|

市場調査レポート

商品コード

1430506

空域・手順設計:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Airspace And Procedure Design - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 空域・手順設計:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

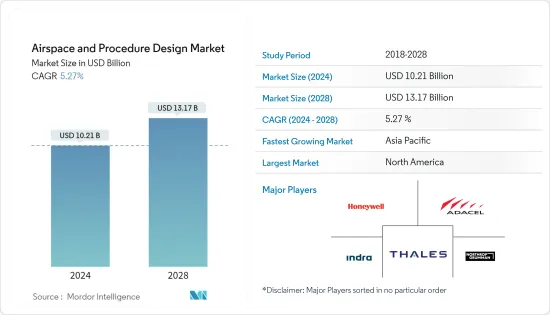

空域・手順設計市場規模は2024年に102億1,000万米ドルと推定され、2028年には131億7,000万米ドルに達すると予測され、予測期間中(2024年~2028年)のCAGRは5.27%で成長する見込みです。

主なハイライト

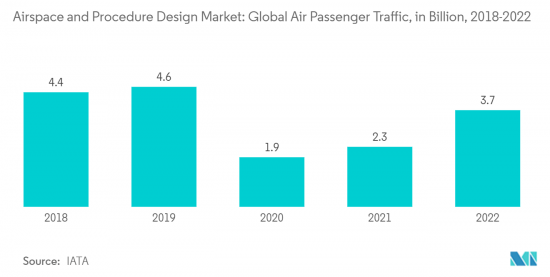

- 国際航空運送協会(IATA)、国際民間航空機関(ICAO)、国際空港評議会(ACI)、国連世界観光機関(UNWTO)、世界貿易機関(WTO)、国際通貨基金(IMF)の最新情報によると、2022年の国際航空旅客輸送量は2021年に比べて改善しました。2022年中の国際航空旅客輸送量は前年比152.7%増加し、収益旅客キロ(RPK)は2021年比で64.4%増加し、2019年12月のパンデミック前の水準の約76.9%に達しました。

- 過去数年間の旅客輸送量の増加により、政府や空港当局は既存の空港インフラの拡張や新空港の建設に投資し、旅客処理能力を高めています。このことが、予測期間中の市場成長を促進すると予想されます。

- これに加えて、航空会社や空港運営会社も航空交通管理インフラの近代化や既存設備の自動化に投資しており、これが今後数年間の市場成長を加速させると思われます。

- しかし、サイバー攻撃のリスクは、空域および手順設計市場の成長に対する大きな脅威です。

空域・手順設計市場の動向

予測期間中はハードウェアセグメントが市場シェアを独占

新しい空港の建設と既存の空港の拡張は、世界中で航空交通管理ハードウェアの需要を生み出すと予測されています。いくつかの空港では、航空交通管理業務の効率を高めるため、老朽化したハードウェア機器を新しい高度な機器に置き換えようとしています。最近THALES社は、アベイド・アマニ・カルメ国際空港、アルーシャ空港、ジュリウス・ニエレレ国際空港、キリマンジャロ国際空港、ムワンザ国際空港、ソンウェ空港にATMシステムを設置したと発表しました。この近代化は、THALES社とタンザニア民間航空局(TCAA)との間で結ばれた、同国の航空交通の安全性と効率性を高めるための契約の一環です。同社は近代化の一環として、監視レーダーとTopSky-ATCを設置しました。

同様に、2022年4月、連邦航空局は、大統領の超党派インフラ法に基づき、航空管制塔の交換、ナビゲーション、気象、追跡装置の近代化、電源システムのアップグレード、空港の航空路交通管制センター、管制塔、TRACONなどのインフラのアップグレードのために10億米ドル以上の投資を発表しました。このような開発は、予測期間中にハードウェアセグメントの需要を急速に促進すると予測されています。

