|

市場調査レポート

商品コード

1692521

世界の急性呼吸窮迫症候群(ARDS)治療- 市場シェア分析、産業動向・統計、成長動向予測(2025年~2030年)Global Acute Respiratory Distress Syndrome (ARDS) Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の急性呼吸窮迫症候群(ARDS)治療- 市場シェア分析、産業動向・統計、成長動向予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

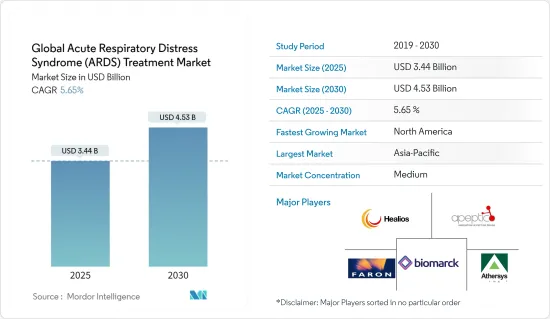

世界の急性呼吸窮迫症候群治療市場規模は、2025年に34億4,000万米ドルと推定され、2030年には45億3,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは5.65%です。

重症感染症のCOVID-19患者の臨床データによると、肺水腫のX線学的証拠から、COVID-19患者では急性肺障害(ALI)の症状が低酸素血症や場合によってはARDSに進行する可能性があることが示されています。2021年12月にPneumonia誌に掲載された「COVID-19における急性呼吸窮迫症候群:可能性のある機序と治療管理」と題する研究によると、入院患者の約3分の1または(33%)がARDSを経験します。さらに、集中治療室に入院したCOVID-19患者のほぼ3/4(または75%)にARDSがみられます。COVID-19のARDS患者は予後が悪く、死亡率が高いです。したがって、急性呼吸窮迫市場はCOVID-19によって大きな影響を受けています。

急性呼吸窮迫症候群(ARDS)市場は、急性肺損傷の有病率と発生率の上昇、ARDSの幅広い危険因子、ARDSを発症するCOVID-19患者の増加などの要因によって牽引されています。また、急性呼吸窮迫症候群(ARDS)の世界市場は、ARDSを引き起こす生活習慣の選択、大気汚染、事故に関連した疾患の流行などの要因の結果、成長すると予想されています。急性呼吸窮迫症候群」と題された調査によると2022年6月に発表されたMark D Siegelによる「Epidemiology, pathophysiology, pathology, and etiology in adults(成人における疫学、病態生理学、病理学、病因学)」によると、米国では年間約190,000件のARDS症例が報告されています。罹患率は患者の年齢とともに上昇し、15~19歳では10万人年当たり16人であったのが、75~84歳では10万人年当たり306人となりました。さらに、高齢者の増加が市場の成長を支えています。例えば、国連経済社会局の報告書「World Population Ageing 2020 Highlights」によると、2020年の世界の65歳以上の人口は7億2,700万人です。2050年には2倍以上の15億人近くに達すると予想されています。高齢者は呼吸器疾患やその他の病気にかかるリスクが高いため、治療の必要性が生じ、市場の成長を促進すると予想されます。

さらに、医療支出の増加と市場参入企業の戦略的イニシアチブは、世界の急性呼吸窮迫症候群(ARDS)市場に成長機会をもたらします。例えば、2020年6月、NeuroRxはRelief Therapeuticsとの提携により、米国食品医薬品局からNeuroRxに対し、COVID-19に伴う急性肺障害/急性呼吸窮迫症候群の治療としてRLF-100(Aviptadil)のファストトラック指定を授与したと発表しました。さらに2020年11月、Novartisはメソブラスト社と、急性呼吸窮迫症候群の治療remestemcel-Lの開発、販売、製造に関する全世界での独占的ライセンスと提携契約を締結したと発表しました。

このように、前述のすべての要因が予測期間中の市場成長を押し上げると予想されるが、治療や機器に関連する高コストや規制の複雑さが市場成長を抑制要因になる可能性があります。

