|

市場調査レポート

商品コード

1687469

アナログ集積回路(IC)産業- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Analog Integrated Circuit (IC) Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アナログ集積回路(IC)産業- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

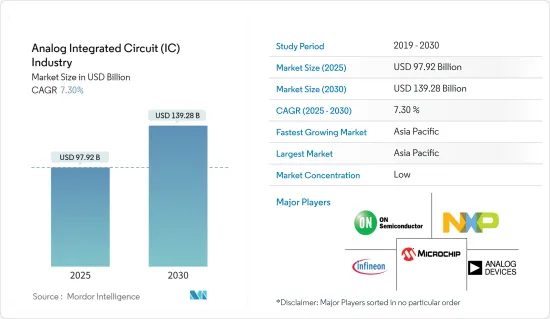

アナログ集積回路産業は、2025年の979億2,000万米ドルから2030年には1,392億8,000万米ドルに成長し、予測期間(2025年~2030年)のCAGRは7.3%になると予測されています。

主なハイライト

- アナログ集積回路(IC)には、1枚の半導体ウエハー上に作られた相互接続部品が含まれます。2つの電圧レベルだけで動作するデジタル回路とは異なり、アナログ部品は連続スペクトルの入力信号に反応します。これらの回路は電子機器に不可欠で、さまざまなエネルギー出力レベルを処理し、鍛造します。発振器、直流増幅器、マルチバイブレーター、オーディオ・アンプなどの機器は、一貫した入出力レベルを確保するためにアナログ回路に依存しています。

- モノのインターネット(IoT)のような技術の台頭は、リアルタイムで接続されるさまざまな機器におけるアナログICの利点を浮き彫りにし、市場の成長を促進します。特に、高速接続、クラウド導入、データ分析の急増に伴い、IoTの足跡は拡大しています。例えば、フォーブス誌は、2024年末までに2,070億台以上のデバイスが世界にネットワーク化されると予測しており、これは市場にとってプラスの成長機会となります。

- アナログICの需要は、スマートフォン、コンピューター、家電、電気自動車のブームに後押しされ、近年急増しています。スマートフォンは、充電IC、ディスプレイPMIC、SoC PMIC、カメラPMICなど、さまざまなICを利用しています。アップル、クアルコム、インテル、サムスンS.LSIなどの業界大手がこの情勢を支配しています。技術的に高度なスマートフォンの生産が増加し、5Gと6Gの統合が進んでいることから、世界のアナログIC市場は大きく成長する見込みです。

- しかし、2023年の世界のスマートフォンのニーズは2022年に比べて落ち込んでおり、その原因はインフレ、個人消費の減退、先行き不透明感です。この落ち込みは、市場の成長にマイナスの影響を与えそうです。しかし、2024年度には、5Gスマートフォンに対する需要の高まりと5Gネットワークの世界の拡大、特に5Gスマートフォンと折りたたみ式スマートフォンの急増により、緩やかな回復が見込まれます。GSMAの予測によると、2025年までに5Gネットワークは世界人口の3分の1をカバーすると予想されています。

- 熟練したアナログチップ設計エンジニアへの依存は顕著です。しかし、半導体業界ではかなり不足しています。インテルのシンディ・ハーパーは、業界の人材需要が供給を上回っていることを強調しました。シーメンスEDAのRuchir Dixit氏によると、米国では今後5年間で25万人の半導体エンジニアが不足すると予想されています。中国と台湾では、それぞれ30万人と5万人のエンジニアが不足すると予想されています。このような不均衡は、市場の成長にとって課題となります。

- ロシア・ウクライナ戦争は、エレクトロニクスを含む複数の産業に波及しました。この地政学的緊張は、既存の半導体サプライチェーンの混乱とチップ不足を激化させました。このような混乱は、ニッケル、パラジウム、銅、シリコン、チタンのような必須原材料の価格変動につながり、材料不足をもたらしました。

- SEMIによると、ロシアは世界のパラジウムの45-50%を供給しており、これは半導体パッケージングに不可欠な材料です。世界の貿易の扉がロシアに閉ざされ、半導体メーカーはますます代替原料ソースを求めるようになり、半導体生産の遅れはさらに長期化します。これは市場の成長を妨げると予想されます。

