プレッシャーラベル:市場シェア分析、産業動向と統計、成長予測(2025~2030年)

Pressure Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642185

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

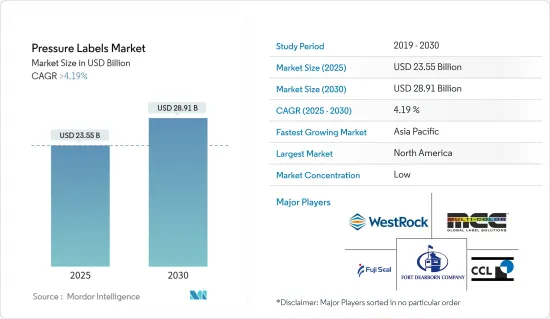

プレッシャーラベル市場規模は2025年に235億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.19%を超え、2030年には289億1,000万米ドルに達すると予測されます。

製薬業界の成長は、多様な分野におけるその広大な応用範囲と相まって、プレッシャーラベル市場の主要な促進要因となっています。プレッシャーラベル製品における最新の技術革新と需要の高まりが、市場の成長を後押しすると予想されます。

主なハイライト

- 世界で最も普及しているラベル技術は、引き続き感圧ラベルです。感圧ラベルは食品事業で幅広く使用されています。その用途は飲食品業界にとどまらず、医薬品、消費財、パーソナルケア、建設業など他の分野にも広がっています。

- 用途に応じて、さまざまな接着剤が感圧ラベルを永久的または再剥離可能にすることができます。さらに、ヘビーデューティー用途の感圧シーラントは、極端な温度変化にも耐えられます。自動車用品、クリーニング製品、アルコール、ワイン、スピリッツ、飲食品など、さまざまなエンドユーザーの用途に適しています。

- さらに、消費者の持続可能性への意識の高まりに伴い、PSラベルの表面在庫はリサイクル可能な材料で構成されています。さらに、技術的なブレークスルーを通じて、多くの企業がリサイクルを妨げない独自の接着剤を開発しました。感圧ラベルは、このような持続可能な技術の支援により、業界リーダーとしての地位を強化すると予想されます。

- さらに、感圧ラベルメーカーの一部は、PE、PP、PET、PVCポリマーフィルム素材を使用して、製品にさらなる機能性を持たせています。これには、強度、耐湿性、色、表面の滑らかさ、透明性、高光沢、耐久性、機械的耐性などが含まれます。感圧ラベルが提供する重要な動向には、持続可能性、堅牢性、RFID、偽造防止ラベルの増加、フェイスストックとしての剥離・再貼付可能フィルムなどがあります。

- 飲食品およびヘルスケアセクターは、COVID-19シナリオにもかかわらず、より有望な成長を示しました。これらの分野のサプライヤーは、消費者やヘルスケアに不可欠なラベル素材の継続的な生産と提供に積極的に取り組んでいます。しかし、販売と生産が停止しているため、ほとんどの業者の損失は悪化しています。競合の増加や印刷・加飾技術の開発とともに、原材料の価格も上昇しています。さらに、ロシアとウクライナの戦争もパッケージングのエコシステム全体に影響を与えています。

プレッシャーラベル市場動向

飲料エンドユーザーセグメントがプレッシャーラベルの成長を牽引する見込み

- パッケージ製品やブランド製品に対する需要の高まりと、製品の真正性やその他の側面に関する消費者の知識の高まりにより、飲料エンドユーザーカテゴリーが予測期間中に最も速い成長を遂げると予想されています。

- 飲料ラベルは様々な状況で容器に密着する必要があるため、感圧ラベルは不可欠です。アプリケーションの環境が室温であろうと、20Fから40Fのようなもっと難しい環境であろうと、飲料ラベル用の粘着デザインは素早く貼り付き、必要に応じて定位置に留まる必要があります。寒さ、湿気、継続的な製品の取り扱いにもかかわらず、ラベルと粘着剤は適切な耐久性を維持する必要があります。

- ポーランド中央統計局によると、ポーランドのビール生産量は2023年に約3,520万ヘクトリットルに達します。飲料パッケージング分野の拡大により、感圧ラベルのニーズは今後数年で高まると思われます。

- 感圧ラベルの需要を牽引するものとして、偽造防止ラベルの拡大が予想されます。模倣を阻止し、食事の真正性を確認するため、これは食品事業にとって特に重要です。偽造防止対策はまた、偽造によってもたらされる収益や顧客ロイヤリティの損失を削減する上でもビジネスを支援します。プレッシャーラベルは主に食品や医薬品のラベルに使用され、RFIDやバーコードによる追跡で偽造を減少させる。