急性呼吸窮迫症候群治療市場動向

エンドユーザー別では病院/クリニックが予測期間中に健全な成長を遂げる見込み

病院/クリニックは、外科的処置や改善された治療のための先進的技術設備を備えており、ARDSによる入院患者数の増加、患者プールの増加、市場参入企業による新製品の発売により、病院セグメントは急速な成長を目の当たりにしています。

また、民間企業による病院数の増加も市場の成長を促進すると予想されます。2022年1月に発表された米国病院協会統計2022によると、2021年の米国における非政府の非営利コミュニティ病院の数は2,946であり、この数は2022年には2,960に増加しました。その結果、ARDS患者の治療に利用できるベッド数が増加し、病院数の増加が予測期間中の同セグメントの成長を支えています。

重症治療室への入院や入室数の増加は、ARDS治療の必要性を生み出し、市場の成長を促進します。急性呼吸窮迫症候群の再入院」と題された調査によると、ARDSは、重症呼吸窮迫症候群(Acute Respiratory Distress Syndrome Readmissions)の1つです。2022年1月にPLOS One Journalで発表された「A nationwide cross-sectional analysis of epidemiology and costs of care」によると、急性呼吸窮迫症候群患者の18.4%が再入院を経験しています。さらに、オーストラリア保健福祉ラボが2022年5月に発表したデータによると、2020~2021年に発生した入院患者数は約1,180万人で、2019~20年に比べて6.3%増加しています。また、1,180万人の入院のうち、集中治療室(ICU)への入院が7.0%、呼吸器疾患が3.8%、入院患者が院内で死亡したことを示す分離モードが10.3%であったことも報告されています。このような救命救急入院の増加は、ARDS治療の必要性を生み出し、市場セグメントの成長を促進すると予想されます。

したがって、上記の要因により、このセグメントは予測期間中に健全な成長率を示すと予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は、大手市場参入企業の存在、製品承認の増加、医療制度の発達、急性呼吸窮迫症候群の高い有病率により、世界のARDS治療市場を独占しています。

2022年2月にNational Library of Medicineに掲載された「Acute Respiratory Distress Syndrome(急性呼吸窮迫症候群)」と題する研究によると、米国におけるARDSの発症率は、1年間で人口10万人当たり64.2~78.9人と報告されています。ARDS症例の初期評価では、25%が軽症、75%が中等症または重症に分類されます。しかし、軽症例の3分の1が中等症または重症に発展します。したがって、米国における急性呼吸窮迫症候群の有病率の増加は、予測期間における市場の成長を支えています。

主要市場参入企業の様々な有機的・無機的戦略の採用は、市場成長を加速させると予想されます。例えば、2020年12月、食品医薬品局(FDA)は、コロナウイルス疾患(COVID-19)によってもたらされる急性呼吸窮迫症候群(ARDS)の治療としてRemestemcel-Lをファストトラック指定しました。さらに2020年9月、AthersysはMultiStem細胞療法が急性呼吸窮迫症候群(ARDS)プログラムに対して米国食品医薬品局(FDA)から再生医療先進治療(RMAT)の指定を受けたと発表しました。

このように、上記のすべての要因のおかげで、市場は高い成長を示すことが期待されています。

急性呼吸窮迫症候群治療産業概要

世界の急性呼吸窮迫症候群市場は競争が激しく、少数の大手企業で構成されています。Faron Pharmaceuticals、BioMarck Pharmaceuticals、GE Healthcare、Hamilton Companyなどの企業が、急性呼吸窮迫症候群市場でかなりの市場シェアを占めています。市場参入企業は、市場で競合を維持するために、新製品の発売、パートナーシップ、提携など様々な戦略を採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 急性呼吸困難症候群の有病率の増加。

- タバコの喫煙率の高さ、都市化、汚染レベルの増加

- 高齢者の増加

- 市場抑制要因

- 不利な償還シナリオ

- 治療に伴う合併症と機器・治療費の高騰

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 治療別

- 薬剤クラス別

- 血管収縮薬

- 気管支拡大薬

- ストロイドと抗生物質

- 鎮静・麻痺薬

- 界面活性剤

- その他

- デバイス

- 薬剤クラス別

- エンドユーザー別

- 病院/クリニック

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Faron Pharmaceuticals

- BioMarck Pharmaceuticals

- GE Healthcare

- Hamilton Company

- Athersys

- United Therapeutics

- Apeptico Forschung

- Fisher & Paykel Healthcare Limited

- NRx Pharmaceuticals, Inc.

