|

市場調査レポート

商品コード

1907223

日本のペットフード市場- シェア分析、業界動向、統計、成長予測(2026年~2031年)Japan Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のペットフード市場- シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

概要

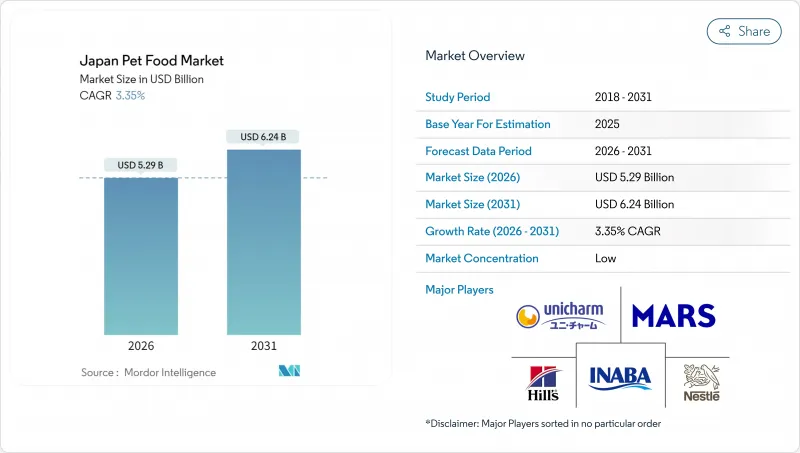

2026年の日本のペットフード市場規模は52億9,000万米ドルと推定され、2025年の51億2,000万米ドルから成長が見込まれます。

2031年の予測では62億4,000万米ドルに達し、2026年から2031年にかけてCAGR3.35%で拡大する見通しです。

この成長は、成熟したペット飼育基盤に支えられており、世帯の38.1%を占める単身世帯が、伴侶としてペットへの依存度を高めています。プレミアム化も重要な要因であり、ペットオーナーはペットの健康と幸福を確保するため、機能性成分、有機配合、獣医師処方療法食を優先しています。その他の成長要因としては、利便性と幅広い製品へのアクセスを提供するデジタルコマースの台頭、自然災害に脆弱な日本の状況による防災備蓄、限られたスペースの都市部アパートに適した小型ペットへの移行などが挙げられます。ただし、ペットの食事管理をより重視する飼い主層に支持される手作りペットフードの流行や、サプライチェーンを混乱させる可能性のある輸入規制の定期的な実施といった動向が、販売数量の伸びをやや抑制しています。市場は依然として分散状態にあり、世界の企業と国内メーカーが品質、安全性、ブランド信頼性に基づいて競合しています。各社は、変化する消費者の嗜好に応えるため、イノベーションとカスタマイズされた製品提供に注力しています。

日本のペットフード市場の動向と分析

ペットの人間化がプレミアム化を牽引

日本の飼い主様はペットを家族の一員として扱う傾向が強まり、人間と同等の栄養を求める需要が高まっています。オーガニックやナチュラル配合の製品が急速に増加しており、日本のペットフード市場全体の伸びを大きく上回っています。クリーンラベル要件、単一タンパク質レシピ、透明性のある原料調達が新製品発売の主流となっており、添加物基準の改定によりコンプライアンスが強化されています。人間向け加工技術と原料のトレーサビリティを提供するブランドは、購入意欲を損なうことなく20~30%の価格プレミアムを実現しています。機能性成分に対する獣医師の推奨拡大や、オーガニックメニューを提供するペットカフェの台頭が、この動向をさらに加速させており、日本におけるペット食の構造的変化、すなわち健康志向への移行を示しています。

機能性食を必要とする高齢化ペット数

高齢ペットの割合は、日本の人口高齢化を反映するほど増加しており、飼い主様は事後対応的なケアよりも治療的栄養管理を優先される傾向が強まっています。獣医用フード市場は急速に拡大しており、標準的な配合にはオメガ3脂肪酸、プロバイオティクス、関節サポート栄養素が標準装備されています。年齢別調査、臨床検証、動物病院との連携に投資する企業は、健康志向の世帯におけるブランドロイヤルティを強化しています。予防医療への意識の高まり、獣医受診の増加、ペット保険の普及が相まって、日本では高齢ペット向け専門栄養への長期的な移行が加速しています。

