|

市場調査レポート

商品コード

1642183

シンクライアント:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Thin Client - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シンクライアント:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

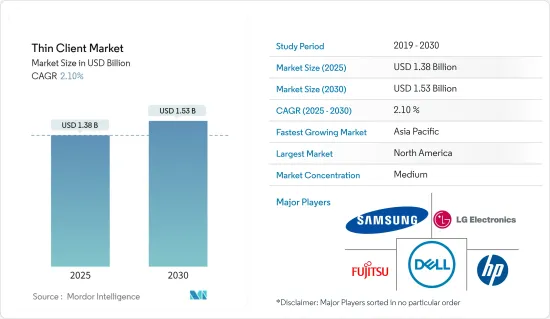

シンクライアント市場規模は2025年に13億8,000万米ドルと推計され、予測期間中(2025-2030年)のCAGRは2.1%で、2030年には15億3,000万米ドルに達すると予測されます。

シンクライアント市場は、主にその利点、すなわちコスト削減とエネルギー消費の削減、集中化と管理の容易さ、さらにこれらのデバイスが提供するインフラセキュリティの向上により、予測期間中に拡大すると予想されます。

主なハイライト

- さまざまな業界が、デスクスペースを大幅に削減し、従来のシステムからの置き換えやアップグレードが容易な、低コストのデバイスを求めています。シンクライアント・システムは、こうした要件を満たします。また、シンクライアント・システムは、一定期間のエネルギー消費量を削減することが可能であり、これが様々な産業で需要が増加している主な理由です。

- ヘルスケア業界でも、セキュリティ上の利点から、コンピューティング・ソリューションとしてデバイスの採用が拡大しています。一方、ITおよび通信業界では、主に仮想ネットワークの開発を促進するためにこれらのデバイスを導入しています。シンクライアント・デバイスを企業やその他の分野に導入することで、ローカル・マシンの設定でユーザーの侵入を制限できるため、セキュリティ関連の利点が向上します。このアプリケーションは、システムをより安全に保護します。

- 大学、研究機関、研究所などのさまざまな教育機関では、IT管理部門でモニターを集中管理し、エネルギー消費を抑えるために、シンクライアント・ソリューションを採用するケースが増えています。これらのデバイスは、システムのアップグレードにかかるコストや、ログインのたびにPCやノートPCをセットアップするのにかかる時間も削減します。

- クラウド・コンピューティングの採用が増加していることも、市場の成長を後押ししています。コストを削減し、コンピューターやサーバーにインストールされていないデータやアプリケーションにアクセスするために、複数の組織がクラウド・コンピューティングを利用しています。クラウドは、動的に拡張可能で仮想的な方法で、コンピューティング・リソースをユーティリティとして迅速に提供できるインフラとして登場しました。世界中の様々な組織がハイブリッドやマルチクラウド環境に移行しています。シンクライアントは、比較的安価で安全なハードウェア・ソリューションとして市場の成長を牽引しています。

- いくつかの企業でワークスペース・アズ・ア・サービス(WaaS)の採用が増加していることから、予測期間中、市場の需要拡大が見込まれます。WaaSは、従業員がリモートからアプリケーションにアクセスできるようにするために、複数の組織で利用されているデスクトップ仮想化です。しかし、新興諸国におけるクラウドコンピューティングのネットワーク問題は、調査対象市場の成長を抑制すると予想されます。

- 地政学的に敏感な業界で事業を展開するエネルギー企業は、特に外国政府からのサイバー攻撃の標的に頻繁に直面しています。しかし、デスクトップ仮想化の基盤としてクラウドを使用することで、機密情報を一元的に保存することができ、認証ポリシーを設定してクラウド環境を保護することができます。このような要因が、シンクライアント市場の需要を生み出すと予想されます。

- ここ数十年、リモートワークの傾向が強まっています。しかし、COVID-19の影響により、ごく短期間のうちにこの傾向は劇的に加速したが、世界中の政府によって呼びかけられた自己隔離対策に迅速に対応することを、規模の大小にかかわらず企業に強いることとなり、この傾向は急速に加速しています。パンデミックの流行により、より多くの人々がリモートで仕事をするようになり、従業員間のデータ共有のセキュリティに関する懸念が高まった。これが、シンクライアント端末の需要導入を後押ししています。

シンクライアント市場動向

ヘルスケア・セグメントが市場の成長を牽引する見込み

- ヘルスケアプロバイダーは、最高水準の患者ケアを提供することに厳格です。彼らは、ケアのあらゆる段階で患者の体験を向上させるために使用するテクノロジーに敏感です。救急治療室への入院からリハビリテーション、外来治療に至るまで、テクノロジーは患者の転帰に大きな影響を与え、医療提供者の生産性と運営コストに決定的な影響を与えます。

