|

市場調査レポート

商品コード

1651046

テレコムビリング・収益管理:市場シェア分析、業界動向と統計、成長予測(2025年~2030年)Telecom Billing Revenue Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| テレコムビリング・収益管理:市場シェア分析、業界動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年02月03日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

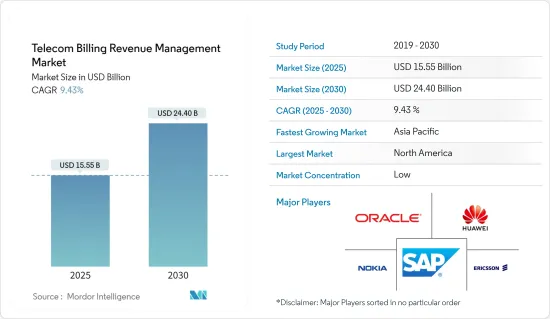

テレコムビリング・収益管理の市場規模は2025年に155億5,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは9.43%で、2030年には244億米ドルに達すると予測されます。

世界中の通信サービス・プロバイダー(CSP)では加入者が増加しており、ネットワークの輻輳や通話障害など、重大な問題を引き起こしています。こうした問題を抑制するため、ユーザーはCSPに対して効率的かつ効果的なビリング・収益管理システムの導入を求め始めています。

主なハイライト

- テレコムビリング・収益プロセスには、通信サービスだけでなく債権回収の管理も含まれます。ビリング・請求情報の計算、顧客の支払いや請求書の管理、データ利用に関する情報提供などが含まれます。通信ネットワークを最適化することで、これらのソリューションは通信事業者やデジタル・サービス・プロバイダーによって頻繁に採用され、業務効率を高めています。

- この10年間で、世界の通信市場は劇的に変化しました。インターネットを介して顧客とやり取りするクラウドネイティブ・ビジネスの台頭から、コンテンツ、アプリケーション、サービスのクラウドへの急速な移行まで。CSPプロバイダーは、この需要に対応するため、何十億もの資金を投じてネットワークをアップグレードしてきました。しかし、多くのCSPは、より近代的な収益管理機能を必要とする従来のビジネス・サポート・システムで運営を続けています。そのため、世界中の多くのCSPが現行のビリング・収益管理システムを採用しています。

- テレコムビリング・収益管理プラットフォーム・ソリューションは、通信サービス・プロバイダーが市場で最新のサービスを開始することを可能にし、顧客との関係を活用するのに役立ちます。また、SaaS(Software-as-a-Service)プラットフォームの登場は、市場の成長をさらに促進します。

- 電気通信業界のベンダーは、これらのソフトウェア・ソリューションを使用して、周波数帯の異常を検出・管理し、最終的には運用コストの削減に役立てています。また、これらの技術対応プログラムは、問題を修正し、ネットワークサービスと可視性を最適化する新たな対策を展開することで、CSPの収益増加をさらに支援します。

- さらに、現在の市場シナリオでは、CSPは、新しいユースケース、デバイス、ビジネスモデル、パートナーシップなど、IP 5Gのあらゆる機会を捉えて収益化するために、リアルタイムのビリングとポリシー制御機能を必要としています。多様なパートナーの管理が複雑化する中、相互接続、ホールセール、OTT/コンテンツプレーヤー、ディストリビューター、相互接続、MVNO、代理店などのパートナーを効率的に管理することなどが課題となっています。

- さらに、デジタル経済が消費を加速させる中、従来のビリングシステムでは、オンデマンド設計やカスタマイズの不足に対応することしかできません。新世代のビリングシステムでは、柔軟なビジネス・ルール・エンジンを通じて、サービスや製品に関してアジャイル原則に基づいて構築します。ビジネス・スクリプトは、CSPが市場投入までの時間(TTM)を数ヶ月から数時間に短縮するのに役立ちます。

- 最近、COVID-19パンデミックが発生したため、会社の方針が在宅勤務にシフトしました。このような在宅勤務により、通信タワーのデータ消費量が増加しました。例えば、インドの通信事業者2社は、5月末までの68日間にわたる全国的な封鎖による景気減速をものともせず、料金の伸びとデータ使用量の増加により、6月までの3ヵ月間(2021年度第1四半期)に大幅な売上高とEBITDA(金利・税金・減価償却前利益)の伸びを報告しました。携帯電話を通じて自宅でインターネットを利用するデバイスが増加した結果、データ使用量が増加しました。これにより、通信料金請求と収益管理の需要が増加しました。

