|

市場調査レポート

商品コード

1437326

診断向けAI(人工知能):世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Artificial Intelligence in Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 診断向けAI(人工知能):世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

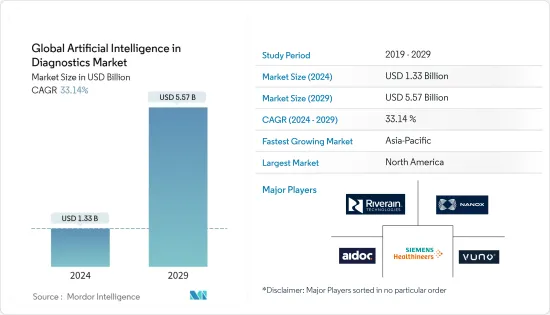

世界の診断向けAI(人工知能)市場規模は、2024年に13億3,000万米ドルと推定され、2029年までに55億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に33.14%のCAGRで成長します。

COVID-19のパンデミックは、医療システム、特に診断に大きな影響を与えています。世界のロックダウン措置により公共の移動が減少し、診断業界に影響を与えました。さらに、COVID-19のパンデミックは世界経済に影響を与えただけでなく、世界中の病院におけるCOVID-19以外の患者に対する一般的な病院医療の機能にも大きな影響を与えました。しかし、世界的に画像診断の需要が高まるにつれ、診断向けAIの導入に対する需要も高まっています。 2021年4月に公開された記事「COVID-19の診断向けAI:課題と展望」によると、診断を含む医療システムのさまざまなレベルでAIが導入されています。特に現在のパンデミック下では、AIアルゴリズムはCOVID-19患者の迅速な診断に不可欠です。

さらに、診断から医薬品開発、疾病伝播予測、人口監視と監視に至るまで、パンデミックの深さと複雑さに対処するためにAIツールが採用されました。 2021年 4月に「Nature Public Health Emergency Collection」誌に掲載された「COVID-19のパンデミックとの闘いにおけるAIの役割」と題された研究では、時間的ステップ法が提案されています。これには、最近の調査調査の紹介、AIがどのように機能するかを調べることが含まれています。社会と医療システムを観察して行動し、さまざまな種類のデータを報告します。したがって、SARS-CoV-2患者の診断向けAIツールの導入は、パンデミック段階を通じて重要な役割を果たし、それによって市場の成長を促進しました。

さらに、医用イメージング分野におけるAIツールの需要の高まり、放射線科医の負担軽減への注目の高まり、AIベースの技術の導入を促進する政府の取り組み、AIベースのスタートアップへの資金調達の増加などの要因が予想されます。市場の成長をすぐに強化します。

イメージングデバイスにAIを組み込むことで診断が改善される可能性があり、予測期間中の市場全体の成長を促進すると予想されます。たとえば、2021年 12月に掲載された米国医師会ジャーナルの「多施設研究による人体結節検出精度に関するAIベースの胸部X線モデル」というタイトルの記事では、AIアルゴリズムが検出の向上に関連していると報告しています。

さらに、世界的にAIスタートアップへの資金提供が増加していることなどの要因により、画像診断モダリティへのAIの組み込みを増やす需要が高まっています。たとえば、2022年 3月に4,000万米ドルの資金調達を行ったヘルステック企業Qure.ai(Qure)は、医用イメージング診断にAIを採用しています。同社はさらに、この資金を利用して、特に米国と欧州での世界のプレゼンスを拡大および向上させ、救命救急および地域診断用の製品開発を加速すると宣言しました。したがって、このような資金調達は市場の成長に貢献すると予想されます。

したがって、前述の要因により、調査対象の市場は分析期間中に成長すると予想されます。しかし、熟練したAI労働力の不足と医療ソフトウェアの曖昧な規制ガイドラインにより、市場の成長が抑制されることが予想されます。

診断向けAI市場の動向

X線セグメントが市場を独占すると予想される

X線セグメントは、予測期間中に大きな市場シェアを獲得すると予想されます。 X線はほとんどの放射線科で行われる最も一般的な画像検査であるため、AIが従来のX線写真(X線画像)のトリアージと解釈を支援する可能性は特に重要です。 X線にAIを組み込むことで、効率、精度、アクセスのしやすさ、ワークフローが向上し、時間が短縮され、品質と患者の安全性が向上します。これらの利点により、X線におけるAIの需要が増加し、予測期間中のこの部門の成長を促進すると予想されます。