- HEALIOS K.K

- Dragerwerk AG & Co. KGaA

- ALung Technologies, Inc(LivaNova PLC)

第7章 市場機会と今後の動向

The Global Acute Respiratory Distress Syndrome Treatment Market size is estimated at USD 3.44 billion in 2025, and is expected to reach USD 4.53 billion by 2030, at a CAGR of 5.65% during the forecast period (2025-2030).

According to the clinical data of COVID-19 patients with severe infection, radiologic evidence of lung edema shows that symptoms of Acute Lung Injury (ALI) can progress to hypoxemia and possibly ARDS in COVID-19 patients. According to the study titled "Acute respiratory distress syndrome in COVID-19: possible mechanisms and therapeutic management" published in the Pneumonia in December 2021, about one-third or (33%) of hospitalized patients experience ARDS. Additionally, ARDS is present in almost 3/4 (or 75%) of COVID-19 patients admitted to the intensive care unit. ARDS patients with COVID-19 have a poor prognosis and a high mortality rate. Thus, the acute respiratory distress market has been significantly impacted by COVID-19.

The market for acute respiratory distress syndrome (ARDS) is being driven by factors such as the rising prevalence and incidence of acute lung injury, a wide range of ARDS risk factors, and an increase in the number of patients with COVID-19 who have ARDS. The global market for acute respiratory distress syndrome (ARDS) is also expected to grow as a result of factors such as the prevalence of diseases linked to lifestyle choices, air pollution, and accidents that cause ARDS. According to the study titled "Acute respiratory distress syndrome: Epidemiology, pathophysiology, pathology, and etiology in adults" by Mark D Siegel published in June 2022, around 190,000 ARDS cases are reported annually in the United States. The incidence rose with patient age, rising from 16 per 100,000 person-years for those aged 15 to 19 to 306 per 100,000 person-years for those aged 75 to 84. Moreover, the growing geriatric population supports market growth. For instance, as per United Nations Department of Economic and Social Affairs report titled 'World Population Ageing 2020 Highlights' mentioned that there were 727 million persons aged 65 years or over in the world in 2020. It is expected that the population is more than double and reaches nearly 1.5 billion in 2050. Since the older population is at high risk of getting respiratory and other illnesses, it is expected to generate the need for treatment, thereby driving the market's growth.

Furthermore, increasing healthcare spending and market participants' strategic initiatives present a growth opportunity for the global acute respiratory distress syndrome (ARDS) market. For Instance, In June 2020, NeuroRx, in partnership with Relief Therapeutics, announced that the United States Food and Drug Administration awarded Fast Track designation to NeuroRx for the investigation of RLF-100 (Aviptadil) for the treatment of acute lung injury/acute respiratory distress syndrome associated with COVID-19. Additionally, in November 2020, Novartis declared that it had entered into an exclusive worldwide license and collaboration agreement with Mesoblast to develop, market, and manufacture remestemcel-L to treat acute respiratory distress syndrome.

Thus, all aforementioned factors are expected to boost the market growth over the forecast period, However, high costs associated with the treatment and devices and regulatory complication may restraint the market growth.

Acute Respiratory Distress Syndrome Treatment Market Trends

Hospital/ Clinics by End User Segment is Expected to Witness Healthy Growth Over the Forecast Period

Hospitals/Clinics are well equipped with advanced technological equipment for surgical procedures and improved treatments and the hospital segment is witnessing rapid growth, owing to the growing number of hospital admission with the ARDS, the increasing number of patient pools, and the launch of new products by the market players are expected to continue over the forecast period, and thus, driving growth in the segment.

The increasing number of hospitals by private players is also expected to propel the growth of the market. The American Hospital Association Statistics 2022 published in January 2022 reported that in 2021, there are 2,946 nongovernment not-for-profit community hospitals, and this number increased to 2,960 in 2022 in the United States. As a result, as the number of beds available increases to treat ARDS patients, thus increasing number of hospitals support the segment growth over the forecast period.

