|

市場調査レポート

商品コード

1852204

分子育種:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Molecular Breeding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 分子育種:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月09日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

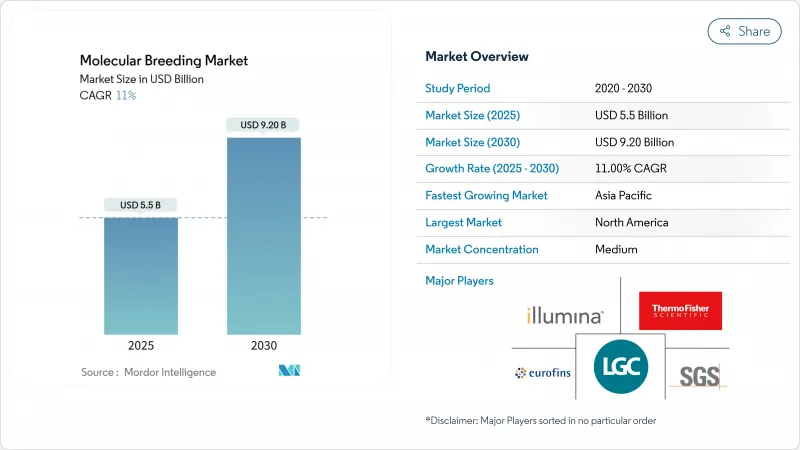

分子育種市場は2025年に55億米ドルを達成し、2030年には92億米ドルに達すると予測され、CAGRは11.0%を記録します。

ゲノム選別に人工知能を取り入れることで、育種サイクルが数年から数ヶ月に短縮され、製品開発効率が向上しています。米国の適応作物・土壌ビジョンやインドの食料安全保障に関する国家行動計画などの政府の取り組みが、気候変動に強い作物品種の需要を促進しています。市場の拡大は、ハイスループットの表現型決定、シーケンスコストの削減、および利用しやすい遺伝子型決定サービスによって促進されます。北米は研究インフラにおいて優位性を維持しているが、アジア太平洋地域は規制改革と食糧安全保障の要件により大幅な成長の可能性を示しています。

世界の分子育種市場の動向と洞察

バイオテクノロジー研究開発資金の拡大

同市場における民間および公的支出は急速に増加しています。サーモ・フィッシャーは2023年に研究開発に13億米ドルを投資し、次世代シーケンサーと試薬のイノベーションを進め、中堅育種業者の参入コストを削減しました。米国農務省のデータ標準化プログラムは、ゲノムデータセットを調和させ、冗長な試験を防ぎ、市場投入までの時間を短縮しています。このような設備投資により、中小企業のコンプライアンス上の障壁が減少し、新規形質開発者が規制要件を回避できるようになりました。さらに、CGIARの4億米ドルの栄養に焦点を当てたポートフォリオのような多国間イニシアティブは、ドナー資金を集め、バイオフォート化の成果を加速させています。

高収量で気候変動に強い作物への需要の高まり

インドでは、記録的な高温に耐える100日小麦品種が発表され、熱や干ばつに強い遺伝子型が試験的規模から商業規模に移行しています。日本の研究センターは、気候変動の影響を受けやすい国々で生産レベルを維持するため、塩分や水ストレス条件に適応したキヌアや大豆の品種を開発しています。植物育種の優先課題は、今や収量の最適化だけでなく、マルチストレス耐性にまで広がっており、生産性と環境回復力を統合する多重化分子マーカーの使用が必要となっています。現在、異常気象は1シーズン当たり数十億米ドルに相当する作物損失を引き起こしており、気候変動に強い種子ポートフォリオの投資収益率を高めているため、財政的な意味合いも大きいです。

厳しく動きの遅い規制当局の承認

新規形質1つあたりのコンプライアンス・コストは1,500万米ドルに達することもあり、開発予算全体の約半分を消費し、小規模なイノベーターの足かせとなっています。遺伝子組換え作物に対するEUの遺伝子組換え法規制により、企業は米国やブラジルのような有利な規制のある市場に注力するようになります。アルゼンチン、ウルグアイ、タイは2024年に規制を更新し、承認を簡素化したが、規制の不確実性は引き続きタイムラインを延長し、資金調達コストを増加させる。

セグメント分析

植物への応用は2024年の分子育種市場の63%を占め、これは主にトウモロコシ、小麦、大豆の育種プログラムにおけるゲノム選抜の実施によるものです。畜産分野はCAGR13.1%で成長を遂げており、乳牛における従来の推定と比較して優れた性能を示すゲノム育種値や、CRISPRベースの耐病性豚の開発がその原動力となっています。Angus SteerSELECTのようなツールは、重要な枝肉形質について0.72を超える予測精度を実証し、肥育場の収益性を高め、投資を集めています。

