|

市場調査レポート

商品コード

1644594

世界の車載用MCU-市場シェア分析、産業動向・統計、成長予測(2025~2030年)Global Automotive MCU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の車載用MCU-市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

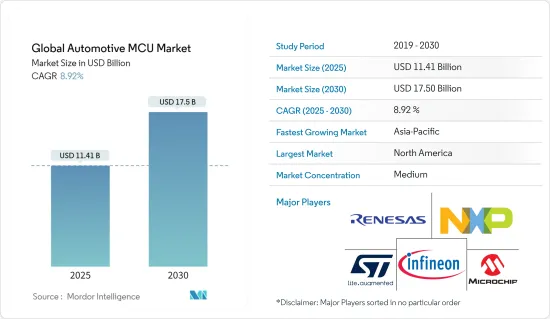

車載用MCUの世界市場規模は、2025年に114億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.92%で、2030年には175億米ドルに達すると予測されます。

極端な動作条件に対応し、極端な温度下でもリアルタイム応答と高信頼性を提供し、自動車設計の課題に対応する機能安全機能を組み込んだデバイスに対する需要の高まりが、調査対象市場の成長に有利な機会を提供すると予想されます。

主要ハイライト

- 自動化の進展により、自動車機能の自動運転を担うマイクロコントローラのニーズが高まっています。MCUは、排気システムを清潔に保ち、さまざまな車両部品に電力を分配し、燃料消費を削減するといった自動機能を実行するために自動車に使用されています。さらに、自動車の電動化により、電気自動車(EV)のニーズに最適化された新しい特殊なMCUの必要性が生じています。EV需要の急増に対応するため、市場の各社は先進的な製品を革新し、大規模な研究開発プロジェクトに投資しています。

- 例えば、STは2022年2月、ゾーン・アーキテクチャ関連のソリューションに弾みをつけるべく、ソフトウェア定義のEV向けに最適化された新製品Stellar E MCUを発表しました。 32ビット、300 MHzのArm Cortex-M7コアを中心に構築されています。このMCUは、1コアあたり最大2MBのオンチップ・フラッシュと16Kバイトのキャッシュを備えています。新しいMCUは、Stellarファミリの拡大製品で、強力な集中型ドメイン・ゾーン・コントローラとして、ゾーン・アーキテクチャ自動車の設計とスケーラビリティを簡素化することを目的としています。また、新しいMCUは、EVの効率的な電力変換の主力となっているシリコンカーバイドなどのワイドバンドギャップパワーエレクトロニクスを容易に制御できるようにすることを目的としています。

- さらに、2021年7月には、電気自動車用モーター制御ユニットのメーカーであるSterling Gtake E-mobility Ltd.が、大手電動二輪車メーカーから6億インドルピー相当の受注を獲得したと発表しました。同社はまた、二輪車や三輪車の乗用車、商用車など、さまざまな車種向けにモーター制御ユニット(MCU)を供給するため、20社以上の電気自動車(EV)メーカーと協議を進めていると述べました。

- その反面、世界の自動車産業がCOVID-19による販売不振から回復しつつある中、による危機がその復活に水を差しています。世界の半導体不足は世界の自動車生産を混乱させ、新車販売の遅れを引き起こす可能性があります。最新のインフォテインメントシステム、アンチロック・ブレーキシステム(ABS)、先進運転支援システム(ADAS)、その他の電子安定システムで使用される電子制御ユニットの重要な部品であるマイクロコントローラは供給不足に陥っており、自動車メーカーは減産を余儀なくされています。その結果、自動車メーカーは供給不足が緩和されるまで、選択的に工場を休止しています。しかし、近い将来、市場は急速に進展すると予想されます。

- さらに、極端な気候条件下では車載用MCUが動作不良を起こす可能性があり、設計の複雑さも相まって市場の成長を妨げる可能性があります。

車載マイコン市場の動向

ADAS需要の急増が市場成長を牽引

- 世界保健機関(WHO)によると、交通事故が原因で毎年約130万人が死亡しており、ほとんどの国で国内総生産(GDP)の約3%が犠牲になっています。さらに、Safe International Road Travelによると、米国では毎年4万6,000人以上が交通事故で亡くなっています。米国の交通事故死亡率は人口10万人当たり12.4人です。さらに440万人が、手当てを必要とするほどの重傷を負っています。交通事故は米国における1~54歳の死因の第1位です。また、米国は高所得国の中で交通事故死者数が最も多く、西欧、カナダ、オーストラリア、日本の同種の国よりも約50%も多いです。