出生率の低下による長期的なペット増加の抑制

日本の合計特殊出生率は2024年に1.26人まで低下し、25~35歳が中心となる初めてのペット飼育者の層が縮小しています。地方の人口減少がこの動向を加速させ、既存の飼い主が1匹あたりの支出を増やす一方で、将来の顧客基盤は縮小傾向にあります。したがって、長期的な成長は世帯数の拡大ではなく、プレミアム化に依存します。この人口構成の不均衡により、日本のペットフード市場は高付加価値・低ボリュームのダイナミクスへと移行しています。

セグメント分析

2025年時点で、ペットフード市場シェアの73.55%をフードが占め、おやつ、サプリメント、獣医用フードを大きく引き離しています。ドライフードが販売数量の基軸であり続ける一方、嗜好性と水分補給を重視するプレミアムブランドにおいてウェットフードのシェアが拡大しています。おやつは売上高で第2位を占め、ご褒美需要の動向により最も急速な成長を見せています。栄養補助食品と獣医用フードは規模こそ小さいもの、専門家の推奨や保険適用により支えられた高価格帯のニッチ市場として存在感を維持しています。

ペット用おやつは2031年までにCAGR5.86%と最も高い伸びが予測され、日本のペットフード市場全体の基準値3.35%を上回ります。獣医用ダイエットフードは専門的ながら成長分野であり、獣医師の推奨増加と治療用栄養食品のコスト障壁を軽減するペット保険の普及が追い風となっています。この分野の成長は、日本の高度な獣医療インフラと、飼い主が医療処方ソリューションに投資する意欲を反映しています。

本「日本のペットフード市場レポート」は、ペットフード製品別(フード、ペット用栄養補助食品/サプリメント、ペット用おやつなど)、ペット別(猫、犬など)、流通チャネル別(コンビニエンスストア、オンラインチャネル、専門店、スーパーマーケット/ハイパーマーケットなど)に分類されています。市場予測は金額(米ドル)および数量(メトリックトン)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 エグゼクティブサマリーおよび主要な調査結果

第3章 レポート提供

第4章 主要業界動向

- ペットの飼育数

- 猫

- 犬

- その他のペット

- ペット関連支出

- 消費者の動向

第5章 供給と生産の動向

- 貿易分析

- 原材料の動向

- バリューチェーンと流通チャネル分析

- 規制の枠組み

- 市場促進要因

- ペットの人間化が進み、プレミアム化が加速

- 高齢化するペット数による機能性フードの需要増加

- Eコマース普及によるアクセシビリティの拡大

- 単身世帯の増加がペット飼育を促進

- 政府の防災対策が備蓄需要を促進

- ペット同伴可能なオフィスが増加し、平日のご褒美需要が高まっています

- 市場抑制要因

- 出生率の低下による長期的なペット増加の抑制

- 原材料規制の厳格化によるコスト上昇

- 手作りペットフードがパッケージ商品の売上を食い荒らす

- 人獣共通感染症への懸念による輸入禁止が供給ショックを引き起こす

第6章 市場規模と成長予測(金額と数量)

- ペットフード製品

- フード

- 製品別

- ドライペットフード

- ペット用ドライフードのサブカテゴリー別

- キブル

- その他のドライペットフード

- ペット用ドライフードのサブカテゴリー別

- ウェットペットフード

- ドライペットフード

- 製品別

- ペット用栄養補助食品/サプリメント

- 製品別

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質およびペプチド

- ビタミン・ミネラル

- その他の栄養補助食品

- 製品別

- ペット用おやつ

- 製品別

- カリカリおやつ

- デンタルおやつ

- フリーズドライ・ジャーキーおやつ

- ソフトで噛み応えのあるおやつ

- その他のおやつ

- 製品別

- ペット用医療食

- 製品別

- 皮膚用ダイエットフード

- 糖尿病

- 消化器系敏感性

- 肥満用ダイエットフード

- 口腔ケア用フード

- 腎臓用

- 尿路疾患

- その他の獣医用ダイエットフード

- 製品別

- フード

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- Brand Positioning Matrix

- Market Claim Analysis

- 企業概況

- 企業プロファイル

- Unicharm Corporation

- Mars, Incorporated

- Inaba-Petfood Co., Ltd.

- Nestle(Purina)

- Colgate-Palmolive Company(Hill's Pet Nutrition, Inc.)

- General Mills Inc.

- ADM

- Schell & Kampeter, Inc.(Diamond Pet Foods)

- Clearlake Capital Group, L.P.(Wellness Pet Company, Inc.)

- Virbac S.A.

- Spectrum Brands, Inc.,

- Nippon Pet Food Co., Ltd.

- DoggyMan H.A.Co.,Ltd.

- Petio Corp.

- Earth Pet Co.,Ltd.