|

市場調査レポート

商品コード

1849909

希少医薬品の市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Orphan Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 希少医薬品の市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月13日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

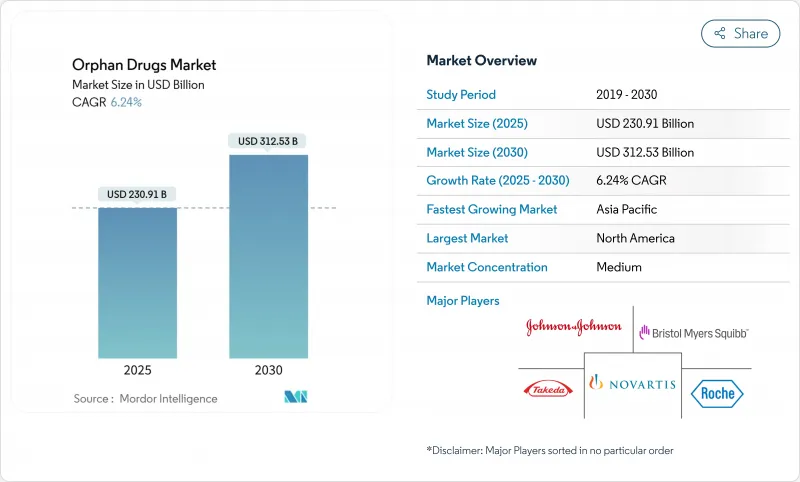

希少医薬品市場は、2025年に2,309億1,000万米ドルとなり、2030年には3,125億3,000万米ドルに達すると予測され、CAGRは6.24%で推移します。

持続的な成長は、規制上の優遇措置、遺伝子・細胞治療のブレークスルー、7,000を超える希少疾患における根強いアンメットニーズを反映しています。生物学的製剤、特に遺伝子治療とモノクローナル抗体の優位性は、一回で治る治療への軸足を強調しています。北米は強力な指定プログラムと強力な償還を背景にリードしており、アジア太平洋は政策の枠組みが拡大するにつれて勢いを増しています。競合情報では、大手製薬企業がパイプラインの厚みを確保するために専門バイオテクノロジー企業を買収し、人工知能を活用した適応試験により開発サイクルを短縮して独占期間の延長を活用しています。

世界の希少医薬品市場の動向と洞察

超希少疾患に対する遺伝子・細胞治療プラットフォームの急増

遺伝子治療は対症療法ではなく原因変異をターゲットにすることで、希少医薬品市場を再定義しつつあります。2024年11月にFDAが承認した芳香族L-アミノ酸脱炭酸酵素欠損症に対するKEBILIDIは、1回の点滴で臨床的に意味のある運動機能の改善を示しました。欧州でも同様の勢いがあり、2024年中にLENMELDYがEMAからメタクロマチック白質ジストロフィーに対する承認を取得し、バイオマーカー主導の加速化経路が検証されました。CRISPR編集とアデノ随伴ウイルス送達の融合は、世界的な有病率が1,000人未満であっても、実行可能なビジネスモデルを可能にします。1コースあたり200万米ドルを超えることもあるプレミアム価格は、メーカーが構築しなければならない特殊なインフラストラクチャーに対するリターンを支えるものです。垂直統合されたベクター製造ラインを持つアーリームーバーは、強力な参入障壁と価格決定力を獲得します。

開発期間を短縮するAI主導の適応試験

人工知能プラットフォームは、中間的な有効性と安全性のシグナルに基づくプロトコールの調整を可能にし、患者への曝露を減らし、固定デザインと比較してタイムラインを18~24カ月短縮します。2024年のAIに関するFDAのワークショップでは、文書化に対する期待が明確化され、より迅速でありながら説明可能なパスウェイが促進されます。機械学習アルゴリズムは、患者の層別化を強化します。これによりスポンサーは、より小さなNサイズで規制レベルのエビデンスを得ることができ、独占権の崖を前にした希少医薬品市場への迅速な参入が可能になります。現在では、社内にデータサイエンスチームを持つ大企業が適応試験能力を独占しており、競合との差を広げています。

高い患者一人当たりの治療費

年間治療費の中央値は2024年に25万6,000米ドルを超え、単回投与の遺伝子治療は頻繁に200万米ドルを超えます。支払者は事前承認とアウトカムベースの契約で対応し、特に治療がその後より広範な集団に拡大した場合に対応します。欧州のHTA機関は、上市後に持続的なベネフィットのエビデンスを要求するようになってきており、スポンサーは長期的なレジストリーに資金を提供するよう迫られています。そのため、価格戦略は、技術革新への投資回収と償還の実行可能性の維持という微妙な均衡を保っています。

セグメント分析

生物製剤は2024年の売上高の65.65%を占め、2030年までのCAGRは8.84%で低分子を上回る。2024年のFDA承認の25%はモノクローナル抗体または遺伝子治療であり、精密介入を可能にするモダリティ・プラットフォームへの嗜好が持続することを示しています。生物学的製剤の希少医薬品市場規模は、2030年までに2,050億米ドルに達すると予測され、高価格で取引される1回限りの治療薬に支えられています。非生物学的製剤は、再利用された低分子化合物による代謝性疾患において依然としてシェアを維持しているが、遺伝子医薬がより効果的に根本的な酵素の欠損に対処するにつれて、競合との差別化が狭まりつつあります。一方、低分子医薬品メーカーは、製剤革新とライフサイクル・マネジメントに依存しています。