- ラベルサプライヤーは、飲料メーカーが持続可能性に関連したパッケージング目標を達成するのを支援するラベル商品を作成・提供することで、持続可能性の動向に対応しています。リサイクルシステムでは、リサイクル可能でPET容器から簡単に剥がせる感圧ラベルが、PET容器に使用されるラベルの新しい進歩です。例えば、Hammer Packaging Inc.は、持続可能性のイニシアチブを推進するために、基材メーカーと緊密に協力しています。感圧ラベル事業では、独創的なソリューションの開発も行っています。

- 米国蒸留酒協会(DISCUS)によると、蒸留酒カテゴリーのサプライヤー総収入のうち、33%と最も高い割合を占めるのは高級蒸留酒です。バリュー・スピリッツは同年、最も急速に売上総利益を伸ばしました。バリュー・スピリッツは前年比8%増、プレミアム・スピリッツは3.8%増でした。

- サプライヤー総収入の中でプレミアムスピリッツが最も多いという事実は、高級品や高級品に対する消費者の需要が高まっていることを示唆しています。このパターンは、消費者が高級品やサービスにより多くのお金を出す用意があることを示唆しています。その結果、プレッシャーラベル市場は、高価なスピリッツの知覚価値と美的魅力を高めるプレミアム・ラベル・オプションを提供することで、このニーズを満たすことができます。その例としては、特殊な仕上げ、エンボス加工、箔押し、エレガンスと高級感を醸し出す特徴的なラベル素材などが挙げられます。

北米が市場成長を記録する見込み

- 米国では、感圧ラベルの情報収集と伝達に電波を使用するRFIDの採用がより重要になった。食品、飲料、医薬品は、監視、認証、偽造防止のために技術統合されたエンドユーザー分野です。

- Mohawkは、この新しい製品ラインの一部として、UPM Raflatac Americasとの戦略的関係を宣言します。Mohawk Renewal HempとStrawの表面紙は、ロール給紙による感圧ラベリングソリューションを提供できます。

- パートナーシップもまた、この地域の市場需要を牽引しています。例えば、Mark AndyとUPM Raflatacは最近、北米の感圧ラベル業界で戦略的関係を結びました。この提携により、両社はフレキソ印刷とデジタル印刷の両方で環境に優しい印刷ソリューションを開発できるようになるはずです。

- PSLの需要は、その適応性の高さから高まっています。このため、業界各社は能力の向上を余儀なくされており、市場の高まる需要に対応できるようになっています。その一例として、UPM Raflatacは2022年12月に米国ワシントン州バンクーバーに新ターミナルを開設する意向を表明しました。この新拠点は、UPM Raflatacのスリッティングと流通能力を拡大し、同社の北米ターミナル・ネットワークをサポートします。顧客の成功をサポートし、感圧ラベルの需要増加に対応するため、UPMラフラタックは一貫して事業強化のための投資を行っています。

プレッシャーラベル業界の概要

プレッシャーラベル市場は、Multi-color Corporation、CCL Industries Inc、Westrock Company、Fuji Seal International Incなどの中小企業がシェアを占めており、非常に断片化されています。また、このため市場競争も激しいです。市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年4月- 世界最大のラベル企業の1つであるマルチカラー・コーポレーション(MCC)は、インモールドラベル(IML)ソリューションの主要企業の1つであるトルコを拠点とするコルシニ社の買収を発表しました。IMLは、容器の製造工程であらかじめ印刷されたラベルを包装用金型に挿入する高成長のラベリング技術で、完全にリサイクル可能で、コスト効率が高く、耐久性があり、一貫性のある製品を作ることができます。

- 2023年6月-CCLインダストリーズは、スイスに本社を置くCapri-Sun Groupが所有するPouch Partners AG(スイス)からPouch Partners s.r.l.(イタリア)を買収する契約を締結したと発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- 市場促進要因

- デジタル印刷技術の進化

- 市場抑制要因

- 過酷な気候条件に耐える製品の不足

第5章 COVID-19が市場に与える影響

第6章 市場セグメンテーション

- 印刷プロセス別

- グラビア

- フレキソ印刷

- スクリーン

- 凸版印刷

- インクジェット

- その他のプロセス(オフセット・リソグラフィー、電子写真法)

- エンドユーザー産業別

- 食品

- 飲料

- ヘルスケア

- 化粧品

- 家庭用

- 産業(自動車、工業用化学品、耐久消費財・非耐久消費財)

- 物流

- その他エンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Fort Dearborn Company

- Multicolor Corporation

- CCL Industries Inc

- Westrock Company

- Fuji Seal International Inc.

