|

市場調査レポート

商品コード

1693816

電力機器- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Power Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電力機器- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

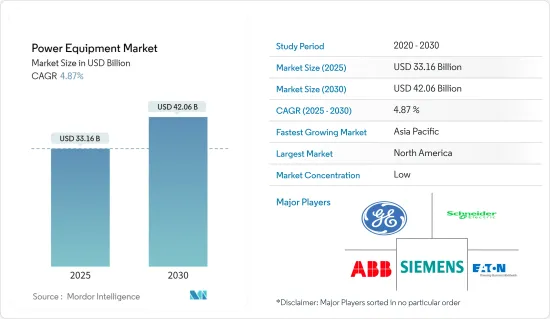

電力機器市場規模は2025年に331億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.87%で、2030年には420億6,000万米ドルに達すると予測されます。

COVID-19は2020年の市場にマイナスの影響を与えました。現在、市場は流行前の水準に達しています。

主要ハイライト

- 中期的には、人口増加とインフラ開発によるエネルギー需要の増加が見込まれ、その結果、予測期間中の電力機器需要が増加します。

- その一方で、高い運転・保守コストが市場成長の妨げになると予想されます。

- 再生可能エネルギーやスマートグリッドのインフラ開拓に向けた技術投資の増加は、電力機器市場に大きな機会をもたらすと予想されます。

電力機器市場の動向

発電が市場を独占する見込み

- 人口増加、都市化、工業化を背景に、世界の電力需要は増加しています。その結果、発電設備は、この増大する需要を満たし、安定した電力供給を確保する上で重要な役割を果たしています。

- さらに、太陽光発電、風力発電、水力発電、地熱発電といった再生可能エネルギー発電への注目が高まっていることも、発電設備の優位性を高めています。よりクリーンでサステイナブルエネルギーへの移行には、ソーラーパネル、風力タービン、水力発電機のような特殊な発電設備が必要です。

- 例えば、2022年6月、ヴェスタスASは、EnBWの900MW He Dreiht洋上風力発電プロジェクト向けに64基のV235-15.0MW風力タービンを供給する契約を獲得しました。ヴェスタスはまた、2025年第2四半期に開始が予定されているタービンの輸送と設置に関して、Cadelerと契約を締結しました。

- 世界各国の政府も施策、インセンティブ、再生可能エネルギー発電目標を実施しており、特に再生可能エネルギーセグメントの発電設備需要をさらに押し上げています。

- このため、再生可能エネルギーの設備容量は世界的に増加しています。国際再生可能エネルギー機関によると、2021年の3,077.23GWに対し、2022年の世界の再生可能エネルギー設備容量は3,371.8GWであり、2021~2022年にかけて9.5%以上の成長率を記録しています。

- したがって、エネルギー需要の増加、再生可能エネルギーへの注目、政府の取り組み、発電により、発電は電力機器市場の中で支配的なセグメントとして浮上しています。

アジア太平洋が著しい成長を遂げる

- アジア太平洋には、世界人口のかなりの割合が集中しており、数多くの大都市があります。今後数年間で、この地域は数百万人の新規顧客の間で電力へのアクセスが拡大するため、電力需要が急増すると予想されます。この需要急増は、急速な人口増加と工業化の進行に起因しています。

- アジア太平洋は、近い将来、電力機器の有力な市場として台頭してくるものと考えられます。主要原動力は、再生可能エネルギー源の使用の増加、電力消費の増加、電力へのアクセスの増加、送電網インフラの継続的な改善です。中国、インド、日本、オーストラリアなどの主要国は、この地域の電力機器市場の形成に極めて重要な役割を果たすと予想されています。

- BP Statistical Review of World Energyによると、2021年の同地域の発電量は13,994.4 TWhで、2020年比で8.4%、2011~2021年の間で4.7%増加しました。

- さらに、同地域の政府は、発電・配電インフラに有利な施策、イニシアティブ、投資を実施することで、重要な役割を果たしています。このようなエネルギー安全保障、再生可能エネルギー促進、電力アクセス改善への取り組みは、アジア太平洋の電力機器需要をさらに促進しています。

- 例えば、中国政府は2022年、ゴビ砂漠地帯に総容量450ギガワットの太陽光発電所と風力発電所を建設するという野心的な計画を発表しました。この構想は、2030年までの再生可能エネルギー目標達成に向けて国を推進することを目的としています。

- こうした進歩は、効率的でサステイナブル電力管理を可能にし、電力機器市場における同地域の優位性を高めています。

- アジア太平洋は、急速な経済成長、都市化、政府のイニシアティブ、再生可能エネルギーの導入、インフラ開拓、産業需要、技術の進歩により、電力機器市場を独占する態勢を整えています。

電力機器産業概要

世界の電力機器市場は半固体化しています。この市場の主要企業(順不同)には、General Electric Company、Schneider SE、ABB、Eaton Corporation、Siemensなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 人口増加とインフラ開発

- 抑制要因

- 高い運用・保守コスト

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 設備タイプ

- 発電機

- 変圧器

- 開閉装置

- サーキットブレーカー

- 電力ケーブル

- その他の機器

- 発電源

- 化石燃料ベース

- 太陽熱

- 風力

- 原子力

- 水力

- エンドユーザー

- 住宅用

- 産業・商業

- 公益事業

- 用途

- 発電

- 送電

- 配電

- 地域、2028年までの市場規模・需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- General Electric Company

- Siemens AG

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Eaton Corporation plc

- Toshiba Corporation

- Honeywell International Inc.

- Bharat Heavy Electricals Limited

- Crompton Greaves Ltd.

- Larsen & Toubro Limited

- Fuji Electric Co., Ltd.

