|

市場調査レポート

商品コード

1693729

飼料用香料・甘味料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Feed Flavors And Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飼料用香料・甘味料:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 291 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

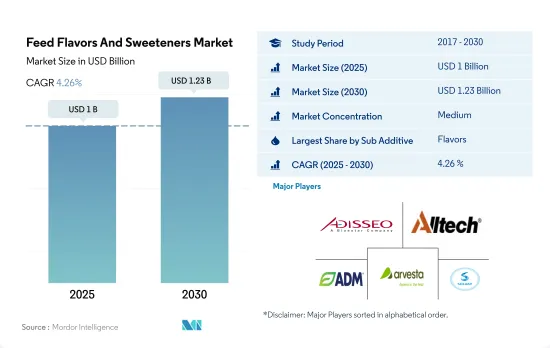

飼料用香料・甘味料の市場規模は2025年に10億米ドルと推定され、2030年には12億3,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは4.26%で成長する見込みです。

- 動物飼料市場は、牛や豚の飼料摂取量を増やすのに役立つ香料や甘味料の需要が牽引しています。これらの動物には多くの味蕾があるため、フレーバーと甘味料の使用は成長と健康に不可欠です。

- フレーバーは甘味料よりも市場シェアが6.4%高く、家畜の利得を18%、飼料効率を7.7%向上させることができるからです。北米は最も急成長している市場であり、予測期間中にCAGR 5.6%を記録すると予想されます。この成長は、米国やカナダなどの国々における飼料摂取量の多さと、飼料工場の増加によってもたらされると考えられます。飼料工場の増加により、2019~2022年の飼料生産量は9.8%増加しました。

- アジア太平洋は最大の市場シェア、すなわち2022年に約30.8%を占めたが、これは中国の食品産業における豚肉と牛肉の需要が高く、動物人口と飼料生産が増加したためです。フレーバーは市場で最も急成長しているセグメントであり、豚の頭数の増加に牽引され、予測期間中にCAGR 4.2%を記録すると予想されます。フレーバーは飼料効率の向上、疾病の回避、嗜好性の改善、飼料摂取量の増加に役立ちます。

- 中国やインドなどの国々は反芻動物の数が多いです。これらの国々はアジア太平洋の反芻動物人口の約57.5%を占めています。この地域では反芻動物用飼料の需要が高く、予測期間中にCAGR 4.7%で反芻動物用フレーバーと甘味料の成長を後押しする可能性があります。

- 豚と反芻動物用飼料需要が高く、動物飼料の嗜好性を向上させる必要性があることから、予測期間中の市場の成長が見込まれます。

- アジア太平洋は飼料用香料・甘味料の最大市場であり、2022年には市場の30.8%を占めます。この地域は、気温の上昇や飼料配合の変更といった課題に直面しており、その結果、動物が消費する飼料量が減少しているため、香料・甘味料の使用が促進されています。

- 北米は2022年の飼料用香料・甘味料市場の25.9%を占め、世界第2位の市場となっています。2017~2022年の同市場の成長は、動物用飼料摂取量と飼料転換率の向上という利点に加え、スクロースやサッカリンなどの甘味料を使用することで、快感ホルモンを増加させて動物のストレスを軽減することに起因しています。

- 米国は、飼料用香料・甘味料の最大市場です。2022年のシェアは18.1%、次いで中国が13.9%です。これらの国の市場シェアが大きいのは、動物の頭数が多く、一人当たりの食肉消費量が多いためと考えられます。

- チリ、インド、英国は急成長国であり、予測期間中にそれぞれ4.9%、4.7%、4.7%のCAGRで推移すると予想されます。欧州では、スペインが最大の市場シェアを占めています。飼料生産の増加と良質な畜産物への高い需要により、予測期間中のCAGRは4.0%を記録すると予想されます。