- Taylor Corporation

- Huhtamaki Group

- Taghleef Industries Inc(Al Ghurair Group)

- Coveris

- Avery Dennison Corp

- UPM Raflatac, Inc

- Inland Printing Co. Ltd

- Constantia Flexibles Group GmbH

- Folienprint RAKO GmbH

- Herma GmbH

- Skanem AS

第8章 投資分析

第9章 市場の将来

目次

The Pressure Labels Market size is estimated at USD 23.55 billion in 2025, and is expected to reach USD 28.91 billion by 2030, at a CAGR of greater than 4.19% during the forecast period (2025-2030).

Growth in the pharmaceutical industry, coupled with its vast application scope in diverse sectors, is the major driver for the pressure labels market. The latest innovations in pressure label products and rising demand is expected to fuel the market growth.

Key Highlights

- The most popular label technology worldwide will continue to be pressure-sensitive labels. They are used extensively in the food business. Their uses extend beyond the food and beverage industry, including the pharmaceutical, consumer goods, personal care, and other sectors, including construction.

- Depending on the application, different adhesives can make pressure-sensitive labels permanent or releasable. Furthermore, temperature extremes would not harm pressure-sensitive sealants for heavy-duty applications. They are appropriate for applications across a range of end-users, including automotive items, cleaning products, alcohol, wine, spirits, food, and beverage, because they can handle the weights of thick labels, such as expanded content labels.

- Additionally, in keeping with consumers' increased awareness of sustainability, the face stock of PS Labels is comprised of recyclable materials. Furthermore, through technical breakthroughs, numerous businesses created unique adhesives that do not obstruct recycling. Pressure Sensitive labels are anticipated to strengthen their position as industry leaders with the aid of sustainable technologies like these.

- Additionally, a growing portion of pressure-sensitive label makers uses PE, PP, PET, and PVC polymer film materials to provide their products with additional functionality. It includes strength, moisture resistance, color, smoothness on the surface, transparency, high gloss, durability, and mechanical resistance. Important trends offered by pressure-sensitive labels include sustainability, robustness, RFID, a rise in anti-counterfeit labels, and detachable and repositionable films as face stock.

- The food, beverage, and healthcare sectors showed more encouraging growth despite the COVID-19 scenario. The suppliers to these sectors are actively engaged in the ongoing production and provision of label materials for essential consumer and healthcare products. However, with sales and production on hold, most merchants' losses are worsening. Along with increased competition and developing printing and decorating technologies, the price of raw materials is also rising. Further, the Russia-Ukraine war also impacts the overall packaging ecosystem.

Pressure Labels Market Trends

Beverage End-User Segment is Expected to Drive Growth of Pressure Labels

- With the rising demand for packaged and branded products and rising consumer knowledge of the authenticity and other aspects of the product, the beverage end-user category is anticipated to see the fastest growth over the projection period.

- Because beverage labels must stick to the container in various situations, pressure-sensitive labeling is essential. Whether the application environment is room temperature or something more difficult, like 20F to 40F, an adhesive design for beverage labeling should stick rapidly and stay in place as needed. Despite cold, dampness, and continuous product handling, the label and adhesive must maintain the appropriate durability.

- According to the Central Statistical Office of Poland, the volume of beer produced in Poland amounted to approximately 35.2 million hectolitres in 2023. The need for pressure-sensitive labels will rise in the upcoming years due to the expanding beverage packaging sector.

- One driving demand for Pressure Labels is anticipated to be the expansion of Anti-Counterfeit Labels. As it discourages copying and verifies the meal's authenticity, this is particularly crucial for the food business. Anti-counterfeiting measures also assist businesses in reducing revenue and customer loyalty losses brought on by counterfeiting. Pressure labels are mostly used to label food and pharmaceutical products to decrease counterfeiting using RFID or barcode tracking.

- Label suppliers are responding to sustainability trends by creating and providing label goods to assist beverage manufacturers in achieving their sustainability-related packaging goals. In recycling systems, pressure-sensitive labels that are recyclable and effortlessly removed from PET containers are new advances for labels used on PET containers. For instance, Hammer Packaging Inc. collaborates closely with substrate producers to promote sustainability initiatives. For its pressure-sensitive label business, it includes developing creative solutions.