さらに、2021年8月に公開された「これらのアルゴリズムはX線を見て、何らかの方法で人種を検出する」と題された記事では、最近市場関係者がX線を解釈し、状態を識別するためのAIソフトウェアを作成するためのイノベーションに多額の費用を費やしていると述べています肺腫瘍の場合など、医師が時々検査することもあります。さらに、上で述べたように、これらのアルゴリズムは、臨床医が探していないスキャン上のいくつかのデータポイントを検出できます。このような開発とX線へのAIの組み込みの拡大により、セグメントの成長が促進されると予想されます。

さらに、業界プレーヤーによる製品発売の増加がこの分野の成長を促進すると予想されます。例えば、富士フイルムが開発したAIを活用した胸部X線検査プログラム「CXR-AID」は、医薬品医療機器総合機構(PMDA)の認定を受け、2021年8月に日本でも利用可能となります。 LunitのAI技術を活用して作成されたCXR-AIDは、X線画像から胸部結節、硬化、気胸などの重大な異常所見を認識できます。

したがって、上記の要因により、このセグメントは分析期間中に成長すると予想されます。

北米が市場を独占しており、予測期間にも同様の成長が予想される

北米の診断市場におけるAIの使用は、医療システムにおける先進技術の使用の増加と国内の慢性疾患の負担の増大によって推進されています。

たとえば、米国がん協会が2022年 1月に発行した「Cancer Facts and Figures 2022」によると、2022年には推定190万人の新たながん症例が診断され、その内、前立腺がんが186,670人、次いで肺がんが169,870人と推定されています。、女性乳がんの症例は144,490件。がんの罹患率の増加と他の慢性疾患の重篤な負担により、正確な診断と治療の需要が高まっています。これにより、早期診断目的でのAIの採用が増加し、最終的には市場の成長が促進される可能性があります。

さらに、カナダ政府が発表し、2021年11月に発表した統計によると、2021年に約229,200人のカナダ人ががんと診断され、前立腺がんは引き続き最も多く診断されるがんと予想され、2021年にすべてのがん診断の46%を占めると予想されています。同じ情報源によると、女性の8人に1人が人生のある時点で乳がんに罹患します。したがって、がんの症例数が増加するにつれて早期診断の需要も高まり、予測期間を通じて診断向けAIの需要が高まります。

いくつかの市場関係者が戦略的イニシアチブの実施に取り組んでおり、市場の成長に貢献しています。たとえば、ロシュは2021年 12月に、乳がん向けに開発された3つのAIベースの深層学習画像分析調査Use Only(RUO)アルゴリズムを導入しました。さらに、2022年 4月、ベンダー中立のAIプラットフォームであるArterysは、堅牢なCardio AI臨床アプリケーションに対するいくつかの新しいモジュールと、ディープラーニングに基づく追加の(8番目の)食品医薬品局(FDA)AI認可を発表しました。

したがって、前述の要因は、北米地域の予測期間中の市場の成長に寄与する可能性があります。

診断向けAI業界の概要

診断向けAI市場は適度な競争があり、いくつかの主要企業で構成されています。現在市場を独占している企業としては、Siemens Healthineers、Nanox Imaging LTD(Zebra Medical Vision, Inc.)、Riverain Technologies、Vuno, Inc.、Aidoc、Neural Analytics、Imagen Technologies、Digital Diagnostics, Inc.、GE Healthcare、AliveCor Inc.、Enlitic、InformAIなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 医用イメージング分野におけるAIツールの需要の高まりと放射線科医の負担軽減への注目の高まり

- AIベースのテクノロジーの導入を促進する政府の取り組み

- AIベースのスタートアップへの資金調達の増加

- 市場抑制要因

- 医師の間でAIベースのテクノロジーの導入に消極的

- 高額な調達コストとメンテナンス

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ別

- in vitro診断

- 診断用イメージング

- MRI

- CT

- X線

- 超音波

- その他

- その他のタイプ

- 用途別

- 心臓病

- 腫瘍

- 神経

- 産科・婦人科

- その他

- エンドユーザー別

- 病院

- 画像診断センター

- 診断研究所

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Siemens Healthineers

- Nanox Imaging LTD(Zebra Medical Vision, Inc.)