アナログ集積回路(IC)産業動向

携帯電話サブセグメントが主要シェアを占める見込み

- ダイナミックな技術の世界では、音声通信が主要な機能である携帯電話や多機能ハンドヘルド機器に、特定用途向けアナログICが不可欠となっています。2G、3G、Wimaxのような広範なセルラーネットワーク向けに開発されたこれらのデバイスは、CDMA、GSM、およびそれらの拡張版などの伝送フォーマットを利用しています。

- 特に発展途上諸国でのスマートフォン普及の高まりは、人口増加と都市化が原動力となっています。例えば、GSMAの報告によると、2023年末までに世界人口の69%にあたる56億人がモバイル通信に加入し、2015年以降16億人の普及が見込まれています。

- 5G技術の出現は、5Gスマートフォンの普及につながりました。エリクソン・モビリティ・レポートによると、2028年末までに50億の5Gモバイル契約が記録されると予想されています。これらの5Gネットワークは人口の85%をカバーし、モバイルトラフィックの約70%を運用すると予想されています。

- これらの要因はすべて、携帯電話のサブセグメントのシェアが継続的に増加していることに起因しています。スマートフォンでは、優れたカメラ画質、AR、VRなどの高度な機能に対するニーズが高まっており、これらはすべてアナログICによって実現されています。アナログICの重要性は、アナログ信号を高精度に処理できる点にあります。そのため、信号処理、電源管理、データ変換などのアプリケーションに欠かせないです。さらに、複数のアナログ回路を1つのチップにまとめることで、より小型で効率的、かつコスト効率の高いデバイスを実現できます。

- GSMAは、北米のスマートフォン加入者は2025年までに3億2,800万人に増加し、モバイルの普及率は86%、インターネット利用者は80%に達すると予測しています。エリクソン・モビリティ・レポートによると、中東・アフリカ(MEA)の5G加入者は2024年までに6,000万人に達し、モバイル加入者全体の約3%を占めると予想されています。GSMAは、2025年までにMENAで約5,000万件の5G接続があり、そのうちアラブ諸国だけで2,000万件になると推定しています。これらの数字は、携帯電話の急速な普及を浮き彫りにし、サブセグメントを推進しています。

中国はアジア太平洋で最も急成長する市場になる見込み

- 中国は、大手半導体メーカー、急速な工業化、広大なコンシューマーエレクトロニクスに牽引され、アナログIC市場の重要な企業としての地位を確固たるものにしようとしています。この地域は、半導体の大量生産と、自動車、家電、IT・通信などさまざまな産業でアナログICが広く採用されていることで知られています。こうした力学が中国のアナログIC市場の成長を後押しし、市場関係者に魅力的な展望を提供しています。

- 中国で急成長しているITおよびデータセンター産業は、増え続ける年間データ生成量に直接対応しています。この成長は、主にその活気あるデータセンター・エコシステムによって、世界のハイテク分野で中国の地位が上昇していることによって、さらに強調されています。中国のインターネット・データセンター業界は、世界で最も技術的に進んだ業界のひとつであり、多くの企業がデジタル・プラットフォームを活用しています。

- データセンターへの投資とインターネットの普及に伴い、センサー対応機器の需要も高まっています。物理空間と相互作用するこれらのセンサーには、アナログ信号をデジタル信号に変換するアナログ処理が必要です。これらの機能をデジタル技術と融合させることで、コスト効率や消費電力が低いだけでなく、信頼性も高いソリューションが生まれます。その結果、これらの要素が今後数年間の市場の成長を後押しすると予想されます。

- 拡大する5Gネットワーク機能は、アナログICモジュールの需要を大きく牽引します。5G領域で大きく前進した中国は、5G基地局の広大なネットワークを誇っています。MIITのデータによると、2024年2月末までに、中国は350万以上の5G基地局を設置しました。多額のインフラ投資と野心的な展開戦略により、中国は広範な5Gカバレッジを達成しました。予測によると、2024年末には中国国内の5G基地局数は600万を超えるかもしれないです。

- サウスチャイナ・モーニング・ポストの報道によると、中国のスマートフォン産業は2023年に若返りの兆しを見せ、出荷台数が前年から6.5%増加しました。この回復は、世界最大の携帯電話市場が暫定的な景気回復と国内競争の激化、特にファーウェイ・テクノロジーズが5G領域で顕著な躍進を遂げたことに対処しているためです。