- このことは、ヘルスケア領域全体でユビキタスなデスクトップ・コンピューティング・インフラに特に当てはまります。従来のデスクトップPCモデル、データ、アプリケーションは、ネットワーク上に分散された個々のPC上にローカルに存在し、多くの場合、個別に構成・管理されたPCのクラスタが形成されています。これらは機密性の高い患者データと関連しており、パラメータがほとんど統一されていないことがよくあります。

- しかし、シンクライアントの場合、データとアプリケーションはデータセンターやクラウドインフラストラクチャで遠隔管理、保存、集中管理されます。シンクライアントは単なるアクセスポータルであり、管理者や臨床医が資格情報の許す限り、アプリケーションや患者データに即座にアクセスできます。

- シンクライアントはそのアーキテクチャの性質上、様々なセキュリティ上の利点があり、セキュリティ上の脅威にさらされることを最小限に抑えながら、HIPAAやその他のヘルスケア規制へのコンプライアンスを確保することができます。クラウドベースのデータやアプリケーションへの許可されたユーザーのアクセスは、ユーザー認証と権限検証によって厳密に制御されます。USB/ポート保護、スマートカード、ファイアウォールにより、これらのセキュリティ対策はさらに強化されます。

- この業界は現在デジタル化に移行しつつあるが、信頼性の低い技術の失敗は患者の健康に影響を与える問題につながるため、変化に強いということはよく知られています。あらかじめ決められたワークフローからの逸脱は、病院の運営に悪影響を及ぼしかねないです。このような躊躇にもかかわらず、業界は絶えず変化する規制や協定に準拠し続けるために、テクノロジーの導入を加速させなければならないです。

- このようなニーズは、提供能力を最大化することを中心に設計された強固なパートナーシップ構造を後押ししています。例えば、2023年3月、最新のワークスペース向けにセキュアに管理されたエンドポイントのパイオニアであるStratodeskは、複数のLG Business SolutionsシンクライアントがStratodesk NoTouch OSの認定を受けたことを発表し、ITチームにプライベートおよびパブリッククラウド環境の両方でターンキーシステムを展開する自信と柔軟性を提供しました。

北米が主要市場シェアを占める見込み

- 北米が市場を独占すると予想される主な要因は、クラウド技術の採用が増加していることや、活動性と柔軟性を必要とする高度な技術志向の製品などです。同地域では、大半の企業がITサポートを利用できます。市場リーダーの存在、相当数のクラウド・サービス・プロバイダー、ホスティング・サーバーの増加が、この地域における市場成長に不可欠な要因となっています。

- 同地域の組織は新技術をいち早く導入しており、これが同地域の優位性を支える主な原動力となっています。大手クラウドサービスプロバイダーは、この地域におけるクラウドベースのシンクライアント展開の成長に重要な役割を果たしています。

- 放送では、クラウド・コンピューティングと仮想化がますます重要な役割を果たしています。ネットワーク・プロトコルで遠隔操作できる仮想マシンやコンピュータは、現場で物理的に利用可能な機器を最適に補完できる可能性があります。

- 北米のIT・通信業界は、他の地域市場の中でも最大級の規模を誇る。銀行、ヘルスケア、政府機関など、大量の機密情報を扱う業界は、シンクライアント・ソリューションの採用に期待を寄せています。ファット・クライアントよりも知的財産の完全性を保つことができるからです。

- シンクライアント・ソリューションのプロバイダーが国内に数社存在することも、このような強いポジションの背景にあります。特に、HP Inc.とシトリックス社の最近の提携は、安全で効率的なシンクライアント・ソリューションの提供を目指しており、リモートワーク機能の強化と、すべての仮想デスクトップとアプリケーションへのシームレスなアクセスに焦点を当てています。

シンクライアント業界の概要

シンクライアント市場は、多くの大手企業が国内外市場に製品を提供しているため、競争が激しく、複雑化しています。市場の集中は緩やかで、主要企業は製品やサービスの革新、提携、合併、買収などの戦略を採用し、地理的範囲を拡大し、競合他社より優位に立とうとしています。市場の主要プレイヤーには、Dell Inc.、H.P. Development Company LP、Samsung Group、L.G. Electronics Inc.などがいます。