第2段落遺伝子治療の模範例としては、鎌状赤血球症に対するLYFGENIAや芳香族L-AAD欠損症に対するKEBILIDIがあり、いずれも単回投与で画期的な臨床効果を示しています。製造の複雑さが参入障壁を高めており、その結果、CDMOとの提携や社内ベクター能力が買収のきっかけとなっています。規制当局は確実な効力測定と長期フォローアップを要求しており、各社は学際的なサーベイランスプログラムの確立を促しています。知的財産戦略はカプシド工学とプロモーターの最適化に重点を置き、市場競争力を強化しています。

腫瘍性疾患は2024年に40.53%のシェアを維持するが、血液悪性腫瘍の飽和が顕在化するにつれて成長ペースは鈍化します。2024年のがん領域の希少医薬品市場シェアは41%であったが、新しいカテゴリーが加速するにつれてわずかに低下すると予想されます。EMAによる再発濾胞性リンパ腫に対するOrdsponoの承認は、T細胞誘導抗体の技術革新が続いていることを裏付けています。しかし、血液・免疫疾患領域では、コンシズマブやフィツシランなどの因子補充薬がCAGR 10.35%で進展しています。

第2パラグラフSOD1-ALSに対するトフェルセンを含む神経系遺伝子治療は、パイプラインの幅を広げ、バイオマーカー主導の承認を強調しています。代謝疾患プログラムは次世代酵素補充療法やmRNA療法を活用し、ウイルス性出血熱のような感染症の希少疾患はニッチな資金を集める。投資家は、これらのセグメントにおけるポートフォリオのウェイトを評価する際、治療の新規性と規制の勢いを追跡します。

地域別分析

北米は、2024年の世界売上高の42.82%を占め、希少疾病用医薬品法に基づく7年間の独占権と25%の臨床試験税額控除の恩恵を受け続けています。WHIM症候群に対するXOLREMDIと高リスク骨髄異形成症候群に対するRYT-ELOの最近のFDA承認は、規制当局の対応力を示しています。とはいえ、インフレ抑制法は、製品が単一の希少疾病用医薬品(オーファン)の効能・効果を超えて拡大した場合、価格再交渉のリスクをもたらすため、ラベルの拡大には戦略的な注意が必要です。

欧州は、10年間の独占権と手数料の軽減を提供するEMAの集中化された手続きを強みに、希少医薬品市場の大部分を占めています。重要医薬品法(Critical Medicines Act)は、地域的な製造の弾力性を構築し、供給不足を合理化することを目指しているが、改革草案では規制当局のデータ保護を9年間に短縮することが提案されており、投資意欲を減退させる可能性があります。マネージド・エントリー契約とアウトカムベースの契約が支払側の交渉を支配し、支出を抑制しながらアクセスを確保しています。

アジア太平洋地域は2030年までのCAGRが11.62%と最も急成長している地域であり、中国のCAREプログラムとインドの希少疾患政策助成金に支えられています。この地域は人口が多いため臨床試験の募集が容易であり、可処分所得の増加もプレミアム療法を支えています。しかし、保険償還が断片的で、疫学データもさまざまであるため、即効的な導入には限界があり、スポンサーは地域ごとのエンゲージメント戦略を開発する必要があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 希少疾患の有病率の上昇

- 政府の有利なインセンティブと税額控除

- 希少疾病用医薬品の市場独占権

- 超希少疾患に対する遺伝子・細胞治療プラットフォームの急増

- AI主導の適応型試験が開発期間を短縮

- 棚上げされたフェーズII資産のニッチ適応症への転用

- 市場抑制要因

- 患者一人当たりの治療費が高め

- 試験とマーケティングのための患者プールが限られている

- 適応拡大とリアルワールドバリューに関する支払者の精査

- 独占期間を短縮するための立法提案

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 薬剤の種類別

- 生物学的製剤

- 非生物製剤

- 疾患領域別

- 腫瘍性疾患

- 血液・免疫疾患

- 神経疾患

- 代謝性疾患

- 感染症

- その他の希少疾患

- 投与経路別

- 非経口

- オーラル

- その他(吸入、局所、埋め込み型)

- 流通チャネル別

- 病院薬局

- 小売薬局

- オンライン薬局

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Johnson & Johnson

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Bristol-Myers Squibb Co.

- Amgen Inc.

- Pfizer Inc.

- Takeda Pharmaceutical Co. Ltd

- Sanofi S.A.

- AstraZeneca plc

- AbbVie Inc.

- Alexion Pharmaceuticals Inc.

- GSK plc

- Daiichi Sankyo Co. Ltd

- Bayer AG

- Vertex Pharmaceuticals Inc.

- Horizon Therapeutics plc

- Regeneron Pharmaceuticals Inc.

- BioMarin Pharmaceutical Inc.

- CSL Behring

- Sarepta Therapeutics Inc.