- ADAS(先進運転支援システム)を搭載した自動車は、道路上の物体を検知・分類し、道路状況に応じてドライバーに警告を発することができます。さらに、これらのシステムは状況に応じて車両を自動的に減速させることができます。安全上不可欠なADAS用途には、歩行者検知・回避、車線逸脱警告・修正、交通標識認識、自動緊急ブレーキ、死角検知などがあります。これらの人命救助システムは、ADAS用途を確実に成功させるために極めて重要であり、最新のインターフェース規格を取り入れ、複数のビジョンベースのアルゴリズムを実行して、リアルタイムマルチメディア、ビジョン・コプロセッシング、センサフュージョン・サブシステムをサポートします。

- National Safety Councilによると、ADAS技術は年間20,841人の死亡を防ぐ可能性があり、これは交通事故死者全体の約62%に相当します。ADAS(先進運転支援システム)の出現により、設計者のマイクロコントローラ(MCU)の使用方法、仕様、製造方法が変化しています。ADASの進化と複雑な性質は、調査された市場において技術革新、コラボレーション、技術的ブレークスルーのためのいくつかの機会を提供すると予想されます。

- 例えば、2022年4月、中国のスマートカー・マイクロチップ設計会社であるSemiDrive Technology Ltd.は、E3シリーズ・マイクロコントローラを発表しました。この車載マイコンはTSMC 22nm車載グレードを採用し、シャーシ・バイ・ワイヤ、ブレーキ制御、BMS、ADAS、LCDパネル、HUD、ストリーミングメディアシステム、CMSなど多くの車載用途セグメントで使用できます。高い安定性と安全性を実現するよう設計されています。車両仕様はAEC-Q100グレード1、機能安全規格はISO 26262 ASIL Dです。

- さらに2022年3月、先進半導体ソリューションのサプライヤーであるルネサスエレクトロニクスは、ADAS(先進運転支援システム)セグメントでのホンダとの協業拡大を発表しました。Hondaは、Honda SENSING Eliteシステムにルネサスの車載用SoC(System on a Chip)「R-Car」と車載用MCU「RH850」を採用しました。Honda SENSING Elite(2021年3月発売の「レジェンド」に搭載)は、レベル3の自動運転(限定領域での条件付き自動運転)に適合する先進技術を搭載しています。さらにHondaは、全方位安全運転支援システム「Honda SENSING 360」にR-CarとRH850を採用し、先行技術の研究開発で得た知見やノウハウを生かしています。

高い市場成長が期待されるアジア太平洋

- 環境問題への関心の高まりと政府の補助金制度の増加は、燃費の良さ、性能の向上、リーズナブルな価格といった要素と相まって、アジア太平洋におけるハイブリッド電気自動車の普及率を高めています。

- 例えば、EV-Volumes.comによると、2021年にはアジア太平洋で約67万2,900台のプラグインハイブリッド電気自動車(PHEV)が販売されました。これは、約26万4,260台のプラグインハイブリッド電気自動車が販売された2020年から飛躍的に増加しました。このような自動車の需要増は、同地域の車載用MCUメーカーの成長を後押しする可能性が高いです。

- さらに、アジア太平洋は半導体と半導体ベースのデバイス製造の重要な拠点として浮上しています。例えば、世界半導体貿易統計(WSTS)の推定によると、アジア太平洋(日本を除く)の半導体産業の売上高は、2019年に2,578億8,000万米ドル、2021年には2,908億5,000万米ドルでした。この地域には著名なエレクトロニクス企業や自動車製造企業もあるため、研究市場の進化の余地があります。

- 自動車システム設計の将来は、車両集中型、ゾーン指向のE/Eアーキテクチャにあり、将来の車両世代に向けたこれらの革新的アーキテクチャが生み出す課題に対処する自動車用チップの必要性が高まっています。この地域の企業は、消費者のニーズに応えるために先進的なソリューションを発表しています。

- 例えば、Renesas Electronics Corporation(日本、東京)は2021年11月、複数の用途を1つのチップに統合し、進化する電気-電子(E/E)アーキテクチャ向けの統合電子制御ユニット(ECU)を実現するニーズの高まりに対応するために設計された、強力な新しいマイクロコントローラ(MCU)グループ、RH850/U2B MCUを発表しました。クロスドメインRH850/U2B MCUは、ハイブリッド内燃機関車やxEVのトラクションインバータ、コネクテッドゲートウェイ、ハイエンド・ゾーン・コントロール、ドメイン・コントロール用途など、車両運動で要求される厳しいワークロードに対応するように設計されています。

