|

市場調査レポート

商品コード

1693908

リチウム硫黄電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Lithium Sulfur Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| リチウム硫黄電池:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

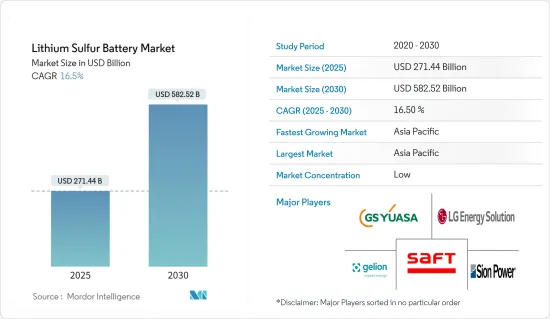

リチウム硫黄電池市場規模は2025年に2,714億4,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは16.5%で、2030年には5,825億2,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、排出量削減のための各国の支援施策や取り組みによる電気自動車需要の増加や、再生可能エネルギー導入の増加に伴うエネルギー貯蔵装置需要の増加などの要因が、予測期間中の市場成長を促進します。

- 一方、リチウム硫黄電池の高コストが予測期間中の市場成長を抑制する可能性が高いです。

- 電池技術の進歩により、エンドユーザー産業全体の需要は劇的に増加しています。また、軍事・航空セグメント向けの高エネルギー密度電池を開発するための政府投資も増加しています。このため、予測期間中に調査される市場には計り知れない機会が生まれる可能性が高いです。

- 予測期間中、アジア太平洋が最大かつ最も急成長している市場になると予想され、需要の大半は中国、日本などの国々からもたらされます。

リチウム硫黄電池の市場動向

市場を独占する航空宇宙セグメント

- 航空宇宙セグメントでは、電池は重要な部品であり、人工衛星、高高度航空機、宇宙船、無人航空機など複数の用途に使用されています。航空宇宙セグメントの電池には、一次電池(単回使用)と二次電池(充電式)があります。航空機に搭載されたり、定期的に携行される機器の電源として使用される電池は、安全で、エネルギー密度が高く、軽量で、信頼性が高く、メンテナンスが最小限で済み、さまざまな環境条件下で効率的に機能するものでなければならないです。

- 航空宇宙セグメントでは、より高いエネルギー密度を持つ電池が必要とされるため、リチウム硫黄電池の設置が増加しています。そのため、より長寿命で強力なエネルギー貯蔵が可能になります。航空宇宙部門はまた、低排出源に向かっています。

- 米国の電池新興企業であるライテンは、エネルギー密度の高いリチウム硫黄電池の潜在市場として電気航空機に注目しています。2023年6月、同社はシリコンバレーでリチウム硫黄電池のパイロットラインを稼働させたと発表しました。このリチウム硫黄電池パイロットラインは、防衛、ロジスティクス、自動車、衛星の各セグメントの早期採用顧客向けに、2023年に業務用電池セルの納入を開始する予定です。

- さらに、このような電池を搭載可能なドローンの活用が世界的に進んでいます。ドローン製造への投資も大きく伸びています。

- 2023年7月、DroneShieldは無名の米国政府機関から3,300万米ドルの契約を獲得しました。この契約は、複数のドローンの制御・航行能力を妨害するために使用できるDroneGun Mk4などの機器の供給を対象としています。

- 航空セグメントの成長は、最近の航空運賃の安さによる世界の航空旅客数の増加、経済状況の開発、可処分所得の増加が主要因となっています。

- コロナウイルスの大流行により、国際航空運送協会(IATA)によると、民間航空会社は2022年に約7,270億米ドルの収益を上げました。しかし、市場の収益は2023年末までに7,790億米ドルに達すると推定されています。

- 上記の要因は、航空宇宙セグメントの成長を促進し、予測期間中のリチウム硫黄電池の需要を押し上げる可能性が高いです。

アジア太平洋が市場を独占する

- アジア太平洋が世界のリチウム硫黄電池市場を独占すると予想されます。中国、日本、韓国など、この地域の国々は主要な支持国であり、市場の成長に貢献しています。オーストラリア、インド、ベトナムなどの国も、予測期間中に自国にリチウムベースの電池製造施設を設置する計画を進めています。

- 同地域では、隅々までクリーンな電力を供給し、照明や携帯電話の充電ニーズに必要な灯油やディーゼルなどの従来型燃料への依存を減らす努力が顕著です。リチウム硫黄電池一体型エネルギー貯蔵ソリューションは、高いエネルギー密度や貯蔵容量といったその技術的な利点により、採用率が高まることが予想されます。

- この地域におけるこれらの電池の需要は、オングリッドとオフグリッド用途でのエネルギー貯蔵システムや電気自動車の採用により、急速に成長すると予想されます。さらに、再生可能エネルギー発電設備の設置が増加していることも、こうした電池の需要を押し上げています。