- Riverain Technologies

- Vuno, Inc.

- Aidoc

- Neural Analytics

- Imagen Technologies

- Digital Diagnostics, Inc.

- GE Healthcare

- AliveCor Inc.

- Enlitic

- InformAI

第7章 市場機会と将来の動向

The Global Artificial Intelligence in Diagnostics Market size is estimated at USD 1.33 billion in 2024, and is expected to reach USD 5.57 billion by 2029, growing at a CAGR of 33.14% during the forecast period (2024-2029).

The COVID-19 pandemic has significantly impacted the healthcare system, particularly diagnostics. The lockdown measures worldwide decreased public mobility and impacted the diagnostic industry. Moreover, the COVID-19 pandemic not only affected the global economy but also greatly impacted the functioning of general hospital care for non-COVID-19 patients in hospitals across the globe. However, with the increasing demand for diagnostic imaging procedures globally, the demand for implementing artificial intelligence in diagnostics is also increasing. According to the article "Artificial intelligence in the diagnosis of COVID-19: challenges and perspectives," published in April 2021, at different levels of the healthcare system, including diagnosis, artificial intelligence (AI) has been implemented. Particularly during the current pandemic, AI algorithms are crucial for the quick diagnosis of COVID-19 patients.

Additionally, AI tools were employed to handle the pandemic's depth and complexity, from diagnosis to drug development, disease transmission prediction, and population monitoring and surveillance. A study titled "The Role of Artificial Intelligence in Fighting the COVID-19 Pandemic," published in the Journal of "Nature Public Health Emergency Collection" in April 2021, proposed a temporal step method, which includes presenting recent research investigations, examining how AI observes and acts on society and the healthcare system, and reporting various data types. Hence, the deployment of AI tools in diagnosing patients with SARS-CoV-2 played a substantial role throughout the pandemic phase, thereby augmenting the market growth.

Furthermore, factors such as increasing demand for AI tools in the medical imaging field and rising focus on reducing the workload of radiologists, government initiatives to increase the adoption of AI-based technologies, and growth in funding for AI-based start-ups are anticipated to bolster the growth of the market shortly.

Incorporating artificial intelligence into imaging devices may improve the diagnosis, which is expected to aid the overall market growth during the forecast period. For instance, the Journal of the American Medical Association article titled "An Artificial Intelligence-Based Chest X-ray Model on Human Nodule Detection Accuracy from a Multicenter Study," published in December 2021, reported that an artificial intelligence algorithm was associated with improved detection of pulmonary nodules on chest radiographs compared with unaided interpretation for different levels of detection difficulty and readers with different experience. The research articles stated that artificial intelligence could be a promising technology for medical imaging shortly.

Moreover, factors such as increasing funding for AI start-ups globally are increasing the demand for increasing incorporation of AI in the diagnostic imaging modalities. For instance, in March 2022, Qure.ai (Qure), a health-tech business raising USD 40 million in fundraising, employs artificial intelligence (AI) for medical imaging diagnostics. The company further declared that it would utilize the funding to broaden and improve its global presence, particularly in the United States and Europe, and accelerate the development of products for critical care and community diagnostics. Therefore, such fundraising is anticipated to contribute to market growth.

Thus, owing to the aforementioned factors, the market studied is anticipated to grow over the analysis period. However, the lack of a skilled AI workforce and ambiguous regulatory guidelines for medical software is expected to restrain the market's growth.

AI in Diagnostics Market Trends

X-rays Segment is Expected to Dominate the Market

The X-rays segment is expected to garner a significant market share during the forecast period. Since X-rays are the most common imaging test performed in most radiology departments, the potential for artificial intelligence (AI) to aid with the triage and interpretation of traditional radiographs (X-ray images) is particularly significant. Incorporating AI in X-rays enhances its efficiency, accuracy, ease of access, and workflow, reducing time and increasing quality and patient safety. These advantages are expected to increase the demand for AI in X-rays, boosting the segment's growth during the forecast period.

Additionally, the article titled "These Algorithms Look at X-Rays-and Somehow Detect Your Race," published in August 2021, stated that recently market players are heavily spending on innovations to create artificial intelligence software that interprets x-rays and for identifying conditions that doctors occasionally check, such as in the case of lung tumors. Additionally, as mentioned above, these algorithms can detect several data points on these scans that clinicians don't look for. Such developments and the growing incorporation of AI in X-rays are anticipated to drive segment growth.