- ITAによると、中国は引き続き世界の自動車市場を席巻しており、年間販売台数と生産台数で首位に立っています。予測によると、国内の自動車生産台数は2025年までに3,500万台に達する可能性があります。さらに、中国汽車工業協会(CAAM)の報告によると、中国の自動車産業は強固な製造基盤に支えられ、輸出台数が前年同期比81%増の176万台に達し、世界の存在感を高めています。この開発力を考えると、中国の現代産業におけるアナログICの需要は相当なものになると予想されます。

アナログ集積回路(IC)産業の概要

- アナログ集積回路(IC)市場予測は、半固有の状況を示しています。メーカー各社は、製品イノベーションと技術差別化を武器に、熾烈な競争を繰り広げています。多くの企業は、先行者利益を確保し競争力を維持するために、アナログICの開発に戦略的に投資しています。この分野の注目すべき企業には、アナログ・デバイセズ社、インフィニオン・テクノロジーズ社、マイクロチップ・テクノロジー社、NXPセミコンダクターズNV社、オン・セミコンダクター社などがあります。

- アナログICの最近の進歩は、消費電力を抑えながら性能を向上させることに集中しています。特筆すべきは、アナログ回路とデジタル回路をワンチップに統合したミックスドシグナルICです。

- この統合は、特にデータ・コンバータやセンサー・インターフェイスのようなアプリケーションにおいて、複雑で効率的なシステムへの道を開くものです。さらに、シリコン・ゲルマニウム(SiGe)やシリコン・オン・インシュレーター(SOI)などの高度な製造技術も、アナログ回路の性能を高めるために活用されています。

- 今後は、ICレベルの枠を超え、システム・レベルでアナログ回路とデジタル回路を統合する方向へのシフトが顕著になります。システムオンチップ(SoC)技術と呼ばれるこの変化は、より効率的でコスト効率の高いデバイスを約束します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- マクロ経済動向が市場に与える影響

第5章 市場力学

- 市場促進要因

- スマートフォン、フィーチャーフォン、タブレット端末の普及率上昇

- 市場の課題

- アナログICの設計複雑化

第6章 市場セグメンテーション

- タイプ別

- 汎用IC

- インターフェース

- 電源管理

- 信号変換

- アンプ/コンパレータ(シグナル・コンディショニング)

- 特定用途向けIC

- 民生用

- オーディオ/ビデオ

- デジタルスチルカメラ/ビデオカメラ

- その他コンシューマー

- 自動車

- インフォテイメント

- その他インフォテインメント

- 通信機器

- 携帯電話

- インフラ

- 有線通信

- 近距離通信

- その他ワイヤレス

- コンピューター

- コンピュータシステムとディスプレイ

- コンピュータ周辺機器

- ストレージ

- その他コンピュータ

- 産業用その他

- 汎用IC

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 ベンダー市場シェア分析

第8章 競合情勢

- 企業プロファイル

- Analog Devices Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- NXP Semiconductors NV

- ON Semiconductor

- Richtek Technology Corporation(MediaTek Inc.)

- Skyworks Solutions Inc.

- STMicroelectronics NV

- Renesas Electronics Corporation

- Texas Instruments Inc.

- Qorvo Inc.

第9章 アナログIC市場の価格分析

第10章 投資分析

第11章 投資分析市場の将来

目次

Product Code: 63830

The Analog Integrated Circuit Industry is expected to grow from USD 97.92 billion in 2025 to USD 139.28 billion by 2030, at a CAGR of 7.3% during the forecast period (2025-2030).

Key Highlights

- Analog integrated circuits (ICs) include interconnected components crafted on a single semiconducting wafer. Unlike digital circuits, which operate on just two voltage levels, analog components react to a continuous spectrum of input signals. These circuits are integral to electronic devices, processing and forging various energy output levels. Appliances such as oscillators, DC amplifiers, multi-vibrators, and audio amplifiers rely on analog circuits to ensure consistent input and output levels.

- The rise of technologies like the Internet of Things (IoT) is set to drive market growth, highlighting the advantages of analog ICs in a wide array of real-time connected devices. Notably, IoT's footprint is expanding with the surge in high-speed connectivity, cloud adoption, and data analytics. For example, Forbes projects over 207 billion devices will be globally networked by the closing of 2024, which presents a positive growth opportunity for the market.

- The demand for analog ICs has surged in recent years, fueled by the boom in smartphones, computers, consumer electronics, and electric vehicles. Smartphones utilize various ICs, including charge ICs, display PMICs, SoC PMICs, and Camera PMICs. Industry giants like Apple, Qualcomm, Intel, and Samsung S.LSI dominate this landscape. Given the rising production of technologically advanced smartphones and the integration of 5G and 6G, the global analog IC market is poised for significant growth.