- さらに、中国政府は電気自動車の販売を促進するため、全国的な充電ステーション建設に投資しています。例えば、2022年1月、中国政府は2025年までに電気自動車2,000万台分の充電ステーションを建設する計画を発表しました。

- 充電インフラの開発は、同国のEV普及を後押ししています。2022年5月現在、中国電気自動車充電インフラ推進連盟(EVCIPA)は、806基の交流充電ステーション、61万3,000基の直流充電ステーション、485基の直流・交流複合充電ステーションを含め、全国に約142万基の充電ステーションがあることを確認しています。

- 日本は、「Well-to-Wheel Zero Emission」と名付けられた施策を確立することを目指しており、世界の排出量ゼロへの取り組みと歩調を合わせ、2050年までにエネルギー供給と自動車技術革新に焦点を当て、すべての自動車をEVに置き換えることで、乗用車1台当たり約90%の削減を含め、1台当たり約80%の温室効果ガス排出量削減を目指しています。このような政府の取り組みは、電子自動車の需要を増加させる可能性が高く、その結果、リチウム硫黄電池の需要も増加すると予想されます。

- 同様に、韓国政府は2023年4月、主要電池企業3社(LG Energy Solution社、SamsungSDI、SK on)と提携し、固体電池を含む先進電池技術を開発するため、2030年までに151億米ドルを共同投資する計画を発表しました。

- このイニシアティブにより、韓国は世界の競合他社に先駆けて固体電池の商業生産を開始できるようになります。参加する電池企業は、韓国内にパイロット生産工場を設立し、製品開発と製造技術革新の拠点とします。これらの施設は、海外の生産拠点で大量生産を開始する前に、固体電池を含む先進製品のテストと製造に使用されます。この取り組みの一環として、LG Energy Solutionsは2027年までにリチウム硫黄電池の生産を商業化する目標を掲げており、まずは主に航空宇宙セグメント向けに生産を開始します。

- したがって、上記の要因から、予測期間中はアジア太平洋がリチウム硫黄電池市場を独占すると予想されます。

リチウム硫黄電池産業概要

リチウム硫黄電池市場はセグメント化されています。同市場の主要企業には、GS Yuasa Corporation、LG Energy Solutions Ltd、Saft Groupe SA、Gelion PLC、Sion Power Corporationなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- エネルギー貯蔵システム(ESS)の需要増加

- 抑制要因

- 限られたサイクル寿命と耐久性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- エンドユーザー

- 航空宇宙

- エレクトロニクス

- 自動車

- 電力セクタ

- その他

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競争情勢

- 合併、買収、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- GS Yuasa Corporation

- Sion Power Corporation

- LG Energy Solutions Ltd

- Li-S Energy Limited

- Polyplus Battery Co.

- Saft Groupe SA

- Gelion PLC

- LYTEN Batteries Inc.

第7章 市場機会と今後の動向

- 電池技術の進歩

目次

Product Code: 50000866

The Lithium Sulfur Battery Market size is estimated at USD 271.44 billion in 2025, and is expected to reach USD 582.52 billion by 2030, at a CAGR of 16.5% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing demand for electric vehicles due to the various countries' supportive government policies and initiatives to reduce emissions and the increasing demand for energy storage devices amid increasing renewable energy installation drive growth in the market during the forecast period.

- On the other hand, the high cost of lithium-sulfur batteries is likely to restrain the market growth during the forecast period.

- Nevertheless, advancements in battery technology have dramatically increased the demand across end-user industries. Also, the government's investment is increasing to develop high-energy-density batteries for the military and aviation sectors. This will likely create immense opportunities for the market studied during the forecast period.

- The Asia-Pacific is expected to be the largest and fastest-growing market during the forecast period, with most of the demand coming from countries like China, Japan, and other countries.

Lithium Sulfur Battery Market Trends

Aerospace Segment to Dominate the Market

- In the aerospace sector, batteries are a vital component and have multiple applications in satellites, high-altitude aircraft, outer space vehicles, and unmanned aerial vehicles. Batteries in aerospace can be either primary (single-use) or secondary (rechargeable). Any battery designated for use as a power source in aircraft-installed or regularly carried equipment must be secure, have a high energy density, be lightweight, dependable, require minimal maintenance, and efficiently function in various environmental conditions.

- The installation of lithium-sulfur batteries is increasing across the aerospace sector as this sector requires batteries with higher energy density. Therefore, it can provide longer-lasting and more powerful energy storage. The aerospace sector is also moving toward lower emission sources.