- 飼料用香料・甘味料市場は、飼料生産の増加と高品質の牛肉、豚肉、豚肉と反芻動物製品の需要による飼料用香料・甘味料需要の高まりにより、予測期間中にCAGR 4.2%を記録すると予測されます。

世界の飼料用香料・甘味料市場の動向

牛肉消費の増加、飲食品部門の成長、農場数の増加が世界の反芻動物生産を牽引

- 世界の乳製品市場は、人口増加、健康志向の高まり、飲食品産業の成長、新興市場の需要増加、付加価値など様々な要因によって牽引されています。中国における肉牛1頭の飼育の収益性は、2019~2020年にかけて75%以上上昇し、1頭当たりの平均純利益は441米ドルとなりました。インドは世界有数の牛の生産国で、2017~2022年の間に牛と水牛の生産頭数は3億120万頭から3億730万頭に増加します。乳製品需要の増加と消費者所得の増加、健康に対する意識の高まりが反芻動物生産の成長を促進しています。

- 牛肉消費の増加と牛飼育の収益性上昇により、肉牛農場の数が増加しています。カナダでは2021年に農場数が2016年から10.1%増加しました。羊とヤギの飼育も、需要増加による収益性の向上により、この地域で増加しています。ヒツジとヤギの生産量は2017~2022年の間に2億1,350万頭から2億2,350万頭に増加しました。アジア太平洋は世界のヤギの40.8%以上を占め、中国、インド、パキスタン、バングラデシュ、モンゴルが主要国です。羊の場合は、中国、インド、イラン、モンゴル、トルコが市場を独占しています。

- 肉牛については、飼育の収益性が飼料添加物市場の成長を牽引しており、羊とヤギについては、需要の高まりがこれらのセグメントの生産と利益を押し上げています。

米国が肉牛生産の80%を輸出しているアジア太平洋と北米における反芻動物用飼料の高い需要、インドにおける新しいミルク供給業者の出現

- 反芻家畜用飼料の主要消費地域はアジア太平洋と北米です。これは、高品質の肉に対する需要の増加、農場の生産性への注目の高まり、栄養価の高い飼料の給与による収益性の向上による。乳牛用の飼料生産は、乳量を増やし乳中の脂肪含量を改善するための配合飼料のニーズの高まりにより、2017~2022年の間に6.7%の成長を示しました。乳価の上昇や、インドにおけるCountry DelightやHappy Nature(DHA Agritech Pvt.Ltd.)といった新しいミルク供給業者の出現も、飼料需要を増加させています。

- 肉牛用飼料の需要は2017~2022年にかけて45.1%増加したが、これは栄養価の高い飼料が収量向上に有利であることや、中国や米国などの国々で肉牛肉の需要が高いことから、生産者が栄養バランスの取れた配合飼料の給与を増やしたためです。2021年、米国は牛肉の約80%を日本、韓国、中国、メキシコ、カナダの5カ国に輸出しました。ミルク、肉、皮の需要が高いため、ヤギ飼育の人気も高まっています。ヤギを含むその他の反芻動物用の配合飼料生産量は、飼料消費の増加により2017~2022年にかけて2.2%増加しました。

- 健康的な飼料に対する意識の高まりと、牛乳や牛肉をベースとした製品の需要が、反芻動物用飼料生産の増加に寄与しています。飼料製造業者は予測期間中に反芻動物用の飼料生産を増加させると予想されます。

飼料用香料・甘味料産業概要

飼料用香料・甘味料市場は適度に統合されており、上位5社で48.26%を占めています。この市場の主要企業は、Adisseo、Alltech、Inc.、Archer Daniel Midland Co.、Arvesta(Palital Feed Additives B.V)and Solvay S.A.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 動物頭数