- The highest percentage of supplier gross income in the spirits category, 33%, belongs to high-end spirits, according to the Distilled Spirits Council of the United States (DISCUS). Value spirits saw the fastest increase in gross income during that same year. Value spirits had an increase of 8% over the prior year, while premium spirits saw an increase of 3.8%.

- The fact that premium spirits comprised the greatest portion of supplier gross income suggests increased consumer demand for high-end and upscale goods. This pattern implies consumers are prepared to shell out more money for premium goods and services. Consequently, the Pressure Labels Market can satisfy this need by offering premium labeling options that raise expensive spirits' perceived value and aesthetic appeal. Some examples might include specialized finishing, embossing, foil stamping, or distinctive label materials that exude elegance and exclusivity.

North America is Expected to Register Market Growth

- The incorporation of radio-frequency identification, which employs radio waves to gather and communicate information in pressure-sensitive labels, became more important in the United States. Food, drinks, and medicines are only end-user verticals with technological integration for monitoring, authentication, and anti-counterfeiting items.

- Mohawk declares a strategic relationship with UPM Raflatac Americas as a part of this new product line. Mohawk Renewal Hemp and Straw paper face stocks can provide roll-fed, pressure-sensitive labeling solutions.

- Partnerships are also driving the market demand in the region. For instance, Mark Andy and UPM Raflatac recently formed a strategic relationship in the North American pressure-sensitive label industry. This collaboration should enable these players to create printing solutions that are both flexographic and digital converters friendly to the environment.

- The demand for PSLs is rising as a result of their adaptability. The industry's operators are compelled by this to increase their capabilities, allowing them to meet the escalating demand of the market. As an illustration, UPM Raflatac declared intentions to open a brand-new terminal in Vancouver, Washington, in the United States, in December 2022. The new location will expand UPM Raflatac's slitting and distribution capabilities while supporting the company's North American terminal network. To support the success of its clients and meet the increasing demand for pressure-sensitive labels, UPM Raflatac consistently invests in operational enhancements.

Pressure Labels Industry Overview

The Pressure Labels Market is highly fragmented as several small and medium-sized players, such as Multi-color Corporation, CCL Industries Inc, Westrock Company, and Fuji Seal International Inc, contain a share in the market. Also, this makes the market extremely competitive too. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- April 2023 - Multi-Color Corporation (MCC), one of the largest label companies in the world, has announced the acquisition of Turkiye-based Korsini, one of the leading providers of in-mold label (IML) solutions. IML is a high-growth labeling technology in which pre-printed labels are inserted into a packaging mold during a container's manufacturing process, creating a fully recyclable, cost-effective, durable, and consistent product.

- June 2023 - CCL Industries has announced it has signed an agreement to acquire Pouch Partners s.r.l., Italy, from Pouch Partners AG, Switzerland, a company owned by Swiss-headquartered Capri-Sun Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Market Drivers

- 4.4.1 Evolution of Digital Print Technology

- 4.5 Market Restraints

- 4.5.1 Lack of Products with Ability to Withstand Harsh Climatic Conditions

5 Impact of COVID-19 on the Market

6 MARKET SEGMENTATION

- 6.1 By Print Process

- 6.1.1 Gravure

- 6.1.2 Flexography

- 6.1.3 Screen

- 6.1.4 Letterpress

- 6.1.5 Inkjet

- 6.1.6 Other Processes (Offset Lithography, Electrophotography)

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Cosmetics

- 6.2.5 Household

- 6.2.6 Industrial (Automotive, Industrial Chemicals, and Consumer and Non-consumer Durables)

- 6.2.7 Logistics

- 6.2.8 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fort Dearborn Company

- 7.1.2 Multicolor Corporation

- 7.1.3 CCL Industries Inc

- 7.1.4 Westrock Company

- 7.1.5 Fuji Seal International Inc.

- 7.1.6 Taylor Corporation

- 7.1.7 Huhtamaki Group

- 7.1.8 Taghleef Industries Inc (Al Ghurair Group)

- 7.1.9 Coveris

- 7.1.10 Avery Dennison Corp

- 7.1.11 UPM Raflatac, Inc

- 7.1.12 Inland Printing Co. Ltd

- 7.1.13 Constantia Flexibles Group GmbH

- 7.1.14 Folienprint RAKO GmbH

- 7.1.15 Herma GmbH

- 7.1.16 Skanem AS

8 Investment Analysis

9 Future of the Market

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日