テレコムビリング・収益管理市場の動向

携帯電話事業者が市場シェアの大半を占める

- スマートフォンユーザーの急増は、数多くのモバイルアプリケーションと相まって、加入者のかつてない増加を可能にしました。例えば、シスコシステムズによると、2022年現在、世界のスマートフォンユーザーは約57億人に上ります。その結果、モバイル・ネットワーク・プロバイダーの容量に対する需要が大きくなっています。

- モバイル事業者は、5G、Volte、Vowifiなどの新技術を導入し、ネットワーク容量を追加することで、この需要を活用しています。明らかに、OSSとBSSのキャリアクラスのビリングソリューションもこのペースに追いつく必要があり、数百万件の同時トランザクションをサポートすることが求められています。

- 欧州では、通信料金請求のための収益管理システムの市場が拡大すると思われます。5G接続を推進する政府の取り組みが拡大し、市場の主要企業がこの分野に浸透しつつあることが、市場開拓の要因と考えられます。また、モバイル利用者の増加や通信サービス企業の新サービス追加に伴い、効率的な請求書発行や収益管理システム・サービスへの需要が高まっています。

- また、ネットワーク機能、サービス、その他の顧客体験管理強化の革新に牽引され、世界的に通信業界の競合情勢が激化しているため、携帯電話事業者は、強固な収益分配モデルに裏打ちされた新製品や新サービスの立ち上げを加速させる戦略に注力できるようになっています。テレコムビリング・収益管理などのソリューションを活用することで、事業者はビリング精度の維持やエンド・ツー・エンドの紛争管理による顧客体験の向上など、ビジネス・プロセスを自動化することができます。

- さらに、このソリューションによって、利害関係者のレベニューシェアの管理に伴う不正を排除することで、携帯電話事業者はコストを削減することも可能になります。例えば、CFCA(Communications Fraud Control Association)によると、世界の携帯電話事業者は、不正行為や未回収の収入により、年間約380億米ドルの損失を被っています。

北米が大きなシェアを占める

- 北米は通信産業が著しく成熟しているため、大きな市場シェアを占めると予想されます。例えば、米国の大手携帯通信事業者が5Gの商用サービスを数回開始したことで、同地域では5Gのカバレッジが顕著になっています。実際、GSMAの調査では、北米における5Gの普及率は2025年までに46%、すなわち200の5G接続に上昇すると推定しています。

- この調査ではさらに、北米のユニーク・モバイル加入者数は約3億2,100万人で、人口の83%に相当することが明らかになっています。さらに、2025年には3億4,500万人、すなわち人口の85%に達すると予測されています。

- また、米国は世界で最も技術導入が進んでいる国のひとつです。同国は画期的な新興企業で有名です。この高いシェアは、最先端技術の採用と通信業界の需要増によるところが大きいです。IoT、5G、アナリティクス、クラウドといった最先端技術の採用により、米国はテレコムビリング・収益管理市場でも収益面で優位を占めています。

- 加入者数の増加に加え、さまざまなモバイルサービスに対する消費者の支出が高いことや、Amdocs、Oracle、CSG International、HPEなど、この地域の著名なプレーヤーが数社存在していることが、市場の成長を後押ししています。さらに、同地域の通信業界は確立されており、通信製品やサービスの普及率も高いです。同地域の通信セクターは膨大な量のデータを生産しており、それが通信ビリングと収益管理の需要を高めています。

- さらに、COVID-19以後、この地域がロックダウン状態から抜け出した状況、新しい働き方の背景、この地域で支配的な世界化電気通信モデルの潜在的なシフトにより、サービスの自動化速度が加速しました。これらのサービスには、ビリングや収益管理が含まれます。この事例により、今後市場の成長がさらに加速すると予想されます。

テレコムビリング・収益管理産業の概要

テレコムビリング・収益管理市場は、現在多くのプレーヤーで構成されているため、非常に競争が激しく、細分化に向かっています。世界のテレコムビリング・収益管理市場の主要企業数社は、製品の進歩をもたらすために絶え間ない努力をしています。著名な企業数社は提携を結び、市場開拓地域に拠点を広げて市場での地位を固めようとしています。主な企業は、エリクソン、ファーウェイ・テクノロジーズ、SAP SE、オラクルなどです。

- 2023年1月- エリクソンとOoredoo Kuwaitが提携し、両社のネットワークにエリクソンビリングを導入。ビリングシステムのアップデートにより、5G製品の競合マーケティングプランが策定され、同時にOoredoo Kuwaitのネットワーク全体で5Gの進化が可能になった。