家禽部門では、世代間隔を短縮するために、繁殖力と成長遺伝子の精密編集を実施しています。さらに、豚の育種におけるメタボロームとゲノムの統合モデルは、現在の成果は控えめであるにもかかわらず、平均日増体量を改善する可能性を示しています。これらの市場開拓は、畜産分野が2030年までに分子育種市場への寄与を大幅に高める可能性があることを示しています。

一塩基多型(SNPs)は2024年の分子育種市場規模の42%を占め、ハイスループットプラットフォームとの互換性とゲノムワイド関連出力の強化により13.2%のCAGRを維持しています。単価の低下により、以前は単純配列反復配列が持っていた価格的優位性が失われ、発展途上国のプログラムがSNPソリューションを直接採用するようになっています。RNA-seqおよびATAC-seqデータから機能変異パネルを導入することで、酪農タンパク質形質における育種精度が3ポイント向上し、この技術の信頼性が実証されました。

SNPワークフローの標準化により、発現配列タグやその他の従来のマーカーは、主に発現プロファイリングなどの特殊なアプリケーションに位置づけられるようになりました。SNPの採用が増えることで、データの相互運用性が向上し、これはAIを活用した育種システムの開発にとって基本的なことです。

地域分析

北米は2024年の分子育種市場シェアの36%を占め、先進的な研究インフラと効率的な規制の枠組みによって支えられています。イルミナは、2024年に43億3,000万米ドルの売上を計上し、LGC Biosearch Technologiesと提携し、連作作物および家畜分野向けのターゲットジェノタイピングーバイーシーケンス機能を強化しています。米国農務省のSECUREルールは遺伝子編集製品の承認プロセスを合理化し、この地域の市場リーダーシップを維持しています。

アジア太平洋は2030年までのCAGRが12.1%と予測され、最も高い成長の可能性を示しています。中国は2024年に耐病性遺伝子編集小麦を承認し、インドの規制更新は特定のゲノム編集の承認を合理化し、民間育種イニシアチブを加速させる。日本は段階的な規制制度と作物ストレス研究に重点を置いているため、この地域の重要なハブとしての地位を確立しています。政府資金と民間ベンチャー資本の組み合わせにより、食糧安全保障のニーズに対応するためのこの地域の育種インフラが強化されつつあります。

欧州は、規制上の制約にもかかわらず、市場での大きな存在感を維持しています。EU環境委員会が2024年後半に新しいゲノム技術に関する法律を承認したことは、リスク・ベースの評価に向けた動きを示しています。英国では精密育種法が施行され、遺伝子編集作物の試験を迅速化するための2段階の安全性審査システムが確立されました。スイスも同様の規制改革を実施しています。市場開拓は政策展開次第であり、欧州のグリーン・ディール持続可能性要件を満たす品種に対する需要が大きいです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- バイオテクノロジー研究開発資金の拡大

- 高収量で気候変動に強い作物への需要の高まり

- 精密育種とフェノタイピング・プラットフォームの急速な普及

- 政府が支援する食糧安全保障への取り組み

- AIとゲノム選別の融合

- 低投入栽培品種に対する炭素クレジット・インセンティブ

- 市場抑制要因

- 厳しく、遅々として進まない規制当局の承認

- シーケンスとジェノタイピング・インフラの資本コストが高め

- 相互運用可能なデータ・プラットフォームへの限られたブリーダーのアクセス

- 分子改変」種子をめぐる社会的懸念

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 植物

- 畜産

- その他の用途

- マーカータイプ別

- 単純配列反復(SSR)

- 一塩基多型(SNP)

- 発現配列タグ(EST)

- その他のマーカー

- 育種プロセス別

- マーカー支援選抜(MAS)

- 量的形質遺伝子(QTL)マッピング

- マーカーアシストバッククロッシング

- ゲノムセレクション

- ターゲット特性別

- 収量増加

- 病害虫抵抗性

- 生物ストレス耐性

- 品質と栄養特性

- エンドユーザー別

- 種子・作物保護企業

- 畜産会社

- 学術・政府研究機関

- 独立ブリーディング・サービス・プロバイダー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- LGC Limited(Cinven)

- Eurofins Scientific

- SGS SA

- Agilent Technologies, Inc.

- DanBred P/S

- LemnaTec GmbH(Nynomic AG)

- Charles River Laboratories

- Intertek Group plc

- KeyGene NV

- Syngenta AG

- Corteva Agriscience

- Bayer AG

- BASF SE

- Sequentia Biotech SL

- Hudson Alpha