|

市場調査レポート

商品コード

1437321

手術室統合:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Operating Room Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 手術室統合:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

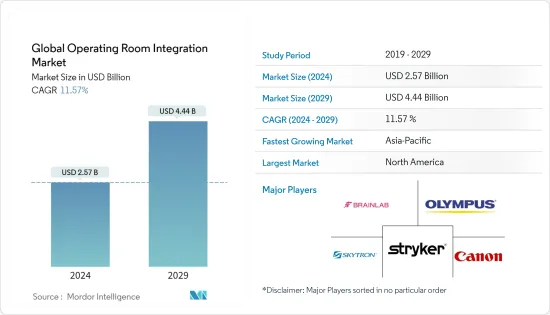

世界の手術室統合市場規模は、2024年に25億7,000万米ドルと推定され、2029年までに44億4,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に11.57%のCAGRで成長します。

COVID-19で、手術を待つ患者にかなりの待ち時間が生じた。 British Journal of Surgeryに掲載された研究によると、COVID-19の影響で、2020年には世界で2,800万件の手術が延期またはキャンセルされ、数百万件の手術が2021年に延期されました。したがって、数千人の患者が手術の遅れに直面しているため、スケジュールの効率を高める必要性が高まっています。より重要になります。さらに、パンデミックにより市場関係者は新たな方法での運営を迫られ、デジタル化が加速しています。パンデミックによる術前計画、ビデオ会議、遠隔での術後の患者関与の増加に対応して、手術室と手術手順は次の3つの方法で変更されました。

低侵襲手術に対する患者の急増などの要因が市場成長の主な要因となっています。これは主に、肥満などの症状を治療するための外科的介入に対する意識が高まり、医療機器メーカーが高度な手術室統合の開発を進めてきたためです。さらに、高齢者人口の増加により手術需要が高まり、手術件数が累積的に増加することも市場の成長を促進すると予想されます。たとえば、2020年の「米国における高齢者における大手術の発生率と累積リスク」というタイトルの記事では、高齢者100人当たり年間9件近くの大手術が行われており、メディケア受給者の7人に1人以上が再手術を受けていると述べた。 500万人近くの高齢者を対象とした5年間にわたる大規模な手術。

さらに、末期の慢性疾患は一般的に手術を必要とするため、世界中で慢性疾患の負担が増大していることも、手術室の需要を増加させる主な要因の1つです。たとえば、米国保健協会によると、2022年に手術室が活動を再開し、医療健康治療と手術の急増が観察され、その結果、2020年末までの手術率は2019年と比較して10%しか低下しませんでした。 ,経済協力開発機構(OECD)によると、2020年にトルコで報告された白内障手術の件数は393,901件でした。同情報源によると、2020年のイタリアにおける人工股関節置換術の件数は84,647件、帝王切開の件数は約114,601件でした。したがって、この外科手術数の増加により、手術室の需要が増加し、それによって市場の成長に貢献すると考えられます。

したがって、上記の要因は、予測期間中に市場の成長を促進すると予想されます。

手術室統合市場動向

心臓血管外科セグメントは、手術室統合市場で主要な市場シェアを保持すると予想される

新型コロナウイルス感染症(COVID-19)の突然の発生により、さまざまな政府が世界中で突然の制限を課したため、市場の成長が妨げられたように見えました。これによりサプライチェーンの人員が削減され、製造プロセスにも影響が出ました。しかし、パンデミック後の期間における厳格なロックダウンの緩和により、患者の流入が増加し、それによって市場の成長が促進されました。

心臓血管疾患および関連手術が世界中で急増しているため、心臓血管外科セグメントは調査対象市場で圧倒的なシェアを保持すると予想されます。たとえば、欧州心臓ネットワークが2021年に発表したデータによると、欧州連合では6,000万人以上が心血管疾患を患っており、毎年 1,300万人近くが新たに心血管疾患と診断されています。さらに、肥満などの不健康なライフスタイルによって引き起こされる病気の負担が増加しているため、過体重が市場の成長を促進すると予想されています。 2020年にA-mansia Biotechが発表した論文では、世界中で20億人以上の18歳以上の成人が太りすぎであると述べています。このうち、世界中で6億5,000万人以上が肥満です。世界保健機関(WHO)は2021年、タバコ使用などの修正可能な行動危険因子が毎年720万人以上の死亡の原因となっており、年間160万人が身体活動不足に起因している可能性があると発表しました。 2021年に英国心臓財団が発表した研究によると、2020年に英国で約37万1,000件の心臓手術と手術が行われました。また、2021年に米国心臓協会が発表した論文によると、米国では毎年約4万人の子供が先天性心臓手術を受けています。このような心臓血管手術の数の増加は、心臓血管手術の需要の増加と手術室統合手順の改善につながります。