- 2023年1月- 日本電気株式会社は、NTTドコモにビリング情報を高性能に処理するためのチャージングゲートウェイ機能(CGF)を提供。CGFは、5GCから送信される多様なビリング情報を整理し、BSSに接続することで、新サービスの迅速な開始、提供、収益化をサポートします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 携帯電話加入者数の増加

- テレコムエコシステムにおける収益分配の複雑化

- 市場抑制要因

- 厳しい通信規制の存在

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- タイプ別

- ソフトウェア

- サービス

- 事業者別

- モバイル事業者

- インターネットサービスプロバイダー

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- NetCracker Technology Corporation

- CSG Systems International Inc.

- Oracle Corporation

- Ericsson

- Huawei Technologies

- SAP Se

- Nokia

- Comarch SA

- Optiva, Inc.

- Enghouse Networks

- Sterlite Technologies Limited

- Intracom Telecom SA

第7章 投資分析

第8章 市場機会と今後の動向

The Telecom Billing Revenue Management Market size is estimated at USD 15.55 billion in 2025, and is expected to reach USD 24.40 billion by 2030, at a CAGR of 9.43% during the forecast period (2025-2030).

Communication Service Providers (CSP) worldwide are experiencing increased subscribers, causing significant issues, including network congestion and call drops. To curb these issues, users have started to demand that CSPs deploy efficient and effective billing and revenue management systems.

Key Highlights

- The process of managing telecom billing and revenue includes the management of debt collection as well as communication services. The procedure involves calculating billing and charging information, managing the customer's payments and invoices, and providing information on data utilization. By optimizing the telecom networks, these solutions are frequently employed by telecommunication and digital service providers to increase operational efficiency.

- In the last decade, the global telecom market has changed dramatically, from the rise of cloud-native businesses that interact with customers via the Internet to the rapid migration of content, applications, and services to the cloud. CSP providers have spent billions upgrading their networks to meet the demand. However, many CSPs continue to operate with traditional business support systems that need more modern revenue management capabilities. Therefore, many CSPs worldwide are adopting current billing and revenue management systems.

- Telecom billing and revenue management platform solutions enable telecom service providers to launch the latest services in the market and help leverage their customer relationships. and develop a sense of harmony between the service providers and end-users. Also, the emergence of software-as-a-service (SaaS) platforms further leverages market growth.

- Vendors in the telecom industry use these software solutions to help detect and manage anomalies in the spectrum and eventually decrease operational costs. Also, these tech-enabled programs further assist the CSPs in increasing their revenue by rectifying problems and deploying new measures to optimize network service and visibility.

- Further, in the current market scenario, CSPs require real-time billing and policy control capabilities to help seize and monetize all IP 5G opportunities, including new use cases, devices, business models, and partnerships. With the growing complexity of managing diverse partners, challenges such as efficiently managing partners, including interconnect, wholesale, OTT/content players, distributors, interconnect, MVNOs, and agents, among others.

- Additionally, with the digital economy accelerating consumption, traditional billing systems can only keep up with a lack of on-demand design or customization. With the new generation of billing systems, build on agile principles in terms of services and products through a flexible business rule engine. The business script helps CSP reduce the time-to-market (TTM) from months to hours. thereby driving demand among the end-users.

- The recent outbreak of the COVID-19 pandemic resulted in a shift in company policies towards work-from-home policies. This remote work from home increased the data consumption of the telecom towers. For instance, two Indian telecom operators reported substantial revenue and earnings before interest, taxes, depreciation, and amortization (EBITDA) growth in the three months ending June (Q1 FY2021) due to tariff growth and higher data usage, defying the economic slowdown from the countrywide lockdown of 68 days up to May-end. The increasing number of devices using the Internet for work from home through mobile phones resulted in an increase in data usage. This increased the demand for telecom billing and revenue management.

Telecom Billing and Revenue Management Market Trends

Mobile Operators to Account Major Market Share

- The proliferation of smartphone users, coupled with numerous mobile applications, has enabled unprecedented growth in subscribers. For instance, According to Cisco Systems, as of 2022, there were around 5.7 billion smartphone users worldwide. This has resulted in significant demand for the capacity of mobile network providers.

- The mobile operators leverage the demand by deploying new technologies such as 5G, Volte, and Vowifi and adding networking capacities. Evidently, the OSS and BSS carrier-class billing solutions also need to keep up the pace and are required to support millions of simultaneous transactions.

