|

市場調査レポート

商品コード

1637909

高強度鋼:市場シェア分析、産業動向・統計、成長予測(2025~2030年)High Strength Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高強度鋼:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

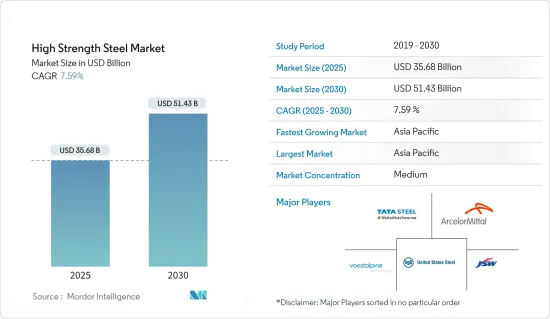

高強度鋼の市場規模は2025年に356億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは7.59%で、2030年には514億3,000万米ドルに達すると予測されます。

同市場は、同地域におけるCOVID-19の大流行により、需要や生産性の低下、サプライチェーンの混乱、地域の閉鎖などの悪影響を受けました。しかし、市場は2021年に大きな成長を示し、2022年も引き続き成長しました。

主なハイライト

- 短期的には、建設業界と自動車業界からの需要増加が市場成長を牽引するいくつかの要因となっています。

- その反面、高い生産コストと高い技術的制約が市場の成長を妨げる可能性が高いです。

- とはいえ、アジア太平洋地域の産業およびインフラ開発は、予測期間中に数多くの機会を提供すると予想されます。

- アジア太平洋地域が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

高強度鋼の市場動向

自動車産業における用途の増加

- 高強度鋼は自動車産業で広く使用され、車両全体の重量を減らすと同時に、剛性とエネルギー吸収を高める部分もあります。

- 高強度鋼は、機械的特性、厚さ、幅能力など、自動車産業での需要を増大させるいくつかの特性を持っています。

- 一般的に、自動車産業における鋼材の強度は、その化学組成、熱履歴、および製造工程で通過する変形プロセスによって変化する微細構造によって制御されます。

- 高強度鋼は、特に自動車産業において重量が燃費効率を考慮する場合、従来の鋼よりもいくつかの利点があります。その機械的特性、溶接性、疲労、静的強度、カソード保護、水素脆化性能は、自動車産業にとって有益であることが証明されています。

- ドイツは欧州自動車市場をリードしており、41の組立工場とエンジン生産工場が欧州の自動車総生産台数の3分の1に貢献しています。自動車産業の主要製造拠点のひとつであるドイツには、装置メーカー、材料・部品サプライヤー、エンジンメーカー、システム・インテグレーターなど、さまざまな分野のメーカーが集まっています。例えばOICAによると、2022年のドイツの自動車生産台数は3,677万8,820台で、2021年比で11%の増加を示しました。したがって、同国における自動車生産の増加は、高張力鋼板市場の需要増加をもたらすと予想されます。

- インドにおける自動車産業への投資の増加と進歩は、高強度鋼の消費を増加させると予想されます。例えば、タタ・モーターズは2022年4月、今後5年間で乗用車事業に30億8,000万米ドルを投資する計画を発表しました。これは同国の高強度鋼市場にプラスの影響を与えると予想されます。

- さらに、輸送車両の需要増が高強度鋼市場を牽引しています。2023年には、旺盛な需要と公共交通機関よりも個人所有の自動車を好む消費者のため、インドの自動車セクターはアジア太平洋地域で最も強くなると予測されています。例えばOICAによると、2022年の同国の自動車生産台数は5,456万6,857台で、2020年比で24%の増加を示しました。したがって、この地域の高強度鋼市場は、自動車製造全体の増加の結果として拡大する可能性が高いです。

- さらに、米国は世界第2位の自動車販売・生産市場です。例えば、OICAによると、2022年の米国の自動車生産台数は1,006万339台で、2021年比で10%の増加を示しました。その結果、自動車生産台数の増加により、燃料添加剤市場の需要増が見込まれます。

- 燃費向上と自動車の軽量化を目的とした高強度鋼の使用増加が、自動車業界の市場成長を押し上げると思われます。

アジア太平洋地域を支配する中国

- 高強度鋼市場では中国がアジア太平洋地域で最大のシェアを占めています。同国における投資と建設活動の活発化により、高強度鋼市場の需要は予測期間を通じて増加すると予想されます。