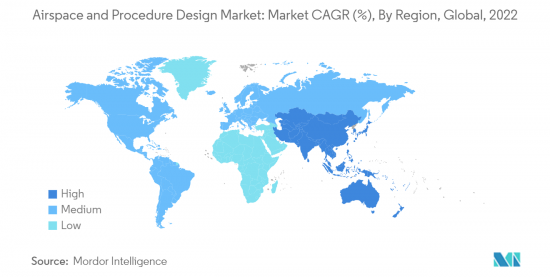

アジア太平洋地域が予測期間中に最も高い成長を遂げる

予測期間中、アジア太平洋地域が最も高いCAGRで市場をリードすると予測されます。同市場の成長は、中国とインドにおける新空港建設と既存空港の拡張に向けた旺盛な投資が後押ししています。2022年1月、中国民用航空局(CAAC)は、2025年までに国内の民間輸送空港の数を270以上に増やす計画を発表しました。新空港の建設により、2025年までに年間1,700万回の航空機移動を処理できるようになり、旅客取扱能力は9億3,000万人、貨物取扱能力は950万トンに増加します。このような開発により、高度な航空交通管理システムの導入が促進され、同国における高い安全性と運航効率が確保されることになります。加えて、同様の旅客数の増加とそれに伴う航空会社顧客からの需要、さらには新たな航空交通管理要件や環境規制により、インドの空港は継続的な適応とインフラ・運営の改善を余儀なくされています。デジタルトランスフォーメーションは、モノのインターネット(IoT)対応技術の統合を通じてインドの空港業界を再構築し、空港の運営を最適化し、安全でタイムリーな旅客輸送を可能にしています。2022年3月、メイク・イン・インディア・イニシアチブを支援するため、バーラト・エレクトロニクス社(BEL)はインド空港庁(AAI)とパートナーシップを結び、空港における航空交通管理と航空機の地上移動のためのシステムを研究開発しました。新しいATMシステムの開発とイントロダクションへのこうした投資は、予測期間中、アジア太平洋地域の航空交通管理市場の成長見通しを促進すると予想されます。

空域・手順設計産業の概要

空域・手順設計市場は半固定的であり、多くの国内外の企業が様々なハードウェア、ソフトウェア、サービスを提供しています。Adacel Technologies Limited、Honeywell International Inc.、Indra Sistemas SA、THALES、Northrop Grumman Corporationは、空域・手順設計市場の著名なプレーヤーの一部です。

プレーヤーは、内蔵のAI技術によって自ら学習し、改善することができる安全な製品の立ち上げに集中しています。ほとんどのソフトウェアメーカーは、データベース上の重要なデータへのアクセス効率と速度を改善するためにAIを使用しています。例えば、ハネウェルは空港運営会社や航空ナビゲーション・サービス・プロバイダーの業務をサポートする新世代のNAVITASソフトウェア・スイート・プラットフォームを発表しました。このソフトウェアは、人工知能(AI)、ビッグデータ、サイバーセキュリティ、機械学習、人間中心設計と統合されており、効率的な地上移動、状況認識の強化、空側の制御と監視、情報管理、統合のための航空交通サービスの自動化とデジタル化をサポートし、可能にします。国際的なプレーヤーは、空域・手順設計システム、部品、コンポーネントの現地メーカーや、システムのサードパーティ・ソフトウェア・メーカーとのパートナーシップから利益を得ることが期待されます。各社のこうした取り組みは、今後数年間、地理的プレゼンスを高めるのに役立つと期待されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 空域

- 航空路管制センター(ARTCC)

- ターミナルレーダー進入管制(TRACON)

- 航空管制塔(ATCT)

- リモートタワー

- 航空情報管理

- コンポーネント

- ハードウェア

- ソフトウェア

- エンドユーザー

- 軍事

- 商業

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Adacel Technologies Limited

- Leonardo S.p.A.

- Frequentis AG

- Advanced Navigation and Positioning

- Honeywell International Inc.

- L3Harris Technologies, Inc.

- Indra Sistemas SA

- RTX Corporation

- Saab AB

- THALES

- Northrop Grumman Corporation

- BAE Systems plc

第7章 市場機会と今後の動向

The Airspace And Procedure Design Market size is estimated at USD 10.21 billion in 2024, and is expected to reach USD 13.17 billion by 2028, growing at a CAGR of 5.27% during the forecast period (2024-2028).

Key Highlights

- According to the latest updates from the International Air Transport Association (IATA), the International Civil Aviation Organization (ICAO), the Airports Council International (ACI), the UN World Tourism Organization (UNWTO), the World Trade Organization (WTO), and the International Monetary Fund (IMF), the international air passenger traffic in 2022 improved compared to that of 2021. The international air passenger traffic during 2022 increased by 152.7% YoY, while the revenue passenger kilometers (RPK) grew by 64.4% compared to 2021 and reached around 76.9% of the December 2019 pre-pandemic levels.

- The growth in passenger traffic over the past few years has led governments and airport authorities to invest in expanding their existing airport infrastructure and constructing new airports to increase their passenger handling capacities. This is expected to drive the growth of the market during the forecast period.

- In addition to this, the airlines and airport operators also invest in the modernization of air traffic management infrastructure and automation of existing equipment, which will accelerate the market growth in the coming years.