- 反芻動物

- 養豚

- 飼料生産量

- 反芻動物

- 豚

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ添加物

- 香料

- 甘味料

- 動物

- 水産養殖

- サブ動物別

- 魚類

- エビ

- その他の養殖種

- 家禽類

- 小動物別

- ブロイラー

- レイヤー

- その他の鳥類

- 反芻動物

- 小動物別

- 肉牛

- 乳牛

- その他の反芻動物

- 豚

- その他の動物

- 水産養殖

- 地域

- アフリカ

- 国別

- エジプト

- ケニア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- フィリピン

- 韓国

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

- 中東

- 国別

- イラン

- サウジアラビア

- その他の中東

- 北米

- 国別

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- 国別

- アルゼンチン

- ブラジル

- チリ

- その他の南米諸国

- アフリカ

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Adisseo

- Alltech, Inc.

- Archer Daniel Midland Co.

- Arvesta(Palital Feed Additives B.V)

- Biovet S.A.

- Innov Ad NV/SA

- PhytobIoTics Futterzusatzstoffe GmbH

- Prinova Group LLC

- Solvay S.A.

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 93763

The Feed Flavors And Sweeteners Market size is estimated at 1 billion USD in 2025, and is expected to reach 1.23 billion USD by 2030, growing at a CAGR of 4.26% during the forecast period (2025-2030).

- The animal feed market is driven by the demand for flavors and sweeteners, which help increase the feed intake of cattle and swine. These animals have many taste buds, making the use of flavors and sweeteners essential for their growth and well-being.

- Flavors have a higher market share of 6.4% than sweeteners as they can improve gains for animals by 18% and feed efficiency by 7.7%. North America is the fastest-growing market, and it is expected to register a CAGR of 5.6% during the forecast period. This growth is likely to be driven by high feed intake in countries such as the United States and Canada and an increase in the number of feed mills. The rise in feed mills led to a 9.8% increase in feed production during 2019-2022.

- Asia-Pacific held the largest market share, i.e., about 30.8% in 2022, owing to the high demand for pork and beef in the Chinese food industry, which increased the animal population and feed production. Flavors are the fastest-growing segment in the market, and it is expected to register a CAGR of 4.2% during the forecast period, driven by the rising swine population. Flavors help increase feed efficiency, avoid diseases, improve palatability, and boost feed intake.

- Countries such as China and India have large ruminant populations. These countries accounted for about 57.5% of the Asia-Pacific ruminant population. There is high demand for ruminant feed in the region, which may boost the growth of flavors and sweeteners for ruminants at a CAGR of 4.7% during the forecast period.

- The high feed demand for swine and ruminants and the need to improve the palatability of animal feed are expected to drive the market's growth during the forecast period.

- Asia-Pacific is the largest market for feed flavors and sweeteners, accounting for 30.8% of the market in 2022. The region has been facing challenges such as rising temperatures and changes in feed formulation, which have resulted in animals consuming less feed, thus boosting the use of flavors and sweeteners.

- North America accounted for 25.9% of the feed flavors and sweeteners market in 2022, making it the second-largest market globally. The growth of the market during 2017-2022 was attributed to the benefits of enhanced feed intake and feed conversion in animals, as well as the use of sweeteners, such as sucrose or saccharin, to reduce stress in animals by increasing the number of feel-good hormones.

- The United States is the largest market in terms of feed flavors and sweeteners. It accounted for an 18.1% share in 2022, followed by China with 13.9%. The large market shares of these countries could be attributed to the presence of a high animal headcount and high per capita meat consumption.

- Chile, India, and the United Kingdom are the fastest-growing countries, and they are expected to register CAGRs of 4.9%, 4.7%, and 4.7%, respectively, during the forecast period. In Europe, Spain holds the largest market share. It is expected to register a CAGR of 4.0% during the forecast period due to the increase in feed production and high demand for good quality animal products.

- The feed flavors and sweeteners market is anticipated to register a CAGR of 4.2% during the forecast period, driven by the rising demand for feed flavors and sweeteners due to increased feed production and demand for high-quality beef, pork, and swine and ruminant products.