- 中国はアジア太平洋地域でGDPが最大の経済大国です。同国の成長率は依然として高いが、人口の高齢化が進み、経済が投資から消費へ、製造業からサービス業へ、外需から内需へとリバランスしているため、徐々に低下しています。

- 中国はここ数年、世界有数のインフラ投資国であり、大きな貢献をしています。例えば、中国国家統計局(NBS)によると、2022年の中国における建設工事の生産額は27兆6,300億元(4兆1,085億8,100万米ドル)に達し、2021年と比較して6.6%増加しました。

- さらに、自動車産業は引き続き中国最大の産業であり、近い将来に明るい兆しが見えます。例えば、OICAによると、2022年の自動車生産台数は27億2,061万台で、2021年比で3%増加しました。したがって、同国の自動車生産におけるこのようなポジティブなシナリオは、高強度鋼市場に対する需要の上向きを生み出すと予想されます。

- さらに、中国は今後3年以内に米国を抜いて世界最大の航空旅行市場になろうとしています。それでも、同国の航空に対する意欲は指数関数的に伸び続けています。例えば、2023年4月、フランスの国賓として中国を訪問したエアバスは、中国の航空業界のパートナーと新たな協力協定を締結しました。今後20年間、中国の航空輸送量は年率5.3%で成長すると予測されており、これは世界平均の3.6%を大幅に上回る。このため、2023年から2041年の間に、旅客機と貨物機の需要が8,420機となり、今後20年間で約39,500機が新たに必要となる世界総需要の20%以上に相当します。したがって、航空産業からのこれらの拡張は、高強度鋼市場に対する上向きの需要を生み出すと予想されます。

- UNCTDによると、2022年の中国の商船数は11万5154隻で、2021年比約6.1%増の10万8481隻となった。従って、商船の増加は高強度鋼市場の需要増加をもたらすと予想されます。

- したがって、国内の様々なエンドユーザー部門の成長に伴い、高強度鋼の需要は今後数年間で大幅に増加すると予想されます。

高強度鋼業界の概要

高強度鋼市場は、部分的に統合されています。この市場の主要企業(順不同)には、アルセロール・ミッタル、米国スチール・コーポレーション、タタ・スチール、JSW、ボスタルピネAGなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設分野からの需要の急増

- 自動車産業からの需要増加

- その他の促進要因

- 抑制要因

- 生産コストの高騰

- その他の阻害要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- 二相鋼

- 焼入れ硬化鋼

- 炭素マンガン鋼

- その他の製品タイプ

- 用途別

- 自動車

- 建設機械

- イエローグッズおよび鉱山機械

- 航空・海洋

- その他の用途

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ArcelorMittal

- ChinaSteel

- CITIC Heavy Industries Co., Ltd.

- JSW Steel

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- SSAB AB

- Tata Steel

- United States Steel Corporation

- Voestalpine AG

第7章 市場機会と今後の動向

- アジア太平洋地域の産業・インフラ開発

- その他の機会

The High Strength Steel Market size is estimated at USD 35.68 billion in 2025, and is expected to reach USD 51.43 billion by 2030, at a CAGR of 7.59% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic in the region, including decreased demand and productivity, supply chain disruptions, and regional lockdowns. However, the market showed significant growth in 2021 and continued to grow in 2022.

Key Highlights

- Over the short term, increasing demand from the construction and automotive industries are some factors driving the growth of the market studied.

- On the flip side, high production costs and high technological constraints will likely hinder the market's growth.

- Nevertheless, industrial and infrastructural development in Asia-Pacific is anticipated to provide numerous opportunities over the forecast period.

- The Asia-Pacific region is expected to dominate the market and will also witness the highest CAGR during the forecast period.

High Strength Steel Market Trends

Increasing Applications in the Automotive Industry

- High-strength steels are widely used in the automotive industry to reduce overall vehicle weight while increasing stiffness and energy absorption in some areas.

- High-strength steels have several properties that increase their demand in the automotive industry, including mechanical properties, thickness, and width capabilities.

- In general, the strength of steel in the automotive industry is controlled by its microstructure, which varies depending on its chemical composition, thermal history, and the deformation processes it goes through during the production process.

- High-strength steel has several advantages over conventional steel, particularly when weight is a consideration for fuel efficiency in the automotive industry. Their mechanical properties, weldability, fatigue, static strength, cathodic protection, and hydrogen embrittlement performance have proven to be beneficial to the automotive industry.