- The market for revenue management systems for telecom invoicing in Europe will increase. Government efforts to promote 5G connectivity are expanding, and key market players are becoming more prevalent in the area, which can be attributed to the market's development. Additionally, the demand for efficient invoicing and revenue management systems and services is growing as mobile users grow and telecom service companies continuously add new services to their portfolios.

- Also, owing to the increase in the competitive landscape of the telecom industry worldwide, led by innovations in network capabilities, service, and other customer experience management enhancements, mobile operators are able to focus on strategies to help accelerate new product and service launches backed by a robust revenue-sharing model. By leveraging solutions such as telecom billing revenue management, operators can automate the business process, such as maintaining billing accuracy and improving customer experience by managing end-to-end disputes.

- Additionally, the solution would also enable mobile operators to save costs by eliminating the fraud associated with managing the stakeholders' revenue shares. For instance, according to the Communications Fraud Control Association (CFCA), mobile operators worldwide lose around USD 38 billion annually due to fraud and uncollected revenues.

North America to Hold Major Share

- North America is expected to hold a significant market share due to its significantly mature telecom industry. For instance, following several commercial 5G launches by major US mobile operators, the region now has prominent 5G coverage. In fact, a GSMA study estimates that 5G adoption in North America will rise to 46% by 2025, i.e., 200 5G connections.

- The study further reveals that around 321 million unique mobile subscribers in North America represent 83% of the population. Additionally, by 2025, the number is forecast to reach 345 million, i.e., 85% of the population.

- Additionally, the United States is among the nations with the highest levels of technological adoption worldwide. The nation is renowned for its ground-breaking startups. This high share is mostly due to the market's adoption of cutting-edge technology and the increased demand from the telecom industry. Due to the adoption of cutting-edge technologies like IoT, 5G, analytics, and cloud, the U.S. also dominated the telecom billing and revenue management market in terms of revenue.

- The increasing number of subscribers, coupled with high consumer spending on various mobile services and the presence of a few of the prominent players in the region, including Amdocs, Oracle, CSG International, and HPE, among others, is set to leverage market growth. Additionally, the region's communication industry is well-established and has a high penetration of telecom products and services. The region's telecom sector produces a vast amount of data, which in turn is increasing demand for telecom billing and revenue management.

- Additionally, the post-COVID-19 situation as the region emerged from lockdown, the backdrop of new ways of working, and potential shifts in the dominant globalization telecom model in the region enabled an acceleration in the rate of automation of services. These services include billing and revenue management. This instance is expected to further leverage the market's growth going forward.

Telecom Billing and Revenue Management Industry Overview

The telecom billing revenue management market is very competitive and moving towards fragmentation as it currently consists of many players. Several key players in the global telecom billing revenue management market are making constant efforts to bring product advancements. A few prominent companies are entering into collaborations and are also expanding their footprints in developing regions to consolidate their positions in the market. The major players are Ericsson, Huawei Technologies, SAP SE, and Oracle Corp., among others.

- January 2023 - Ericsson and Ooredoo Kuwait teamed up to roll out Ericsson billing across their networks. The billing system update helped create competitive marketing plans for 5G products while also enabling 5G evolution across Ooredoo Kuwait's network.

- January 2023 - NEC Corporation gave NTT DOCOMO a charging gateway function (CGF) for the high-performance processing of billing information. The CGF supports new services' quick start, provision, and monetization by organizing the diverse range of billing information sent from 5GC and connecting to the BSS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Cellular or Mobile Subscribers

- 4.2.2 Growing Complexities in Revenue Sharing Across the Telecom Ecosystem

- 4.3 Market Restraints

- 4.3.1 Presence of Stringent Telecom Regulations

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Assessment of COVID-19 Impact on the Industry

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Type

- 5.2.1 Software

- 5.2.2 Service

- 5.3 By Operator

- 5.3.1 Mobile Operator

- 5.3.2 Internet Service Provider

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 US

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.5 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 NetCracker Technology Corporation

- 6.1.2 CSG Systems International Inc.

- 6.1.3 Oracle Corporation

- 6.1.4 Ericsson

- 6.1.5 Huawei Technologies

- 6.1.6 SAP Se

- 6.1.7 Nokia

- 6.1.8 Comarch SA

- 6.1.9 Optiva, Inc.

- 6.1.10 Enghouse Networks

- 6.1.11 Sterlite Technologies Limited

- 6.1.12 Intracom Telecom SA