したがって、上記の要因は、予測期間中に調査対象セグメントの成長を促進すると予想されます。

北米は市場で重要なシェアを保持すると予想されており、予測期間にも同様のシェアを獲得すると予想されます。

米国は、この地域での慢性疾患の蔓延と高度な外科的治療法の採用の増加により、世界市場を主導する可能性が高いです。たとえば、国立慢性疾患予防健康増進センター(2021年 1月)によると、米国の成人 10人中6人が慢性疾患を患っており、成人 10人中4人が2つ以上の慢性疾患を抱えており、これらの症状が引き起こされています。この国のヘルスケア制度には約3兆8,000億米ドルのヘルスケア費がかかっています。さらに、米国の手術室統合市場の高い成長の可能性により、同国で事業を展開している企業は競合他社よりも優位に立つための市場戦略を申請しており、これにより調査対象となっている米国の市場の成長がさらに拡大すると予想されています。予測期間中の国。たとえば、Getingeは2021年 6月に、AIベースの手術室管理システム「Torin」を米国でリリースしたことを明らかにしました。

さらに、研究開発活動の増加、先進技術への迅速な適応、良好なヘルスケアインフラの存在により、地域市場全体の成長が大幅に促進されています。

手術室統合業界の概要

手術室統合市場は細分化されており、競争が激しく、いくつかの主要企業で構成されています。市場シェアの点では、現在、いくつかの大手企業が市場を独占しています。現在市場を独占している企業としては、Brain Lab AG、Canon Inc.、Doricon Medical Systems、Getinge AB、Karl Storz GMBH、Olympus Corporation、Merivaara Corp.、Steris PLC、Stryker Corporation、Skytron LLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 外科手術件数の増加

- 低侵襲手術を求める患者の急増と手術室での患者の安全への懸念

- 市場抑制要因

- 手術室統合のコストとメンテナンスが高い

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- コンポーネント別

- ソフトウェア

- サービス

- 用途別

- 一般外科

- 整形外科

- 心臓血管外科

- 脳神経外科

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Brain Lab AG

- Canon Inc

- Doricon Medical Systems

- Getinge AB

- Karl Storz GMBH &Co. KG

- Olympus Corporation

- Merivaara Corp.

- Steris PLC

- Stryker Corporation

- Skytron LLC

第7章 市場機会と将来の動向

The Global Operating Room Integration Market size is estimated at USD 2.57 billion in 2024, and is expected to reach USD 4.44 billion by 2029, growing at a CAGR of 11.57% during the forecast period (2024-2029).

The COVID-19 caused considerable wait times for patients standing by for surgery. A study published in the British Journal of Surgery showed that COVID-19 led to 28 million postponed or canceled surgeries globally in 2020 with millions of surgeries pushed into 2021. Thus, with thousands of patients facing delays in surgeries the necessity to enhance scheduling efficiencies has become more important. Furthermore, the pandemic has pushed market players to operate in new ways, thus accelerating digitization. Operating rooms and surgical procedures changed in the following three ways in response to the pandemic-increased pre-surgical planning, video conferencing, and remote post-surgical patient engagement.

The factors such as a surge in patient procedures for minimally invasive surgeries are the major driving factors for the growth of the market. This is mainly due to the increasing awareness about the surgical interventions to treat conditions such as obesity has led medical device manufacturers to develop advanced operating room integration. Additionally, growth in the geriatric population resulting in the rising demand for surgeries which results in a cumulative increase in the number of operating procedures is also expected to drive the growth of the market. For instance, in 2020, the article titled 'The Incidence and Cumulative Risk of Major Surgery in Older Persons in the United States mentioned that nearly 9 major surgeries were performed annually for every 100 older persons, and more than 1 in 7 Medicare beneficiaries underwent a major surgery over 5 years, representing nearly 5 million unique older people.