- However, a dip was witnessed in global smartphone need in 2023 compared to 2022, attributed to inflation, waning consumer spending, and a subdued outlook. This downturn is likely to influence market growth negatively. However, a modest recovery is expected in FY 2024 owing to the rising demand for 5G smartphones and the global expansion of 5G networks, especially with the surge in 5G and foldable smartphones. According to GSMA forecasts, by 2025, 5G networks are expected to encompass a third of the global population.

- The reliance on skilled analog chip design engineers is pronounced. However, there is a substantial scarcity in the semiconductor industry. Cindi Harper from Intel highlighted that industry demand for talent outstrips supply. According to Ruchir Dixit of Siemens EDA, a shortfall of 250,000 semiconductor engineers is expected to be seen in the United States over the next five years. In China and Taiwan, deficits of 300,000 and 50,000 engineers are expected, respectively. Such imbalances pose challenges to market growth.

- The Russia-Ukraine War reverberated across multiple industries, including electronics. This geopolitical tension intensified existing semiconductor supply chain disruptions and chip shortages. Such disturbances have led to price volatility in essential raw materials like nickel, palladium, copper, silicon, and titanium, resulting in material shortages.

- According to SEMI, Russia supplied 45-50% of the world's palladium, a crucial material for semiconductor packaging. With global trading doors closing on Russia, semiconductor manufacturers are increasingly pursuing alternative raw material sources, further prolonging semiconductor production delays. This is expected to hamper the growth of the market.

Analog Integrated Circuit (IC) Industry Trends

The Cell Phone Sub-segment is Expected to Hold a Major Share

- In the dynamic world of technology, application-specific analog ICs have become essential for cellular phones and multifunctional handheld devices, where voice communication remains a primary function. These devices, developed for extensive cellular networks like 2G, 3G, and Wimax, utilize transmission formats such as CDMA, GSM, and their enhanced versions.

- Rising smartphone adoption, particularly in developing countries, is driven by population growth and urbanization. For instance, by the end of 2023, GSMA reported that 5.6 billion people, or 69% of the global population, had subscribed to mobile benefits, marking a proliferation of 1.6 billion since 2015.

- The emergence of 5G technology has led to the adoption of 5G smartphones. According to Ericsson Mobility Report, 5 billion 5G mobile subscriptions are expected to be recorded by the end of 2028. These 5G networks are anticipated to cover 85% of the population and operate about 70% of mobile traffic.

- All these factors can be attributed to the continuously increasing share of the cell phone sub-segment of the market as there is an increasing need for advanced features in smartphones, such as great camera quality, AR, and VR, all of which are made possible by analog ICs. The importance of analog ICs lies in their ability to process analog signals with high precision and accuracy. This makes them critical for signal processing, power management, and data conversion applications. Additionally, combining multiple analog circuits on a single chip permits for smaller, more efficient, and cost-effective devices.

- GSMA projects that North America will see smartphone subscribers rise to 328 million by 2025, with mobile penetration at 86% and internet users at 80%. According to Ericsson Mobility Report, Middle East and Africa (MEA) is expected to have 60 million 5G subscribers by 2024, accounting for roughly 3% of total mobile subscriptions. GSMA estimates that there will be about 50 million 5G connections in MENA by 2025, with 20 million in the Arab states alone. These figures highlight the rapid adoption of cell phones, propelling the sub-segment forward.

China is Expected to be the Fastest-growing Market in Asia-Pacific

- China is set to solidify its position as a critical player in the analog IC market, driven by major semiconductor manufacturers, swift industrialization, and a sprawling consumer electronics landscape. The region is celebrated for its high-volume semiconductor production and the widespread adoption of analog ICs across various industries, including automotive, consumer electronics, and telecommunications. These dynamics are poised to propel the growth of the analog IC market in China, offering enticing prospects for market players.

- China's burgeoning IT and data center industry directly responds to the ever-increasing annual data generation. This growth is further underscored by China's rising stature in the global tech arena, primarily fueled by its vibrant data center ecosystem. China's internet data center industry is among the world's most technologically advanced, with many organizations leveraging digital platforms.

- With the increase in investments in data centers and internet penetration, the demand for sensor-enabled devices is also rising. These sensors, which interact with the physical space, necessitate analog processing to convert analog signals to digital ones. Merging these functionalities with digital technology yields a solution that is not only cost-effective and low-power but also reliable. Consequently, these elements are anticipated to bolster the market's growth in the coming years.