車載用マイクロコントローラ産業概要

世界の車載用MCU市場は、Infineon Technologies AG、Microchip Technology Inc.、NXP Semiconductors、Texas Instruments Incorporatedなどの有力企業が存在し、適度にセグメント化されています。市場競争、消費者の嗜好の頻繁な変化、急速な技術進歩は、予測期間中の市場成長に脅威をもたらすと予想されます。

- 2022年1月-Infineon Technologiesは、AURIXマイクロコントローラファミリの拡大と、次世代eMobility、ADAS、車載E/Eアーキテクチャ、手頃な価格の人工知能(AI)向けの新しい28nmマイクロコントローラAURIX TC4xファミリの最初のサンプル出荷を発表しました。この新ファミリーは、当社の主要製品であるAURIX TC3x MCUファミリーの上位マイグレーションパスを記載しています。次世代TriCore 1.8とAURIXアクセラレータ・スイートによるスケーラブルな性能強化が特徴です。

- 2021年4月-Nuvoton Technology Corporationは、最大50MHz動作、AEC-Q100グレード2認定、CAN(Controller Area Network)2.0 Bインタフェース内蔵の車載向けArm Cortex-M0 NUC131U 32ビットマイクロコントローラの新シリーズを発表しました。6組のUART、2組のI2C、1組のSPI、24チャネルの100 MHz PWMからなる豊富なペリフェラルを備え、ステッピング・モーターや空調用コンプレッサーを正確に制御できます。12ビットADCは最大800k SPSを提供し、車載用途の電圧、電流、または温度センサを検知して、外付け周辺コンポーネントの数を減らし、最終製品のフォームファクターを削減します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の想定と市場の定義

- 調査範囲

第2章 調査手法

- 調査の枠組み

- 2次調査

- 1次調査

- 1次調査のアプローチと主要回答者

- データの三角測量と洞察の生成

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- バリューチェーン分析

- COVID-19の市場への影響評価

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- モノのインターネット(IoT)の出現

- 電子自動車(EV)の需要急増

- 自動車におけるインフォテインメント人気の高まり

- 市場課題/抑制要因

- 極端な気候条件下での動作不良

- 設計の複雑さ

- 市場機会

- 技術の進歩と革新

第6章 市場セグメンテーション

- 製品別

- 8ビット

- 16ビット

- 32ビット

- 用途別

- パワートレインとシャーシ

- セーフティ&セキュリティ

- ボディエレクトロニクス

- テレマティクスとインフォテインメント

- 車種別

- 乗用車内燃機関車

- 商用内燃機関車

- 電気自動車

- BEV

- HEV

- PHEV

- FCEV

- 地域別

- 北米

- 欧州

- アジア太平洋

- その他

第7章 競合情勢

- 企業プロファイル

- Infineon Technologies AG

- Microchip Technology Inc.

- NXP Semiconductors

- Renesas Electronics Corporation

- STMicroelectronics

- Texas Instruments Incorporated

- Toshiba Electronic Devices & Storage Corporation

- Analog Devices Inc.

- ROHM Semiconductor

- Broadcom Inc.

第8章 投資分析

第9章 市場の将来

The Global Automotive MCU Market size is estimated at USD 11.41 billion in 2025, and is expected to reach USD 17.50 billion by 2030, at a CAGR of 8.92% during the forecast period (2025-2030).

An increased demand for devices designed for extreme operating conditions, providing real-time response and high reliability, even in extreme temperatures, and incorporating features for functional safety to meet automotive design challenges, is expected to offer lucrative opportunities for growth of the studied market.

Key Highlights

- The rise in automation has generated a significant need for microcontrollers responsible for the automatic operation of vehicle functions. MCUs are being used in automobiles to perform automatic functions like keeping the exhaust system clean, distributing electricity to various vehicle components, and reducing fuel consumption. Further, the electrification of vehicles is creating a need for new and specialized MCUs that are optimized for the needs of electric vehicles (EVs). To cater to the upsurge in demand for EVs, companies in the market are innovating advanced products and investing in extensive R&D projects.

- For instance, aiming to keep the impetus going for zonal architecture-related solutions, in February 2022, ST released Stellar E MCUs, a new offering optimized for software-defined EVs Built around 32-bit, 300 MHz Arm Cortex-M7 cores. The MCUs feature up to 2 MB of on-chip Flash and 16 Kbyte of cache per core. The new MCUs, an extension of the Stellar family, are meant to be powerful, centralized domain and zone controllers to simplify design and scalability for a zonal architecture automobile. Also, the new MCUs aim to allow for easy control of wide-bandgap power electronics, such as silicon carbide, which has become a mainstay for efficient power conversion in EVs.