- Germany leads the European automotive market, with 41 assembly and engine production plants contributing to one-third of Europe's total automobile production. Germany, one of the leading manufacturing bases of the automotive industry, is home to manufacturers from different segments, such as equipment manufacturers, material and component suppliers, engine producers, and whole system integrators. For instance, according to OICA, in 2022, automobile production in Germany amounted to 36,77,820 units, which showed an increase of 11% compared to 2021. Therefore, increasing the production of automobiles in the country is expected to create an upside demand for high strength steel market.

- Increased investments and advancements in the automobile industry in India are expected to increase the consumption of high-strength steel. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This is expected to positively impact the high-strength steel market in the country.

- Moreover, the growing demand for transport vehicles drives the high-strength steel market. In 2023, India's automotive sector is predicted to be the strongest in the Asia-Pacific region, owing to strong demand and consumers' preference for personal vehicles over public transportation. For instance, according to OICA, in 2022, automobile production in the country amounted to 54,56,857 units, which showed an increase of 24% compared to 2020. Therefore, the region's high-strength steel market is likely to expand as a result of the rise in overall automobile manufacturing.

- Furthermore, the United States is the second-largest vehicle sales and production market globally. For instance, according to OICA, in 2022, automobile production in the United States amounted to 1,00,60,339 units, which showed an increase of 10% compared to 2021. As a result, an increase in automobile production is expected to create an upside demand for the fuel additives market.

- Increasing the usage of high-strength steel for better fuel efficiency and lightweight vehicles will boost the market growth in the automotive industry.

China to Dominate the Asia-Pacific Region

- China holds the largest Asia-Pacific market share for high strength steel market. The demand for the high-strength steel market is expected to rise throughout the forecast period due to rising investments and construction activity in the country.

- China is the largest economy in the Asia-Pacific region in terms of GDP. The growth in the country remains high but is gradually diminishing as the population is aging, and the economy is rebalancing from investment to consumption, manufacturing to services, and external to internal demand.

- China is a huge contributor, as it has been one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to 27.63 trillion yuan (USD 4108.581 billion), an increase of 6.6% compared with 2021.

- Moreover, automotive continues to remain the country's largest sector and reflects positive signs for the near future. For instance, according to OICA, in 2022, automobile production in the country amounted to 2,70,20,615 units, which shows an increase of 3% compared with 2021. Therefore, such a positive scenario in the production of automobiles in the country is expected to create an upside demand for high strength steel market.

- Furthermore, China is on course to overtake the United States as the world's biggest air travel market within the next three years. Still, the country's appetite for aviation continues to grow exponentially. For instance, on April 2023, during a French state visit to China, Airbus signed new cooperation agreements with China's Aviation industry partners. Over the next 20 years, China's air traffic is forecast to grow at 5.3% annually, significantly faster than the world average of 3.6%. This will lead to a demand for 8,420 passenger and freighter aircraft between 2023 and 2041, representing more than 20% of the world's total demand for around 39,500 new aircraft in the next 20 years. Therefore, these expansions from the aviation industry are expected to create an upside demand for high strength steel market.

- According to UNCTD, China had 1,15,154 merchant ships in 2022, which showed an increase of around 6.1% compared to 2021, amounting to 1,08,481 merchant ships. Therefore, the increase in merchant ships is expected to create an upside demand for high strength steel market.

- Hence, with the growth in the various end-user sectors in the country, the demand for high-strength steel is expected to increase significantly in the upcoming years.

High Strength Steel Industry Overview

The High Strength Steel Market is partially consolidated in nature. The major players in this market (not in a particular order) include ArcelorMittal, United States Steel Corporation, Tata Steel, JSW, and voestalpine AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Increasing Demand from Construction Sector

- 4.1.2 Increasing Demand from Automobile Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Costs of Production

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Dual Phase Steel

- 5.1.2 Bake Hardenable Steel

- 5.1.3 Carbon Manganese Steel

- 5.1.4 Other Product Types

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Construction

- 5.2.3 Yellow Goods and Mining Equipment

- 5.2.4 Aviation and Marine

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 ChinaSteel

- 6.4.3 CITIC Heavy Industries Co., Ltd.

- 6.4.4 JSW Steel

- 6.4.5 NIPPON STEEL CORPORATION

- 6.4.6 Nucor Corporation

- 6.4.7 POSCO

- 6.4.8 SAIL

- 6.4.9 SSAB AB

- 6.4.10 Tata Steel

- 6.4.11 United States Steel Corporation

- 6.4.12 Voestalpine AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Industrial and Infrastructural Development in Asia-Pacific

- 7.2 Other Opportunities