- Rockwell Automation, Inc.

- ABB Ltd.

第7章 市場機会と今後の動向

- 再生可能エネルギーとスマートグリッドインフラ開発への技術投資の増加

The Power Equipment Market size is estimated at USD 33.16 billion in 2025, and is expected to reach USD 42.06 billion by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020. Presently, the market has reached pre-pandemic levels.

Key Highlights

- Over the medium term, increasing population growth and infrastructure development are expected to increase energy demand, consequently increasing the demand for power equipment during the forecasted period.

- On the other hand, high operations and maintenance costs are expected to hinder market growth.

- Nevertheless, the increasing technological investments in developing renewable energy and smart grid infrastructure are expected to create huge opportunities for the power equipment market.

Power Equipment Market Trends

Power Generation Expected to Dominate the Market

- The global electricity demand is rising, driven by population growth, urbanization, and industrialization. As a result, power generation equipment plays a critical role in meeting this escalating demand and ensuring a consistent electricity supply.

- Moreover, the expanding focus on renewable energy sources, such as solar, wind, hydro, and geothermal power, further contributes to the dominance of power generation equipment. The transition towards cleaner and more sustainable energy necessitates specialized power generation equipment like solar panels, wind turbines, and hydroelectric generators.

- For instance, in June 2022, Vestas AS won a contract to supply 64 V235-15.0 MW wind turbines for EnBW's 900 MW He Dreiht offshore wind project. Vestas has also entered into an agreement with Cadeler for the transportation and installation of the turbines, which is planned to start in Q2 2025.

- Governments worldwide are also implementing policies, incentives, and renewable energy targets, further boosting the demand for power generation equipment, particularly in the renewable energy sector.

- This has led to an increase in renewable energy installed capacity globally. According to the International Renewable Energy Agency, in 2022 the global renewable energy installed capacity was 3371.8 GW, compared to 3077.23 GW in 2021, registering a growth rate of more than 9.5% between 2021 and 2022.

- Therefore, with increasing energy demand, the focus on renewable energy, government initiatives, and power generation, power generation emerges as the dominant segment within the power equipment market.

Asia-Pacific to Witness Significant Growth

- Asia-Pacific houses a significant proportion of the global population and has numerous major cities. In the coming years, the region is expected to witness a surge in power demand due to the expanding access to electricity among millions of new customers. This escalating demand can be attributed to rapid population growth and the ongoing process of industrialization.

- The Asia-Pacific region is poised to emerge as a prominent market for power equipment in the foreseeable future. The main drivers are the increasing use of renewable energy sources, rising power consumption, increased access to electricity, and ongoing improvements to power grid infrastructure. Key countries such as China, India, Japan, and Australia are anticipated to play pivotal roles in shaping the power equipment market within the region.

- According to the BP statistical review of world energy, the electricity generation in the region was 13,994.4 TWh in 2021, an increase of 8.4% compared to 2020 and 4.7% between 2011 and 2021.

- Additionally, governments in the region are playing a crucial role by implementing favorable policies, initiatives, and investments in power generation and distribution infrastructure. This commitment to energy security, renewable energy promotion, and improved electricity access further propel the demand for power equipment in Asia-Pacific.

- For instance, the Chinese government unveiled its ambitious plan in 2022 to construct solar and wind energy power plants with a total capacity of 450 gigawatts in the Gobi desert regions. This initiative aims to propel the nation towards achieving its renewable energy target by 2030.

- These advancements enable efficient and sustainable power management, enhancing the region's prominence in the power equipment market.

- Asia Pacific is therefore poised to dominate the power equipment market due to rapid economic growth, urbanization, government initiatives, the deployment of renewable energy sources, infrastructure development, industrial demand, and technological advancements.

Power Equipment Industry Overview

The global power equipment market is semi-consolidted. Some of the key players in this market (in no particular order) are General Electric Company, Schneider SE, ABB Ltd., Eaton Corporation, and Siemens AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Population Growth and Infrastructure Development

- 4.5.2 Restraints

- 4.5.2.1 High Operational and Maintenance Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment Type

- 5.1.1 Generator

- 5.1.2 Transformer

- 5.1.3 Switchgears

- 5.1.4 Circuit Breakers

- 5.1.5 Power Cable

- 5.1.6 Other Equipment Types

- 5.2 Power Generation Source

- 5.2.1 Fossil Fuel Based

- 5.2.2 Solar

- 5.2.3 Wind

- 5.2.4 Nuclear

- 5.2.5 Hydro

- 5.3 End-User

- 5.3.1 Residential

- 5.3.2 Industrial and Commercial

- 5.3.3 Utility

- 5.4 Application

- 5.4.1 Power Generation

- 5.4.2 Transmission

- 5.4.3 Distribution

- 5.5 Geography [Market Size and Demand Forecast till 2028 (for regions only)]

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Australia

- 5.5.3.4 Japan

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Nigeria

- 5.5.4.4 South Africa

- 5.5.4.5 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Chile

- 5.5.5.4 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 General Electric Company

- 6.3.2 Siemens AG

- 6.3.3 Schneider Electric SE

- 6.3.4 Mitsubishi Electric Corporation

- 6.3.5 Eaton Corporation plc

- 6.3.6 Toshiba Corporation

- 6.3.7 Honeywell International Inc.

- 6.3.8 Bharat Heavy Electricals Limited

- 6.3.9 Crompton Greaves Ltd.

- 6.3.10 Larsen & Toubro Limited

- 6.3.11 Fuji Electric Co., Ltd.

- 6.3.12 Rockwell Automation, Inc.

- 6.3.13 ABB Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Technological Investments in Developing Renewable Energy and Smart Grid Infrastructure