The increasing number of hospital admissions and admissions in the critical care unit creates the need the ARDS treatment and thus drives the growth of the market. According to the study titled "Acute respiratory distress syndrome readmissions: A nationwide cross-sectional analysis of epidemiology and costs of care" published in the PLOS One Journal in January 2022,18.4% of patients with acute respiratory distress syndrome underwent rehospitalization. Moreover, as per data released by the Australian Institute of Health and Welfare in May 2022, there are about 11.8 million hospital admission occurred in 2020-21 which is 6.3% more compared to 2019-20. It also reported that out of 11.8 million admissions, 7.0% of hospitalizations involved a stay in the Intensive Care Unit (ICU), 3.8% of hospitalizations involved respiratory disease and 10.3 % of hospitalizations had a separation mode indicating the patient died in the hospital. Such increasing admission in emergency critical care creates the need for ARDS treatment and is thus expected to drive the growth of the market segment.

Thus, owing to the above factors the segment is expected to show a healthy growth rate over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America dominated the global ARDS treatment market due to the presence of major market players, an increase in product approvals, a developed health care system, and a high prevalence of acute respiratory distress syndrome.

According to the study titled "Acute Respiratory Distress Syndrome" published in the National Library of Medicine in February 2022, reported the incidence of ARDS in the United States range from 64.2 to 78.9 cases per 100,000 people in a year. Initial assessments of ARDS cases place 25% of cases in the mild category and 75% in the moderate or severe category. But one-third of mild cases go on to develop into moderate or severe illnesses. Thus, the growing prevalence of acute respiratory distress syndrome in the United States supports the market growth over the forecast period.

The key market players' adoption of various organic and inorganic strategies is anticipated to accelerate market growth. For instance, in December 2020, the Food and Drug Administration (FDA) granted Remestemcel-L Fast Track designation for the treatment of acute respiratory distress syndrome (ARDS) brought on by coronavirus disease (COVID-19). Additionally, in September 2020, Athersys announced that MultiStem cell therapy was granted Regenerative Medicine Advanced Therapy (RMAT) designation from the United States Food and Drug Administration for the acute respiratory distress syndrome (ARDS) program.

Thus, owing to all above-mentioned factors the market is expected to witness high growth.

Acute Respiratory Distress Syndrome Treatment Industry Overview

The global acute respiratory distress syndrome market is highly competitive and consists of a few major players. Companies like Faron Pharmaceuticals, BioMarck Pharmaceuticals, GE Healthcare, Hamilton Company, and others, hold a substantial market share in the acute respiratory distress syndrome market. Market players are adopting various strategies such as new product launches, partnerships, and collaborations to remain competitive in the marketplace.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Acute Respiratory Distress Syndrome.

- 4.2.2 High Prevalence of Tobacco Smoking, Urbanization, And Growing Levels of Pollution

- 4.2.3 Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Unfavorable Reimbursement Scenario

- 4.3.2 Complications Associated with Treatments and High Cost of Devices and Treatments

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Treatment

- 5.1.1 By Drug Class

- 5.1.1.1 Vasoconstrictor

- 5.1.1.2 Bronchodilators

- 5.1.1.3 Streoid and Antibiotics

- 5.1.1.4 Sedative and Paralytic

- 5.1.1.5 Surfactant

- 5.1.1.6 Other

- 5.1.2 Devices

- 5.1.1 By Drug Class

- 5.2 By End User

- 5.2.1 Hospitals/Clinics

- 5.2.2 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Faron Pharmaceuticals

- 6.1.2 BioMarck Pharmaceuticals

- 6.1.3 GE Healthcare

- 6.1.4 Hamilton Company

- 6.1.5 Athersys

- 6.1.6 United Therapeutics

- 6.1.7 Apeptico Forschung

- 6.1.8 Fisher & Paykel Healthcare Limited

- 6.1.9 NRx Pharmaceuticals, Inc.

- 6.1.10 HEALIOS K.K

- 6.1.11 Dragerwerk AG & Co. KGaA,

- 6.1.12 ALung Technologies, Inc ( LivaNova PLC)