Moreover, the rising burden of chronic disease across the globe is also one of the major factors increasing the demand for the operating room, as end-stage chronic diseases generally demand surgery. For instance, as per the American Health Association, in 2022, operating rooms resumed their activities and observed an upsurge in medical health treatments and surgeries, leading to only a 10% lower rate of surgery by the end of 2020 in comparison to 2019. Moreover, per the Organization for Economic Cooperation and Development (OECD), the number of cataract surgical procedures reported in 2020 in Turkey was 393,901. According to the same source, the number of hip replacement procedures in Italy in 2020 was 84,647, and cesarean section procedures were approximately 114,601. Thus, this growth in the number of surgical procedures will likely increase the demand for the operating room, thereby contributing to market growth.

Thus the above-mentioned factors are expected to drive the growth of the market during the forecast period.

Operating Room Integration Market Trends

The Cardiovascular Surgery Segment is Expected to Hold a Major Market Share in the Operating Room Integration Market

The sudden outbreak of COVID-19 seemed to impede the growth of the market due to the sudden imposition of restrictions across the world by different governments. This reduced the manpower in the supply chain and also affected the manufacturing processes as well. However, the relaxation of strict lockdowns during the post-pandemic period has increased the patient influx and thereby propelling the growth of the market.

The Cardiovascular surgery segment is expected to hold a dominating share in the studied market owing to the surge in cardiovascular diseases and related surgeries across the globe. For instance, The data published by the European Heart network in 2021 reported that in the European Union, more than 60 million people live with cardiovascular disease and that close to 13 million new cases of cardiovascular diseases are diagnosed every year. Moreover, with the rising burden of diseases caused by unhealthy lifestyles, such as obesity, being overweight is expected to drive the growth of the market. The article published by A-mansia Biotech in 2020 states that more than 2 billion adults 18 years and older were overweight across the world. Of these, over 650 million were obese in the world. The World Health Organization (WHO) published in 2021 that modifiable behavioral risk factors such as tobacco use account for over 7.2 million deaths every year, and 1.6 million deaths annually can be attributed to insufficient physical activity. As per the study published by the British Heart Foundation in 2021, Around 371,000 heart procedures and operations in England in 2020. Also, the article published by the American Heart Association in 2021, Approximately 40,000 children undergo congenital heart surgery in the United States each year. Such an increasing number of cardiovascular surgeries leads to the rise in the demand for cardiovascular surgery and better operating room integration procedures.

Thus, the above-mentioned factors are expected to drive the growth of the studied segment during the forecast period.

North America is Expected to Hold a Significant Share in the Market and is expected to do the Same in the Forecast Period.

The United States is likely to command the global market due to the growing prevalence of chronic diseases and the rising adoption of advanced surgical treatment methodologies in the region. For instance, as per the National Center for Chronic Disease Prevention and Health Promotion (January 2021), 6 in 10 adults in the United States have a chronic disease, and 4 in 10 adults have two or more chronic diseases, and these conditions are posing around USD 3.8 trillion of healthcare costs on the country's healthcare system. Furthermore, due to the high growth potential of the United States operating room integration market, the companies operating in the country are filing for market strategies to have the edge over their competitors, which is further expected to augment the growth of the studied market in the country over the forecast period. For instance, in June 2021, Getinge revealed that it released the 'Torin' AI-based OR management system in the United States.

Additionally, an increase in research and development activities, quick adaptability to advanced technology, and the presence of favorable healthcare infrastructure are fueling the growth of the overall regional market to a large extent.

Operating Room Integration Industry Overview

The operating room integration market is fragmented and competitive and consists of several major players. In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Brain Lab AG, Canon Inc., Doricon Medical Systems, Getinge AB, Karl Storz GMBH, Olympus Corporation, Merivaara Corp., Steris PLC, Stryker Corporation, Skytron LLC, and others..

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in number of surgical procedures

- 4.2.2 Surge in patient preference for minimally invasive surgeries and Patient Safety concerns in operating room

- 4.3 Market Restraints

- 4.3.1 High cost and maintenance of the operating room integration

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Orthopedic Surgery

- 5.2.3 Cardiovascular Surgery

- 5.2.4 Neurosurgery

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Brain Lab AG

- 6.1.2 Canon Inc

- 6.1.3 Doricon Medical Systems

- 6.1.4 Getinge AB

- 6.1.5 Karl Storz GMBH & Co. KG

- 6.1.6 Olympus Corporation

- 6.1.7 Merivaara Corp.

- 6.1.8 Steris PLC

- 6.1.9 Stryker Corporation

- 6.1.10 Skytron LLC