- 2023年11月-AWSは、企業のワークスペースに革命を起こすAmazon WorkSpaces Thin Clientの発売を発表。

- 2023年8月-LG Electronics Inc拡張の簡素化に加え、製品寿命の延長、優れた安全性、高性能、容易な接続性、効率性と生産性を向上させる大幅な省エネを実現するCQと呼ばれるシンクライアント・シリーズを2023年に発売。このシンクライアントは、信頼性の高いパフォーマンス、強力なデータ保護、セキュアな仮想デスクトップ体験を実現し、導入と管理が容易なエンドポイントをヘルスケア施設に提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- ネットワークインフラのセキュリティ強化

- コストとエネルギー消費の削減

- 市場の課題

- クラウドコンピューティングにおける新興諸国のネットワーク問題

第6章 市場セグメンテーション

- タイプ別

- ハードウェア

- ソフトウェアサービス

- エンドユーザー別

- BFSI

- IT・通信

- ヘルスケア

- 政府機関

- その他エンドユーザー(小売、製造、教育)

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Dell Inc.

- HP Development Company LP

- Samsung Group

- LG Electronics Inc.

- NEC Corporation

- Fujitsu Ltd

- Lenovo Group Limited

- Cisco Systems Inc.

- Advantech Co. Ltd

- Siemens AG

- IGEL Technology GmbH

第8章 投資分析

第9章 市場機会と今後の動向

The Thin Client Market size is estimated at USD 1.38 billion in 2025, and is expected to reach USD 1.53 billion by 2030, at a CAGR of 2.1% during the forecast period (2025-2030).

The market for thin clients is expected to increase in the forecast period mainly because of its advantages, i.e. cost savings and reduced energy consumption, centralisation and ease of management as well as increased infrastructure security offered by these devices.

Key Highlights

- Various industries seek low-cost devices that significantly decrease desk space and offer an easy replacement/upgrade for conventional systems. The thin client systems qualify for these requirements. They can also reduce energy consumption over a period, which is the primary reason for the increasing demand for devices across various industries.

- The healthcare industry is also witnessing an extensive adoption of devices as a computing solution, owing to their security benefits. In contrast, the IT and telecom industry is installing these devices primarily to facilitate the development of a virtual network. Implementing thin client devices in enterprises or other areas can provide better security-related advantages, as they limit the user from any intrusion in a local machine setting. This application renders the system more secure and protected.

- Various educational institutions, such as colleges, research institutes, and labs, are increasingly adopting thin client solutions to control the monitors centrally at the IT control department, thereby reducing energy consumption. These devices also decrease the cost of system upgrades and the time consumed in setting up the PC or laptop at each login.

- The increasing growing adoption of cloud computing is also driving market growth. Several organizations use cloud computing to reduce costs and access the data and applications not installed on the computers or servers. Clouds emerged as an infrastructure that may enable the rapid delivery of computing resources as a utility in a dynamically scalable and virtual manner. Various organizations across the world are moving to a hybrid and multi-cloud environment. A thin client contributes to a comparatively less expensive and secure hardware solution, driving the market's growth.

- With the rising adoption of workspace-as-a-service (WaaS) in several enterprises, the market is anticipated to witness augmented demand during the forecast period. WaaS is a desktop virtualization used by multiple organizations to provide their employees access to applications remotely. However, network issues in developing countries for cloud computing are expected to restrain the growth of the studied market.

- Energy companies operating in a geopolitically sensitive industry face frequent cyberattack targets, especially from foreign governments. However, using the cloud as a base for desktop virtualization allows sensitive information to be stored centrally, and authentication policies can be set to secure the cloud environment. This factor is anticipated to generate demand for the thin client market.

- Over the last decades, there has been an increasing trend of remote work. But the effect of COVID-19, which has dramatically accelerated this trend during a very brief period but forced companies regardless of size to adjust quickly to selfisolation measures called for by governments around the world, is rapidly accelerating it. With the pandemic requiring more people to be working remotely, the concern regarding the security of data sharing among employees increased. This has been driving the adoption of the demand for thin-client devices.

Thin Client Market Trends

The Healthcare Segment is Expected to Drive the Market's Growth

- Healthcare providers are stringent in offering the highest standards of patient care. They are acutely attuned to the technologies they use to improve the patient experience at every stage of care. From admissions to the emergency room to rehabilitation and outpatient care, the technology can significantly impact patient outcomes and critically impact providers' productivity and operational costs.

- This holds especially true for the ubiquitous desktop computing infrastructure across the healthcare domain. The legacy desktop PC model, data, and applications reside locally on individual PCs distributed across the network, often yielding a cluster of individually configured and managed PCs. These are associated with sensitive patient data, often with little to no parameter uniformity.