- The expanding 5G networking capabilities are set to drive significant demand for analog IC modules. Having made substantial strides in the 5G domain, China boasts a vast network of 5G base stations. Data from MIIT indicates that by the close of February 2024, China had established over 3.5 million 5G base stations. Owing to its hefty infrastructure investments and ambitious rollout strategies, the nation achieved widespread 5G coverage. Projections suggest that by the end of 2024, the number of 5G base stations in China might exceed six million.

- According to a report from South China Morning Post, China's smartphone industry showed signs of rejuvenation in 2023, witnessing a 6.5% uptick in shipments from the prior year. This rebound came as the world's largest handset market grappled with a tentative economic recovery and heightened domestic competition, especially with Huawei Technologies making notable strides in the 5G domain.

- According to ITA, China continues to dominate the global automotive landscape, leading in annual sales and manufacturing output. Projections indicate domestic vehicle production could reach 35 million by 2025. Furthermore, bolstered by a robust manufacturing base, China's automotive industry amplified its global presence, with exports soaring 81% year-on-year, totaling 1.76 million vehicles in the initial five months of 2023, as reported by the China Association of Automobile Manufacturers (CAAM). Given this development prowess, the demand for analog ICs in modern Chinese industries is anticipated to be substantial.

Analog Integrated Circuit (IC) Industry Overview

- The analog Integrated Circuit (IC) market forecast indicates a semi-consolidated landscape. Manufacturers are committed to fierce competition, leveraging product innovation and technological differentiation. Many companies strategically invest in developing analog ICs to secure a first-mover advantage and maintain competitiveness. Notable players in this arena include Analog Devices Inc., Infineon Technologies AG, Microchip Technology Inc., NXP Semiconductors NV, and ON Semiconductor.

- Recent advancements in analog ICs have centred on enhancing performance while curbing power consumption. A notable stride has been in mixed-signal ICs, which merge analog and digital circuits onto a single chip.

- This integration paves the way for intricate and efficient systems, especially for applications like data converters and sensor interfaces. Additionally, advanced fabrication technologies, including silicon-germanium (SiGe) and silicon-on-insulator (SOI), have been harnessed to elevate analog circuit performance.

- Looking ahead, there's a pronounced shift towards integrating analog and digital circuits at the system level, moving beyond the confines of the IC level. This change, termed system-on-a-chip (SoC) technology, promises more efficient and cost-effective devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Penetration of Smartphones, Feature Phones, and Tablets

- 5.2 Market Challenges

- 5.2.1 Increasing Design Complexity of Analog IC

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 General-Purpose IC

- 6.1.1.1 Interface

- 6.1.1.2 Power Management

- 6.1.1.3 Signal Conversion

- 6.1.1.4 Amplifiers/Comparators (Signal Conditioning)

- 6.1.2 Application-Specific IC

- 6.1.2.1 Consumer

- 6.1.2.1.1 Audio/Video

- 6.1.2.1.2 Digital Still Camera and Camcorder

- 6.1.2.1.3 Other Consumers

- 6.1.2.2 Automotive

- 6.1.2.2.1 Infotainment

- 6.1.2.2.2 Other Infotainment

- 6.1.2.3 Communication

- 6.1.2.3.1 Cell Phone

- 6.1.2.3.2 Infrastructure

- 6.1.2.3.3 Wired Communication

- 6.1.2.3.4 Short Range

- 6.1.2.3.5 Other Wireless

- 6.1.2.4 Computer

- 6.1.2.4.1 Computer System and Display

- 6.1.2.4.2 Computer Periphery

- 6.1.2.4.3 Storage

- 6.1.2.4.4 Other Computers

- 6.1.2.5 Industrial and Others

- 6.1.1 General-Purpose IC

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 VENDOR MARKET SHARE ANALYSIS

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Analog Devices Inc.

- 8.1.2 Infineon Technologies AG

- 8.1.3 Microchip Technology Inc.

- 8.1.4 NXP Semiconductors NV

- 8.1.5 ON Semiconductor

- 8.1.6 Richtek Technology Corporation (MediaTek Inc.)

- 8.1.7 Skyworks Solutions Inc.

- 8.1.8 STMicroelectronics NV

- 8.1.9 Renesas Electronics Corporation

- 8.1.10 Texas Instruments Inc.

- 8.1.11 Qorvo Inc.