- Lyten, a US-based battery startup company, is looking toward electric aircraft as a potential market for its energy-dense lithium-sulfur batteries. In June 2023, the company announced the commissioning of its lithium-sulfur battery pilot line in Silicon Valley. The lithium-sulfur pilot line is expected to start delivering commercial battery cells in 2023 to early adopting customers within the defense, logistics, automotive, and satellite sectors.

- Furthermore, the utilization of drones for various purposes is increasing worldwide, which can be equipped with such batteries. The investment in manufacturing drones is growing significantly.

- In July 2023, DroneShield was awarded a USD 33 million contract with an unnamed U.S. government agency. The contract covers the supply of equipment such as DroneGun Mk4, which can be used to disrupt the control and navigation capabilities of multiple drones.

- The growth in the aviation sector is mainly driven by the increasing number of air passengers globally because of the cheaper airfare in recent times, developing economic conditions, and rising disposable income.

- Due to the coronavirus pandemic, According to the International Air Transport Association (IATA), commercial airlines generated about USD 727 billion in revenue in 2022. However, the market's revenue was estimated to reach USD 779 billion by the end of 2023.

- The abovementioned factors will likely drive growth in the aerospace sector, boosting the demand for lithium-sulfur batteries during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the global lithium-sulfur battery market. Countries in the region, such as China, Japan, and South Korea, are the leading supporters and are contributing to the growth of the market studied. Countries like Australia, India, and Vietnam are also following plans to set up lithium-based battery manufacturing facilities in their countries during the forecast period.

- The region is significantly making efforts to supply clean electricity to every corner and reduce dependency on conventional fuels, such as kerosene and diesel, for their lighting and mobile phone charging needs. Lithium-sulfur battery integrated energy storage solutions will likely witness an increasing adoption rate due to their technical benefits, such as high energy density and storage capacity.

- The demand for these batteries in the region is expected to grow rapidly, owing to the adoption of energy storage systems and electric vehicles for on-grid and off-grid applications. Further, the increasing installation of renewable energy generation facilities also boosts the demand for such batteries.

- Furthermore, the Chinese government is investing in building charging stations nationwide to promote electric vehicle sales. For instance, in January 2022, the Chinese government announced plans to build enough charging stations for 20 million electric vehicles by 2025.

- The development of charging infrastructure is propelling EV adoption in the country. As of May 2022, China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA) confirmed that there were nearly 1.42 million charging stations across the country, including 806 AC charging stations, 613 thousand DC charging stations, and 485 DC-AC combined charging stations.

- Japan aims to establish a policy named 'Well-to-Wheel Zero Emission,' in line with the global efforts to eliminate emissions, focusing on energy supply and vehicle innovation by 2050 and replacing all vehicles with EVs to reduce greenhouse gas emissions by around 80% per vehicle, including an approximate 90% reduction per passenger vehicle. Such government initiatives are likely to increase the demand for electronic vehicles, which, in turn, is expected to increase the demand for lithium-sulfur batteries.

- Similarly, in April 2023, the South Korean government, in partnership with the three leading battery companies (LG Energy Solution Ltd, Samsung SDI Co., Ltd and SK on Co., Ltd.), announced plans to jointly invest USD 15.1 billion by 2030 to develop advanced battery technologies, including solid-state batteries.

- The initiative will enable South Korea to begin commercial production of solid-state batteries ahead of global competitors. The participating battery firms will establish pilot production plants in South Korea, serving as centers for product development and manufacturing innovation. These facilities will be used to test and manufacture advanced products, including solid-state batteries, before initiating mass production at overseas production sites. As a part of this effort, LG Energy Solutions set out a target for commercializing the production of lithium-sulfur batteries by 2027, primarily for the aerospace sector to start with.

- Therefore, based on the above factors, the Asia-Pacific is expected to dominate the lithium-sulfur battery market during the forecast period.

Lithium Sulfur Battery Industry Overview

The lithium-sulfur battery market is fragmented. Some of the major players in the market include (in no particular order) GS Yuasa Corporation, LG Energy Solutions Ltd, Saft Groupe SA, Gelion PLC, and Sion Power Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Electric Vehicles

- 4.5.1.2 Increasing Demand for Energy Storage Systems (ESS)

- 4.5.2 Restraints

- 4.5.2.1 Limited Cycle Life and Durability

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Aerospace

- 5.1.2 Electronics

- 5.1.3 Automotive

- 5.1.4 Power Sector

- 5.1.5 Other End Users

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 GS Yuasa Corporation

- 6.3.2 Sion Power Corporation

- 6.3.3 LG Energy Solutions Ltd

- 6.3.4 Li-S Energy Limited

- 6.3.5 Polyplus Battery Co.

- 6.3.6 Saft Groupe SA

- 6.3.7 Gelion PLC

- 6.3.8 LYTEN Batteries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Battery Technology