Global Feed Flavors And Sweeteners Market Trends

Increased consumption of beef meat, growing food and beverage sector, and increasing number of farms are driving the global ruminants production

- The global dairy market is being driven by various factors, including population growth, rising health consciousness, growth in the food and beverage industry, increasing demand from emerging markets, and value addition. The profitability of raising a single beef cow in China increased by more than 75% in 2020 from 2019, with an average net profit of USD 441.0 per cow. India is the leading producer of cattle globally, with the production of cattle and buffaloes increasing from 301.2 million heads to 307.3 million heads between 2017 and 2022. The rise in demand for dairy products, coupled with the increasing consumer income and awareness about health, is driving the growth of ruminant production.

- The increasing consumption of beef and the rising profitability of raising cattle have increased the number of beef cattle farms. In Canada, the number of farms increased by 10.1% in 2021 from 2016. Sheep and goat rearing is also increasing in the region, owing to increasing profits due to the rising demand. The production of sheep and goats increased from 213.5 million heads to 223.5 million heads between 2017 and 2022. The Asia-Pacific region accounted for more than 40.8% of the global goat population, with China, India, Pakistan, Bangladesh, and Mongolia being the major countries. In the case of sheep, China, India, Iran, Mongolia, and Turkey dominate the market.

- The profitability of raising cattle is driving the growth of the feed additives market in terms of beef cattle, and the rising demand for sheep and goats is boosting production and profits in these sectors.

High demand for ruminants feed in Asia-Pacific and North America with the United States exported 80% of beef production and emergence of new milk providers in India

- The primary consumers of ruminant feed production in terms of regions are Asia-Pacific and North America, owing to the increased demand for high-quality beef meat, increased focus on farm productivity, and profitability through feeding of nutritional feed. Feed production for dairy cattle witnessed a growth of 6.7% between 2017 and 2022 due to the rising need for compound feed to increase the yield and improve the fat content in the milk. The increasing milk prices and the emergence of new milk providers, such as Country Delight and Happy Nature (DHA Agritech Pvt. Ltd) in India, have also increased the demand for feed.

- The demand for beef cattle feed increased by 45.1% between 2017 and 2022 as producers increased the feeding of nutritionally balanced compound feed due to the advantages of nutrient-rich feed in yield enhancement and the high demand for beef meat in countries such as China and the United States. In 2021, the United States exported about 80% of beef meat to five countries, including Japan, South Korea, China, Mexico, and Canada. The popularity of goat farming has also increased due to the high demand for milk, meat, and skin. Compound feed production for other ruminants, including goats, increased by 2.2% from 2017 to 2022 due to the increase in feed consumption.

- Increased awareness about healthy feed and the demand for milk and beef-based products have contributed to increasing ruminant feed production. Feed millers are expected to increase feed production for ruminants during the forecast period.

Feed Flavors And Sweeteners Industry Overview

The Feed Flavors And Sweeteners Market is moderately consolidated, with the top five companies occupying 48.26%. The major players in this market are Adisseo, Alltech, Inc., Archer Daniel Midland Co., Arvesta (Palital Feed Additives B.V) and Solvay S.A. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Ruminants

- 4.1.2 Swine

- 4.2 Feed Production

- 4.2.1 Ruminants

- 4.2.2 Swine

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Additive

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Kenya

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 South Korea

- 5.3.2.1.8 Thailand

- 5.3.2.1.9 Vietnam

- 5.3.2.1.10 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Chile

- 5.3.6.1.4 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Adisseo

- 6.4.2 Alltech, Inc.

- 6.4.3 Archer Daniel Midland Co.

- 6.4.4 Arvesta (Palital Feed Additives B.V)

- 6.4.5 Biovet S.A.

- 6.4.6 Innov Ad NV/SA

- 6.4.7 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.8 Prinova Group LLC

- 6.4.9 Solvay S.A.

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms