|

市場調査レポート

商品コード

1431021

世界の疼痛管理装置:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Pain Management Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の疼痛管理装置:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 113 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

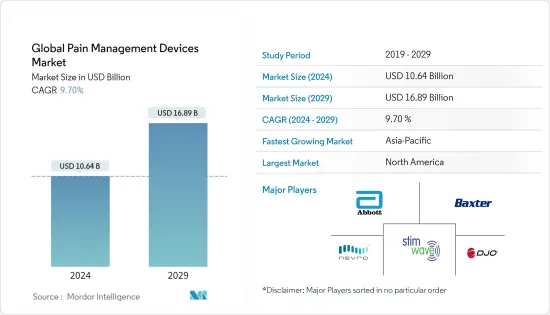

世界の疼痛管理装置の市場規模は、2024年に106億4,000万米ドルと推定され、2029年までには168億9,000万米ドルに達すると予測され、予測期間中(2024年~2029年)のCAGRは9.70%で成長する見込みです。

COVID-19パンデミックは当初、疼痛管理装置市場に大きな影響を与えました。政府によるロックダウンと厳格な法律が疼痛管理装置市場の成長に影響を与えました。いくつかの予期せぬ理由により、この市場の成長はCOVID-19の初期段階で大きく抑制されました。しかし、輸液予約の大幅な増加や、疼痛管理装置の市場を世界的に拡大させたアブレーション処置により、市場は牽引力を得ました。また、疼痛管理装置の多くは緊急性が低いと判断され、さらに政府による厳格なロックダウンのために外来患者や介入処置がすべて縮小されたため、疼痛管理装置市場は大きな影響を受けました。

COVID-19症例の大幅な増加も、間接的に全世界で痛みに苦しむ患者数を増加させました。筋痛、背部痛、頭痛など、COVID-19の最初の症状は痛みであると報告されています。例えば、『Best Practice and Research in Clinical Anaesthesiology』2020年7月号は、COVID-19患者の大半が筋骨格系、背部痛、頭痛を症状として持っていたと報告しています。また、Scientific Reportsによれば、COVID後の疼痛スコアは10段階で6に増加し、COVID前は10段階で5であったといいます。COVID-19に関連する疼痛を管理し克服するために、人々は医薬品よりも疼痛管理装置の方を選ぶようになり、その結果、ヘルスケア業界は疼痛管理装置の製造を増加させ、この市場を牽引しています。

また、がんや心血管疾患などの慢性疾患の増加も、疼痛管理装置の普及を後押しし、疼痛管理装置市場を牽引しています。例えば、世界保健機関が発表したデータによると、2020年には約1,000万人ががんで死亡したと報告されました。がんの罹患率は過去数年間で劇的に上昇しており、この病気の症状として関連する慢性疼痛も増加しているため、疼痛管理装置市場を直接牽引しています。

疼痛管理装置のひとつである疼痛制御鎮痛(PCA)ポンプは、脊椎手術やいくつかの重要な関節手術に伴う痛みを克服するため、術後の疼痛管理に使用されます。例えば、国立脊髄損傷統計センター(NSCISC)の2021年データシートは、脊髄損傷の年間発生率を100万人当たり60件としています。このような症例の増加や外科手術の増加に伴い、輸液ポンプやPCAポンプの需要が大幅に増加し、疼痛管理装置市場を牽引しています。

したがって、前述の要因により、この市場は分析期間中に成長すると予想されます。しかし、認知度の低さから、疼痛管理装置よりも疼痛管理薬を好む患者はまだ少なく、これが疼痛管理装置市場の抑制要因となっている可能性があります。また、これらの装置は痛みを克服するための第二選択治療の治療に使用されており、これもこの市場の課題となっています。

疼痛管理装置市場の動向

神経障害性疼痛管理装置分野は世界市場で最大のシェアを占め、著しい成長を遂げる

神経障害性疼痛は、神経系が損傷を受けたり、正常に機能していない場合に発生します。神経障害性疼痛管理装置分野は、この疼痛管理装置市場で優位性を示しています。神経障害性疼痛管理装置の成長は、神経障害性疼痛の有病人口の増加に起因しています。例えば、疾病管理センター(Centers for Disease Control and Center, 2021)は、成人の約5人に1人が神経因性疼痛に苦しんでいると報告しています。神経因性疼痛を扱う人口の発生率の増加によるものです。

COVID-19の症例の増加は、神経障害性疼痛を含む慢性疼痛の症状の増加を目の当たりにしました。例えば、学術誌『Pain Reports 2021』に掲載された「COVID-19パンデミック後の神経障害性疼痛の有病率増加の可能性」と題された論文では、COVID-19は神経障害性疼痛の末梢または中枢神経合併症も引き起こすと述べられています。特にギラン・バレー症候群、脊髄炎、脳卒中を含むCOVID-19の合併症の増加が、慢性神経障害性疼痛の潜在的リスクに関してレビューされています。COVID-19後の慢性神経障害性疼痛の有病率の増加は、市場成長を後押しするもう一つの理由です。

従来の疼痛管理療法には薬物療法がありますが、薬物療法には副作用が伴うため、神経障害性疼痛を克服するために神経刺激疼痛管理装置へと移行しつつあります。このような理由から、神経障害性疼痛管理装置分野がこの疼痛管理装置分野で最大のシェアを占めています。

北米が疼痛管理装置市場を独占する見込み

北米は疼痛管理装置市場を独占してきましたが、先進技術の存在、主要な市場プレーヤー、外来センターにおける疼痛管理装置の大規模な導入により、今後もこの市場を独占すると予想されます。

米国は、痛みに苦しむ人の数が増加しています。例えば、Journal of Pain and Palliative Therapy, 2021によると、米国人口の約20.28%が慢性疼痛に苦しんでおり、このうち5%は影響の大きい慢性疼痛に苦しむ成人です。そのため、米国では慢性疼痛を患う人口が増加しており、疼痛管理装置市場を急速に牽引しています。また、米国では神経障害性疼痛の有病率が高く、慢性疾患の罹患率が高いことが報告されているため、同国の人口は医薬品よりも疼痛管理装置に依存しています。例えば、Pain Medicineの記事によると、米国人口の約2%が神経障害性疼痛に苦しんでいます。また、International Journal of Environmental Health and Public Resource誌(2021年)の記事によると、北米では慢性疾患の有病率が高いため、アメリカ人全体の約45%(1億3,300万人)が少なくとも1つの慢性疾患に苦しんでいます。痛みに苦しむ患者の増加は、市場の成長を促進します。

高い成長の可能性、患者ベースの人口の大幅な増加、高い可処分所得により、疼痛管理装置市場の需要は予測期間中に増加すると予想されます。

疼痛管理装置産業の概要

疼痛管理装置市場は、世界的および地域的に事業を展開する複数の企業が存在するため、その性質上断片化されています。既存の主要企業は、Abbott lab、AstraZeneca PLC、Baxter International Inc、DJO Global LLC、SPR Therapeutics、Stim Wave LLC、LivaNova、Nevro Corp、Innovis、ICU Medical Incなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 革新的で技術的に高度な疼痛管理装置の登場

- 疼痛管理装置の採用増加

- 高齢者人口の増加

- 市場抑制要因

- 疼痛管理のための薬剤の優先的使用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模:金額ベース)

- 製品タイプ別

- 神経刺激装置

- 輸液ポンプ

- アブレーション装置

- 用途別

- 筋骨格系

- がん性疼痛

- 神経障害性疼痛

- 顔面痛および片頭痛

- その他

- エンドユーザー別

- 理学療法センター

- 病院・クリニック

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic

- Boston Scientific Corporation

- Stryker

- Stim Wave LLC

- ICU Medical Inc

- Enovis

- Baxter

- LivaNova

- Abbott

- DJO Global LLC

- SPR Therapeutics

- Nevro Corp

第7章 市場機会と今後の動向

The Global Pain Management Devices Market size is estimated at USD 10.64 billion in 2024, and is expected to reach USD 16.89 billion by 2029, growing at a CAGR of 9.70% during the forecast period (2024-2029).

COVID-19 pandemic has had a substantial impact on the pain management devices market initially. The lockdown and strict laws imposed by the government impacted the growth of the pain management devices market.Due to some unforeseen reasons, the growth of this market was severely obstructed during the initial COVID-19 phase. However, the market gained traction due to the significant increase in infusion appointments, and ablation procedures which increased the market for pain management devices globally. Also, most of the pain management devices were deemed to be not so urgent, also all the outpatient and interventional procedures were reduced due to the strict lockdown imposed by the government, and thus the pain management device market was greatly impacted.

A significant increase in COVID-19 cases had also indirectly increased the number of patients suffering from pain worlwide. It was reported that pain was the first symptom of COVID-19, including myalgias, back pain, and headache. For instance, Best Practice and Research in Clinical Anaesthesiology, July 2020, reported that the majority of the COVID-19 patients had musculoskeletal, back pain, and headaches as a symptom. In another instance, the journal Scientific Reports, states that post-covid pain scores increased to 6 on a 10 scale as compared to pre-covid which was 5 on a 10. To manage and overcome the pain associated with COVID-19, people were more drifted towards pain management devices rather than medicines due to their less severe effects which subsequently led the healthcare industry to increase the manufacture of the pain management devices, which has driven this market.

The rise in cases of chronic diseases such as cancer and other cardiovascular diseases also boosted these devices to manage pain well, which has driven the pain management devices market. For instance, as per the data published by World Health Organization about 10 million deaths due to cancer were reported in 2020. The incidence of cancer is rising dramatically over the past few years and chronic pain associated as a symptom of this disease is also increasing, which is directly driving the pain management devices market.

One of the pain management device, pain controlled analgesia (PCA) pumps, are used to manage post-operative pain to overcome the pain associated with spine surgeries and some critical joint surgeries. For instance, National Spinal Cord Injury Statistical Center (NSCISC) 2021 datasheet has accounted the annual incidence of spinal cord injuries at 60 cases per million. With the increasing number of these cases, and a number of surgical procedures performed the demand for infusion and PCA pumps has significantly increased and thus has driven the pain management devices market.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period. However, still few patients prefer pain management drugs over devices due to a lack of awareness which may cause hindrance to the management devices market. Also, these devices are used for the treatment of second-line of therapy to overcome pain, which is another challenge for this market.

Pain Management Devices Market Trends

The neuropathic pain management devices segment counted for the largest share of the global market and witness significant growth

Neuropathic pain can happen if the nervous system is damaged or not working correctly. The neuropathic pain management device segment has witnessed dominance in this pain management devices market. The growth of neuropathic pain management devices has increased attributed due to the increase in the prevalence population of neuropathic pain. For instance, the Centers for Disease Control and Center, 2021 reports that about one in five adults suffers from neuropathic pain. Due to an increase in the incidence rate of the population dealing with neuropathic pain

The increase in cases of COVID-19 had witnessed an increase in the symptoms of chronic pain including neuropathic pain. For instance, the article titled 'Potential for the increased prevalence of neuropathic pain after the COVID-19 pandemic' in the journal Pain Reports 2021, states that COVID-19 also causes peripheral or central neurological complications of neuropathic pain. Increased complications of COVID-19 including in particular Guillain-Barre syndrome, myelitis, and stroke are reviewed with regards to their potential risk of chronic neuropathic pain. This increase in the prevalence of chronic neuropathic pain after COVID-19 is another reason boosting the market growth.

Traditional therapy for pain management includes drugs and medicine, but due to the side effects associated with drugs, people are shifting towards neurostimulation pain management devices to overcome neuropathic pain. Thus because of the above-mentioned reasons neuropathic pain management devices segment is witnessing the largest share in this pain management devices segment.

North America is Expected to Dominate the Pain Management Devices Market

North America has dominated the pain management devices market and is expected to dominate this market due to the presence of advanced technology, key market players, and the large incorporation of pain management devices in ambulatory centers.

The United States accounts for the increasing number of individuals suffering from pain. For instance, the Journal of Pain and Palliative Therapy, 2021 accounts that approximately 20.28% of the United States population is suffering from chronic pain and 5% of this population comprises adults who are suffering from high-impact chronic pain. Therefore, with the increasing prevalence of the population suffering from chronic pain in the United States rapidly drives its market for pain management devices. Also due to the high prevalence of neuropathic pain and higher incidence of the chronic disease reported in the United States, the population there is more dependent on pain management devices rather than on medicines. For instance, according to an article in the journal Pain Medicine, about 2% of the United States population suffers from neuropathic pain. Additionally, as the article in journal International Journal of Environmental Health and Public Resource, 2021 mentioned that approximately 45%, (or 133 million) of all Americans suffer from at least one chronic disease thus due to the high prevalence of population in North America suffering from chronic diseases. The increase in patient population suffering from pain will in turn propel the market growth.

Due to high growth potential, a significant increase in the patient base population, and high disposable income the demand of the pain management devices market is expected to increase during the forecast period.

Pain Management Devices Industry Overview

The pain management devices market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The existing key players in the market are Abbott lab, AstraZeneca PLC, Baxter International Inc, DJO Global LLC, SPR Therapeutics, Stim Wave LLC, LivaNova, Nevro Corp, Innovis, ICU Medical Inc, and other prominent players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The advent of Innovative and Technologically Advanced Pain Management Devices

- 4.2.2 Increase in Adoption of Pain Management Devices

- 4.2.3 Rise in Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Preferable use of medications for pain management

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION( Market Size by Value)

- 5.1 By Product Type

- 5.1.1 Neurostimulation Devices

- 5.1.2 Infusion Pumps

- 5.1.3 Ablation Devices

- 5.2 By Application

- 5.2.1 Musculoskeletal

- 5.2.2 Cancer Pain

- 5.2.3 Neuropathic Pain

- 5.2.4 Facial Pain and Migraine

- 5.2.5 Other

- 5.3 By End-User

- 5.3.1 Physiotherapy Centers

- 5.3.2 Hospitals and Clinics

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Stryker

- 6.1.4 Stim Wave LLC

- 6.1.5 ICU Medical Inc

- 6.1.6 Enovis

- 6.1.7 Baxter

- 6.1.8 LivaNova

- 6.1.9 Abbott

- 6.1.10 DJO Global LLC

- 6.1.11 SPR Therapeutics

- 6.1.12 Nevro Corp