Furthermore, the increase in product launches by the industry players is anticipated to drive the segment's growth. For instance, in August 2021, CXR-AID, a chest X-ray program powered by artificial intelligence (AI) developed by Fujifilm, will be made available in Japan after receiving certification from the Pharmaceuticals and Medical Devices Agency (PMDA). CXR-AID, which was created utilizing Lunit's AI technology, can recognize significant abnormal findings from X-ray images, such as chest nodules, consolidation, and pneumothorax.

Thus, owing to the abovementioned factors, the segment is expected to grow over the analysis period.

North America Dominates the Market and Expected to do Same in the Forecast Period

The use of artificial intelligence in the diagnostics market in North America is being driven by the increasing use of advanced technology in healthcare systems and the rising burden of chronic diseases in the country.

For instance, according to Cancer Facts and Figures 2022 published in January 2022 by the American Cancer Society, an estimated 1.9 million new cancer cases will be diagnosed in 2022, among which prostate cancer is estimated to be 186,670, followed by 169,870 cases of lung cancer, and 144,490 cases of female breast cancer. The increased prevalence of cancer and the high burden of other chronic diseases increase the demand for accurate diagnosis and treatment. This is likely to increase the adoption of AI for early diagnosis purposes, ultimately boosting the market growth.

Furthermore, according to statistics published by the Government of Canada and released in November 2021, about 229,200 Canadians were diagnosed with cancer in 2021, and prostate cancer is expected to remain the most diagnosed cancer, accounting for 46% of all cancer diagnoses in 2021. According to the same source, breast cancer affects one out of every eight women at some point in their lives. Thus, as the number of cancer cases rises, so does the demand for early diagnosis, driving demand for AI in diagnostics over the projection period.

Several market players are engaged in implementing strategic initiatives, contributing to the market's growth. For instance, in December 2021, Roche introduced three artificial intelligence (AI)-based, deep learning image analysis Research Use Only (RUO) algorithms developed for breast cancer. In addition, in April 2022, Arterys, the vendor-neutral AI platform, launched several new modules to its robust Cardio AI clinical application and an additional (eighth) Food and Drug Administration (FDA) AI clearance based on deep learning.

Therefore, the factors mentioned earlier will likely contribute to market growth over the forecast period in the North American region.

AI in Diagnostics Industry Overview

The Artificial Intelligence in Diagnostics Market is moderately competitive and consists of several major players. Some of the companies which are currently dominating the market are Siemens Healthineers, Nanox Imaging LTD (Zebra Medical Vision, Inc.), Riverain Technologies, Vuno, Inc., Aidoc, Neural Analytics, Imagen Technologies, Digital Diagnostics, Inc., GE Healthcare, AliveCor Inc., Enlitic, and InformAI.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For AI Tools in the Medical Imaging Field and Rising Focus On Reducing the Workload of Radiologists

- 4.2.2 Government Initiative to Increase the Adoption Of AI-Based Technologies

- 4.2.3 Growth in Funding for AI-Based Start-Ups

- 4.3 Market Restraints

- 4.3.1 Reluctance Among Medical Practitioners to Adopt AI-Based Technologies

- 4.3.2 High Procurement Costs and Maintenance

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 In Vitro Diagnostics

- 5.1.2 Diagnostic Imaging

- 5.1.2.1 MRI

- 5.1.2.2 CT

- 5.1.2.3 X-rays

- 5.1.2.4 Ultrasound

- 5.1.2.5 Others

- 5.1.3 Other Types

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Oncology

- 5.2.3 Neurology

- 5.2.4 Obstetrics/ Gynecology

- 5.2.5 Other Applications

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Imaging Centers

- 5.3.3 Diagnostic Laboratories

- 5.3.4 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Siemens Healthineers

- 6.1.2 Nanox Imaging LTD (Zebra Medical Vision, Inc.)

- 6.1.3 Riverain Technologies

- 6.1.4 Vuno, Inc.

- 6.1.5 Aidoc

- 6.1.6 Neural Analytics

- 6.1.7 Imagen Technologies

- 6.1.8 Digital Diagnostics, Inc.

- 6.1.9 GE Healthcare

- 6.1.10 AliveCor Inc.

- 6.1.11 Enlitic

- 6.1.12 InformAI