|

|

市場調査レポート

商品コード

1431615

衛星用コンポーネント:市場シェア分析、産業動向、成長予測(2024~2029年)Satellite Component - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星用コンポーネント:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

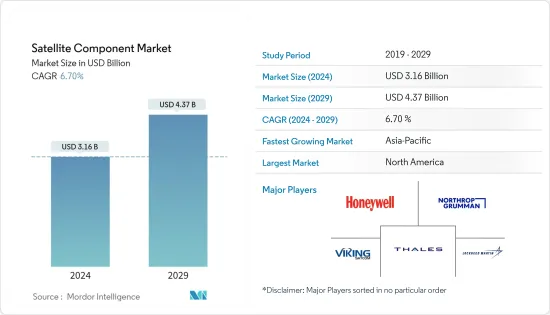

衛星用コンポーネント市場規模は2024年に31億6,000万米ドルと推定され、2029年には43億7,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは6.70%で成長します。

主なハイライト

- 世界の衛星用コンポーネント市場は、COVID-19パンデミックによりかつてない課題に直面しています。宇宙分野は、原材料の不足、衛星打ち上げ計画の遅延、政府による厳しい規制によるサプライチェーンの混乱といった課題を目の当たりにしました。パンデミック後、市場は力強い回復を見せた。宇宙分野への支出の増加と小型衛星打ち上げの増加が、パンデミック後の市場成長を牽引しています。

- 衛星用コンポーネントは、通信システム、電力システム、電源システム、その他で構成されます。通信システムには、信号の受信と再送信を行うアンテナと中継器が含まれます。推進系は衛星を推進するロケットで構成され、電力系は電力を供給するソーラーパネルで構成されます。衛星打ち上げ数の増加と宇宙分野への支出の増加が市場成長の原動力となっています。国連宇宙部(UNOOSA)の指標によると、2022年には8,261個の衛星が地球を周回しており、2021年4月と比較して11.84%増加しています。

衛星用コンポーネント市場動向

アンテナセグメントは予測期間中に著しい成長を示すと予測

- アンテナセグメントは予測期間中に著しい成長を示すと予測されています。この成長の背景には、高度な通信システムへの需要の増加、衛星打ち上げ数の増加、宇宙分野への支出の増加があります。衛星アンテナは、衛星の送信電力を地球上の指定された地理的領域に集中させ、信号全体の品質を劣化させる望ましくない信号からの干渉を避けるために使用されます。通信、放送、ナビゲーション、天気予報など、様々な最終用途の衛星打ち上げの増加が、このセグメントの成長を牽引しています。

- 米国宇宙局(UNOOSA)は、2022年11月に155回の軌道上およびサブオービタル打ち上げが行われたと発表しています。さらに2022年6月、衛星産業協会(SIA)は第25回衛星産業現状報告(SSIR)を発表しました。同報告書によると、2021年の商業衛星配備数は1,713機と、2020年比で40%以上の著しい急増を示しました。この衛星需要の高まりは、衛星用コンポーネントへの対応ニーズを引き起こし、予測期間中の市場成長を促進します。その一例として、2022年7月にMDA Ltd.が衛星メーカーのヨーク・スペース・システムズと衛星用Kaバンドステアラブルアンテナの建設契約を締結したことが挙げられます。

予測期間中、北米が市場で上位を占める

- 北米が衛星用コンポーネント市場を独占し、予測期間中もその支配は続く。米国航空宇宙局(NASA)やSpaceXによる宇宙研究開発への支出の増加や衛星打ち上げ数の増加が背景にあります。2022年、米国政府は宇宙プログラムに約620億米ドルを支出し、世界で最も宇宙支出が多い国となった。2022年には世界で180回のロケット打ち上げが成功し、そのうち76回は米国が打ち上げました。

- 例えば、2021年9月、米国の衛星製造会社Terran Orbitalは、フロリダのスペースコーストに3億米ドルを投じて世界最大の衛星製造・部品施設を開設すると発表しました。さらに2021年12月、レッドワイヤー・コーポレーションは衛星製造会社Terran Orbitalと3年間のサプライヤー契約を締結し、衛星製造やサービス提供に使用される様々な先端部品やソリューションを提供することになった。

衛星用コンポーネント業界の概要

衛星用コンポーネント市場は、一握りの企業が大きなシェアを占めており、適度に統合されています。著名な市場企業には、THALES、Viking Satcom、Lockheed Martin Corporation、Northrop Grumman Corporation、Honeywell International Inc.などがいます。競争の激化に伴い、主要な相手先商標製品メーカー(OEM)は、宇宙用途の高度な衛星用コンポーネントやシステムの設計・開発に注力しています。次世代衛星のアンテナ、中継器、推進システムなどの研究開発や設計開発への支出の増加は、今後数年間により良い機会を生み出すと思われます。

例えば、2021年10月、欧州宇宙機関(ESA)、フランスの宇宙機関CNES、衛星メーカーのThales Alenia Spaceは、軌道上の大型衛星の温度を維持する冷却システムを共同開発すると発表しました。大型商業通信衛星に使用される初の機械式ポンプループとなります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- コンポーネント

- アンテナ

- 電力システム

- 推進システム

- トランスポンダー

- その他のコンポーネント(センサー、熱制御システムなど)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Lockheed Martin Corporation

- Viking Satcom

- Sat-lite Technologies

- Honeywell International Inc.

- THALES

- Northrop Grumman Corporation

- IHI Corporation

- BAE Systems plc

- Challenger Communications

- JONSA TECHNOLOGIES CO., LTD.

- Accion Systems

第7章 市場機会と今後の動向

The Satellite Component Market size is estimated at USD 3.16 billion in 2024, and is expected to reach USD 4.37 billion by 2029, growing at a CAGR of 6.70% during the forecast period (2024-2029).

Key Highlights

- The global satellite component market has faced unprecedented challenges due to the COVID-19 pandemic. The space sector witnessed challenges such as shortages of raw materials, delayed satellite launch programs, and supply chain disruptions due to strict regulations imposed by governments. The market showcased a strong recovery after the pandemic. An increase in expenditure on the space sector and rising small satellite launches drive the market growth post-covid.

- The satellite components consist of the communications system, power systems, power systems, and others. The communication system includes antennas and transponders that receive and retransmit signals. The propulsion system consists of rockets that propel the satellite, and the power system includes solar panels that provide power. An increasing number of satellite launches and growing expenditure on the space sector drive the market growth. According to the United Nations Office for Outer Space Affairs (UNOOSA) index, in 2022, there were 8,261 individual satellites orbiting the Earth, with an increase of 11.84% compared to April 2021.

Satellite Component Market Trends

The Antenna Segment is Expected to Show Remarkable Growth During the Forecast Period

- The antenna segment is projected to show significant growth during the forecast period. The growth is due to increasing demand for advanced communication systems, rising number of satellite launches, and rising spending on the space sector. Satellite antennas are used to concentrate the satellite's transmitting power to the designated geographical region on Earth and avoid interference from undesired signals that will deteriorate the overall quality of the signal. Increasing satellite launches for various end-use applications such as communications, broadcasting, navigation, weather forecasting, and others drive the growth of the segment.

- The United Nations Office for Outer Space Affairs (UNOOSA) stated that 155 orbital and suborbital launches took place in November 2022. Moreover, in June 2022, the Satellite Industry Association (SIA) unveiled the 25th annual State of the Satellite Industry Report (SSIR). The report indicated a remarkable deployment of 1,713 commercial satellites in 2021, reflecting a notable surge of over 40 percent compared to 2020. This escalating demand for satellites is set to trigger a corresponding need for satellite components, thereby propelling market growth in the projected period. As an illustration, a significant development took place in July 2022 when MDA Ltd. entered into a contract with York Space Systems, a satellite manufacturer, to construct Ka-Band steerable antennas for satellites.

North America Held Highest Shares in the Market During the Forecast Period

- North America dominated the satellite components market and continued its domination during the forecast period. An increase in spending on space research and development and a rising number of satellite launches from the National Aeronautics and Space Administration (NASA) and SpaceX. In 2022, the United States government spent approximately USD 62 billion on its space programs and making the country with the highest space expenditure in the world. There were 180 successful rocket launches worldwide in 2022, out of which 76 were launched by the United States.

- For instance, in September 2021, Terran Orbital, a satellite manufacturing company in the United States, announced that it would open the world's largest satellite manufacturing and component facility on Florida's Space Coast at a cost of USD 300 million. Furthermore, in December 2021, Redwire Corporation signed a three-year supplier agreement with Terran Orbital, a satellite manufacturer, to provide a range of advanced components and solutions used in satellite manufacturing and service offerings.

Satellite Component Industry Overview

The satellite component market is moderately consolidated in nature, with a handful of players holding significant shares in the market. Some prominent market players are THALES, Viking Satcom, Lockheed Martin Corporation, Northrop Grumman Corporation, and Honeywell International Inc. With the growing competition, major original equipment manufacturers (OEMs) are focusing on the design and development of advanced satellite components and systems for space applications. Growing expenditure on research and development and design and development of next-generation satellite antennas, transponders, propulsion systems, and others will create better opportunities in the coming years.

For instance, in October 2021, the European Space Agency (ESA), French space agency CNES and Thales Alenia Space, a satellite manufacturer, announced it would jointly develop a cooling system that will maintain the temperature of big satellites in orbit. It will be the first mechanically pumped loop to be used on large commercial telecommunications satellites.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component

- 5.1.1 Antennas

- 5.1.2 Power Systems

- 5.1.3 Propulsion Systems

- 5.1.4 Transponders

- 5.1.5 Other Components (Sensors, Thermal Control Systems, etc)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lockheed Martin Corporation

- 6.1.2 Viking Satcom

- 6.1.3 Sat- lite Technologies

- 6.1.4 Honeywell International Inc.

- 6.1.5 THALES

- 6.1.6 Northrop Grumman Corporation

- 6.1.7 IHI Corporation

- 6.1.8 BAE Systems plc

- 6.1.9 Challenger Communications

- 6.1.10 JONSA TECHNOLOGIES CO., LTD.

- 6.1.11 Accion Systems