力の向上に役立ち、それによって予測期間中の成長を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 応用

- 民間航空機

- 軍用機

- 一般航空用航空機

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋地域

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- 残りの中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- RTX Corporation

- Rolls-Royce plc

- Safran

- General Electric Company

- Honeywell International, Inc.

- MTU Aero Engines AG

- PBS AEROSPACE Inc.

- Motor Sich JSC

- TUSAS Engine Industries, Inc.

第7章 市場機会と将来の動向

The Turboprop Engine Market size is estimated at USD 23.80 billion in 2024, and is expected to reach USD 28.55 billion by 2029, growing at a CAGR of 3.71% during the forecast period (2024-2029).

The preference for turboprop engine-powered aircraft in commercial aviation is growing with the introduction of new regional routes. The turboprop engines are highly efficient in short-distance and low-altitude flying, which is helping their growth in the commercial aviation sector. In the military and general aviation segments, the growth in demand is mainly due to the introduction of new aircraft models that are powered by turboprop engines.

The increrasing demand of turboprop aircraft are due to the introduction of newly developed shorter routes and the ability to fly at low altitudes, coupled with cost efficiency. Within the turboprop engine market, the hybrid variety holds dominance owing to its increasing popularity in the civil aviation sector. Furthermore, the deployment of turboprop engines is extensive as older aircraft are retrofitted with these hybrid engines. In addition, newer aircraft are already equipped with this modern turboprop engine.

The turboprop engines prove to be highly efficient in low altitude flying, short distance travel, requiring minimal airstrip space for take-off and landing, and enhancing fuel efficiency. These factors contribute to making air travel more accessible and convenient for individuals, thereby driving the market demand for turboprop engines.

Turboprop Engine Market Trends

General Aviation Segment is Expected Witness Significant Growth During the Forecast Period

With the growth in demand for newer aircraft models featuring the latest avionics and technological advancements in terms of performance, several turboprop aircraft manufacturers are developing new aircraft. Growth in the HNWI and UHNWI populations globally is acting as a catalyst for the increased demand for private travel, subsequently driving the procurement of turboprop aircraft globally. For instance, from 2017 to 2022, the HNWI population increased by 83% globally. In July 2022, Pratt & Whitney Canada announced a new engine model for its PT6 E-Series engine family. The PT6E-66XT engine is purpose-built for Daher's latest single-engine turboprop airplane, the TBM 960.

In January 2022, Pratt & Whitney Canada that Diamond Aircraft had selected the PT6A-25C engine for its new DART-750 aircraft. DART-750 aircraft is an all-carbon fiber tandem turboprop trainer aircraft. Thus, the growth in demand for newer turboprop aircraft, especially in the general aviation segment is expected to drive the innovations in turboprop engines which is expected to help the market growth during the forecast period.

North America Projected to Dominate the Market During the Forecast Period

North America is the largest market for Turboprop Engines in 2022. The region is also expected to grow with the highest CAGR during the forecast period, due to large-scale demand for turboprop aircraft from the United States. In the General Aviation segment, North America alone accounted for about 56% of the turboprop aircraft deliveries in 2022 in which the U.S. has having contribution of around 79%. The region is also generating demand for new turboprop aircraft in the commercial aircraft segment, with the growth in the demand for regional aircraft.

It is expected that by 2039 there will be a requirement of 79,000 pilots in the business aviation and civil helicopter sector in the North American region. The positive economic recovery trend along with the fleet expansion plans of flight training institutes is expected to aid the growth of other categories during the forecast period. It is expected around 1,400 turboprops will be delivered during 2023-2028 in North America.

In November 2023, RTX's Pratt & Whitney received a contract valued up to USD 870 million for TF33 engines powering B-52s, and E-3s by the Defense Logistics Agency of the U.S. Such kind of development will drive the demand for turboprop engine market during the forecast period in North America.

Turboprop Engine Industry Overview

The turboprop engine market is consolidated, with the presence of a few turboprop engine OEMs which occupy a majority of the market share. Some of the prominent players in the market are RTX Corporation, Rolls-Royce plc, Safran, General Electric Company, and Honeywell International, Inc. The engine manufacturers and OEMs enjoy long-term contracts, for providing products and their services, thereby, making it difficult for new players to enter and sustain in the market. Significant investment into R&D of advanced technologies like additive manufacturing and incorporation of automation and AI to increase the production rate of the engines are expected to help the players to ramp up their production capacity, thereby, helping their growth during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porters Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial Aircraft

- 5.1.2 Military Aircraft

- 5.1.3 General Aviation Aircraft

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Israel

- 5.2.5.4 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 RTX Corporation

- 6.2.2 Rolls-Royce plc

- 6.2.3 Safran

- 6.2.4 General Electric Company

- 6.2.5 Honeywell International, Inc.

- 6.2.6 MTU Aero Engines AG

- 6.2.7 PBS AEROSPACE Inc.

- 6.2.8 Motor Sich JSC

- 6.2.9 TUSAS Engine Industries, Inc.