- Additionally, in July 2021, Sterling Gtake E-mobility Ltd, a manufacturer of motor control units for electric vehicles, announced that it had bagged an order worth INR 60 crore from a leading electric two-wheeler maker. The company said it is also in the advanced stages of discussions with over 20 electric vehicle (EV) manufacturers to supply motor control units (MCUs) for different vehicle types, including two-wheelers and three-wheelers passenger vehicles and commercial vehicles.

- On the flip side, as the global automotive sector is recovering from a slump in sales caused by Covid-19, another crisis is dampening its revival. A global semiconductor shortage disrupts global automotive production and may cause a delay in the sales of new vehicles. Microcontrollers, a crucial component of electronic control units used in modern infotainment systems, anti-lock braking systems (ABS), advanced driver assist systems (ADAS), and other electronic stability systems are in short supply forcing carmakers to reduce output. Resultantly, the carmakers are selectively idling plants until the shortage eases. However, the market is expected to make quick progress in the near future.

- Moreover, the possibilities of operational failure of the automotive MCUs in extreme climatic conditions, coupled with their design complexity, might hamper the growth of the studied market.

Automotive Microcontrollers Market Trends

Surging Demand for ADAS is Likely to Drive the Market Growth

- According to World Health Organization (WHO), approximately 1.3 million people die each year due to road traffic crashes which cost most countries approximately 3% of their gross domestic product (GDP). Further, according to Safe International Road Travel, more than 46,000 people die in crashes on U.S. roadways every year. The U.S. traffic fatality rate is 12.4 deaths per 100,000 inhabitants. An additional 4.4 million are injured seriously enough to require medical attention. Road crashes are the leading cause of death in the U.S. for people aged 1-54. Also, the U.S. suffers the most road crash deaths of any high-income country, about 50% higher than similar countries in Western Europe, Canada, Australia, and Japan.

- Vehicles installed with Advanced Driver Assistance Systems (ADAS) can detect and classify objects on the road and alert drivers according to the road conditions. Additionally, these systems can automatically decelerate vehicles, depending on the situation. A few essential safety-critical ADAS applications include pedestrian detection/avoidance, lane departure warning/correction, traffic sign recognition, automatic emergency braking, blind-spot detection, etc. These lifesaving systems are crucial to ensuring the success of ADAS applications, incorporating the latest interface standards, and running multiple vision-based algorithms to support real-time multimedia, vision co-processing, and sensor fusion subsystems.

- According to National Safety Council, ADAS technologies have the potential to prevent 20,841 deaths per year, or about 62% of total traffic deaths. The emergence of advanced driver assistance systems (ADAS) is changing how designers use, specify, and manufacture microcontrollers (MCUs). The evolving and complex nature of ADAS is expected to offer several opportunities for innovation, collaborations, and technological breakthroughs in the studied market.

- For instance, in April 2022, SemiDrive Technology Ltd., a Chinese smart car microchip designer, released its E3 series microcontrollers. The automotive microcontroller adopts a TSMC 22nm automotive grade which can be used in many automotive application fields such as chassis by wire, brake control, BMS, ADAS, LCD panel, HUD, streaming media system, and CMS, among others. It is designed to reach high stability and safety levels. Its vehicle specification is AEC-Q100 Grade 1, and the functional safety standard is ISO 26262 ASIL D.

- Moreover, in March 2022, Renesas Electronics, a supplier of advanced semiconductor solutions, announced the expansion of its collaboration with Honda in the field of advanced driver-assistance systems (ADAS). Honda adopted Renesas' R-Car automotive system on a chip (SoC) and RH850 automotive MCU for its Honda SENSING Elite system. Honda SENSING Elite (featured in the Legend, which went on sale in March 2021) incorporates advanced technology that qualifies for Level 3 automated driving (conditional automated driving in limited areas). Further, Honda has selected R-Car and RH850 for use in the Honda SENSING 360 omnidirectional safety and driver assistance system, which builds on the knowledge and expertise gained through research and development work on the earlier technology.

The Asia Pacific Region is Expected to Witness a High Market Growth

- The growing environmental concerns and rising government subsidy programs, coupled with factors such as better fuel economy, enhanced performance, and reasonable cost, are augmenting the penetration rate of hybrid electric vehicles in the Asia-Pacific region.

- For instance, according to EV-Volumes.com, approximately 672.9 thousand plug-in hybrid electric vehicles (PHEVs) were sold across the Asia-Pacific region in 2021. This was a dramatic increase from 2020 when around 264.26 thousand plug-in hybrid electric vehicles were sold. The increasing demand for these vehicles is likely to boost the maker growth of automotive MCUs in the region.