- However, risk of cyber attack is a major threat to the growth of the airspace and procedure design market.

Airspace And Procedure Design Market Trends

Hardware Segment to Dominate Market Share During the Forecast Period

The construction of new airports and the expansion of existing airports are anticipated to generate the demand for air traffic management hardware worldwide. Several airports are replacing aging hardware equipment with new advanced equipment to enhance the efficiency of air traffic management operations. Recently, THALES announced that the company installed ATM systems at Abeid Amani Karume International Airport, Arusha Airport, Julius Nyerere International Airport, Kilimanjaro International Airport, Mwanza International Airport, and Songwe Airport. The modernization is a part of the contract between THALES and the Tanzania Civil Aviation Authority (TCAA) to enhance the country's air traffic safety and efficiency. The company installed surveillance radars and TopSky - ATC as a part of modernization.

Similarly, in April 2022, the Federal Aviation Administration announced an investment of more than USD 1 billion under the President's Bipartisan Infrastructure Law for air traffic control tower replacement, modernization of navigation, weather and tracking equipment, upgrades to power systems, infrastructure upgrades at the air route traffic control centers, towers, and TRACONs, among others at the airport. Such developments are anticipated to drive the demand for the hardware segment rapidly during the forecast period.

Asia-Pacific To Witness Highest Growth During the Forecast Period

The Asia-Pacific region is expected to lead the market with the highest CAGR during the forecast period. The growth in the market is propelled by robust investments toward constructing new airports and expanding existing airports in China and India. In January 2022, the Civil Aviation Administration of China (CAAC) announced its plan to increase the number of civil transport airports in the country to more than 270 by 2025. The construction of new airports will allow the country to handle 17 million aircraft movements annually and increase the passenger handling and cargo handling capacities to 930 million passengers and 9.5 million tonnes, respectively, by 2025. Such developments would bolster the adoption of sophisticated air traffic management systems to ensure high levels of safety and operational efficiency in the country. In addition, a similar increase in passenger volume and adjoining demand from airline customers, as well as new air traffic management requirements and environmental regulations, are forcing Indian airports to continuously adapt and improve their infrastructure and operations. Digital transformation is reshaping the Indian airport industry through the integration of the Internet of Things (IoT)- enabled technologies to help airports optimize their operations and enable safe and timely passenger travel. In March 2022, to support the Make in India Initiative, Bharat Electronics Limited (BEL) entered into a partnership with the Airports Authority of India (AAI) to research and develop systems for air traffic management and surface movement of aircraft at airports. Such investments into the development and introduction of new ATM systems are expected to drive the growth prospects of the air traffic management market in the Asia-Pacific region during the forecast period.

Airspace And Procedure Design Industry Overview

The airspace and procedure design market is semi-consolidated, with many local and international players providing various hardware, software, and services. Adacel Technologies Limited, Honeywell International Inc., Indra Sistemas SA, THALES, and Northrop Grumman Corporation are some of the prominent players in the airspace and procedure design market.

Players are concentrating on the launch of secure products that can learn and improve themselves through built-in AI technology. Most software producers are using AI to improve the efficiency and speed of accessing important data on the database. For instance, Honeywell launched a new generation NAVITAS software suite platform to support the operations of airport operators and air navigation service providers. The software is integrated with artificial intelligence (AI), big data, cybersecurity, machine learning, and human-centered designs that will support and enable automation and digitization of air traffic services for efficient ground movement, enhanced situational awareness, control and monitoring of airside, information management, and integration. International players are expected to benefit from the partnership with local producers of airspace and procedure design systems, parts, and components and third-party software manufacturers of systems. Such initiatives of the companies are expected to help them increase their geographic presence in the years to come.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Airspace

- 5.1.1 Air Route Traffic Control Centers (ARTCC)

- 5.1.2 Terminal Radar Approach Control (TRACON)

- 5.1.3 Air Traffic Control Towers (ATCT)

- 5.1.4 Remote Towers

- 5.1.5 Aeronautical Information Management

- 5.2 Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 End User

- 5.3.1 Military

- 5.3.2 Commercial

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Adacel Technologies Limited

- 6.2.2 Leonardo S.p.A.

- 6.2.3 Frequentis AG

- 6.2.4 Advanced Navigation and Positioning

- 6.2.5 Honeywell International Inc.

- 6.2.6 L3Harris Technologies, Inc.

- 6.2.7 Indra Sistemas SA

- 6.2.8 RTX Corporation

- 6.2.9 Saab AB

- 6.2.10 THALES

- 6.2.11 Northrop Grumman Corporation

- 6.2.12 BAE Systems plc