- However, with thin clients, data and applications are remotely administered, stored, and centralized in the data center or cloud infrastructure. The thin client is simply the access portal, giving administrators and clinicians immediate access to their applications and patient data as their credentials allow.

- By the nature of their architecture, thin clients offer various security advantages to help ensure compliance with HIPAA and other healthcare regulations while minimizing exposure to security threats. Authorized user access to cloud-based data and applications is strictly controlled via user authentication and permissions verification. USB/port protections, smart cards, and firewalls can further augment these security measures.

- Although the industry is currently transitioning into digitization, it has been notoriously recognized to be resistant to changes since any failure of unreliable technology translates into issues that affect patient health. Any deviation from predetermined workflows can adversely affect a hospital's operations. Despite the hesitancy, the industry must accelerate technology adoption to remain compliant with the constantly changing regulations and agreements.

- Such needs have encouraged robust partnership structures designed around maximizing offering capabilities. For instance, in March 2023, Stratodesk, the pioneer of securely managed endpoints for modern workspaces, announced that several LG Business Solutions Thin Clients are now certified with Stratodesk NoTouch OS, providing IT teams with The confidence and flexibility to deploy turnkey systems in both private and public cloud environments.

North America is Expected to Hold a Major Market Share

- North America is expected to dominate the market, primarily due to the main factors such as the increasing adoption of cloud technology and highly technology-oriented products, which require activity and flexibility. IT support is available to the majority of companies in the region. The presence of market leaders, a significant number of cloud service providers, and an increasing number of hosted servers in the area are essential contributors to the market's growth in the region.

- The organizations in the region are early adopters of new technologies, which is the primary driving force behind the region's dominance. Large cloud service providers play a significant role in the region's growth of cloud-based thin client deployment.

- In broadcasting, cloud computing and virtualization are playing an increasing role. Virtual machines and computers that can be remotely controlled through network protocols may provide an optimum complement to the physically available equipment on site.

- The North American IT and telecommunications industry is one of the largest among other regional markets. Industries such as banking, healthcare, and government organizations, which handle a large amount of sensitive information, are looking forward to adopting thin client solutions. They can preserve the integrity of the intellectual property better than a fat client.

- This strong position can be attributed to the presence of several well-established thin client solution providers within the country. Notably, a recent partnership between HP Inc. and Citrix aims to deliver secure and efficient thin client solutions, focusing on enhancing remote work capabilities and seamless access to all virtual desktops and applications.

Thin Client Industry Overview

The thin client market is fragemented and highly competitive due to the presence of many large players in the market providing products in the domestic and international markets. The market appears to be mildly concentrated, with the key players adopting strategies like product and service innovations, partnerships, mergers, and acquisitions to extend their geographic reach and stay ahead of the competitors. Some of the major players in the market are Dell Inc., H.P. Development Company LP, Samsung Group, and L.G. Electronics Inc.

- November 2023 - AWS has announced the launch of Amazon WorkSpaces Thin Client to Revolutionize Enterprise Workspaces and offers quick and reliable access to business applications, catering to customer service, technical support, and healthcare sectors.

- August 2023 - LG Electronics Inc In addition to simplifying expansion, it has launched a series of thin clients in 2023 called CQ which are designed for extended product life, superior safety, high performance, easy connectivity and substantial energy savings that can improve efficiency and productivity. The thin client provides healthcare facilities with an endpoint which delivers reliable performance, strong data protection and a secure virtual desktop experience that can be easily implemented and managed.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Enhanced Network Infrastructure Security

- 5.1.2 Reduction of Cost and Energy Consumption

- 5.2 Market Challenges

- 5.2.1 Network Issues in Developing Countries for Cloud Computing

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Hardware

- 6.1.2 Software and Services

- 6.2 By End User

- 6.2.1 BFSI

- 6.2.2 IT and Telecom

- 6.2.3 Healthcare

- 6.2.4 Government

- 6.2.5 Other End Users (Retail, Manufacturing, Education)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Inc.

- 7.1.2 HP Development Company LP

- 7.1.3 Samsung Group

- 7.1.4 LG Electronics Inc.

- 7.1.5 NEC Corporation

- 7.1.6 Fujitsu Ltd

- 7.1.7 Lenovo Group Limited

- 7.1.8 Cisco Systems Inc.

- 7.1.9 Advantech Co. Ltd

- 7.1.10 Siemens AG

- 7.1.11 IGEL Technology GmbH