- Further, the Asia Pacific has emerged as a significant hub for manufacturing semiconductors and semiconductor-based devices. For instance, according to World Semiconductor Trade Statistics (WSTS) estimates, the semiconductor industry revenue in the Asia Pacific region (excluding Japan) was USD 257.88 billion in 2019 and USD 290.85 billion in 2021. The region is also home to prominent electronics and automotive manufacturing companies, thus, offering scope for the evolution of the studied market.

- The future of automotive system design lies in a vehicle-centralized, zone-oriented E/E architecture, which heightens the need for automotive chips that address the challenges these innovative architectures create for future vehicle generations. The companies in the region are launching advanced solutions to cater to the needs of their consumers.

- For instance, in November 2021, Renesas Electronics Corporation (Tokyo, Japan) introduced a powerful new group of microcontrollers (MCUs), the RH850/U2B MCUs, designed to address the growing need to integrate multiple applications into a single chip and realize a unified electronic control unit (ECU) for the evolving electrical-electronic (E/E) architecture. Delivering a combination of flexibility, high performance, freedom from interference, and security, the cross-domain RH850/U2B MCUs are built for the rigorous workloads required by vehicle motion in terms of hybrid ICE and xEV traction inverter, connected gateway, high-end zone control, and domain control applications.

Automotive Microcontrollers Industry Overview

The global automotive MCU market is moderately fragmented with the presence of prominent players like Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductors, Texas Instruments Incorporated, etc. The competition, frequent changes in consumer preferences, and rapid technological advancements are expected to pose a threat to the market's growth during the forecast period.

- January 2022 - Infineon Technologies announced the extension of its AURIX microcontroller family and the availability of the first samples of its new AURIX TC4x family of 28nm microcontrollers for next-generation eMobility, ADAS, automotive E/E architectures, and affordable artificial intelligence (AI) applications. The new family delivers an upward migration path for the company's leading AURIX TC3x MCU family. It features the next-generation TriCore 1.8 and scalable performance enhancements from the AURIX accelerator suite.

- April 2021 - Nuvoton Technology Corporation launched a new series of Arm Cortex-M0 NUC131U 32-bit microcontrollers for automotive applications, running up to 50 MHz, qualified by AEC-Q100 Grade 2 and build-in Controller Area Network (CAN) 2.0 B interface. It is equipped with a rich peripheral comprising six sets of UARTs, two sets of I2Cs, 1 set of SPI, and 24 channels of 100 MHz PWM to make accurate control to drive both stepping motor or HVAC compressor. 12-bit ADC delivers up to 800 k SPS to sense voltage, current, or temperature sensors for automotive applications to reduce the number of external peripheral components and the form factor of the end product.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Defination

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Primary Research Approach And Key Respondents

- 2.5 Data Triangulation And Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power Of Suppliers

- 4.2.2 Bargaining Power Of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat Of Substitutes

- 4.2.5 Intensity Of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of the Impact of Covid-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of Internet of Things (IoT)

- 5.1.2 Surge in demand for electronic vehicles (Evs)

- 5.1.3 Increasing popularity of infotainment in automobiles

- 5.2 Market Challenges/Restraints

- 5.2.1 Operational failure in extreme climatic conditions

- 5.2.2 Design Complexity

- 5.3 Market Opportunities

- 5.3.1 Technological Advancements and Innovations

6 MARKET SEGMENTATION

- 6.1 Segmentation - By Product

- 6.1.1 8-bit

- 6.1.2 16-bit

- 6.1.3 32-bit

- 6.2 Segmentation - By Application

- 6.2.1 Powertrain and Chassis

- 6.2.2 Safety and Security

- 6.2.3 Body Electronics

- 6.2.4 Telematics and Infotainment

- 6.3 Segmentation - By Vehicle Type

- 6.3.1 Passenger ICE vehicle

- 6.3.2 Commercial ICE vehicle

- 6.3.3 Electric Vehicle

- 6.3.3.1 BEV

- 6.3.3.2 HEV

- 6.3.3.3 PHEV

- 6.3.3.4 FCEV

- 6.4 Segmentation - By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Microchip Technology Inc.

- 7.1.3 NXP Semiconductors

- 7.1.4 Renesas Electronics Corporation

- 7.1.5 STMicroelectronics

- 7.1.6 Texas Instruments Incorporated

- 7.1.7 Toshiba Electronic Devices & Storage Corporation

- 7.1.8 Analog Devices Inc.

- 7.1.9 ROHM Semiconductor

- 7.1.10 Broadcom Inc.