|

|

市場調査レポート

商品コード

1408754

日本のデータセンターネットワーキング:市場シェア分析、産業動向と統計、2024年~2030年の成長予測Japan Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本のデータセンターネットワーキング:市場シェア分析、産業動向と統計、2024年~2030年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

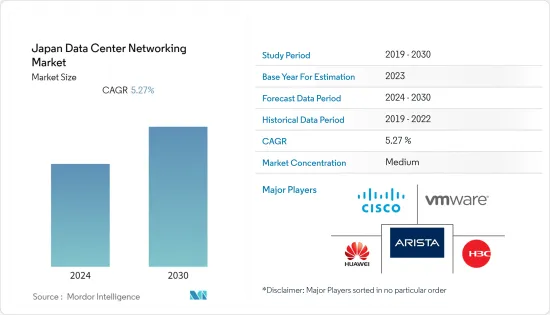

日本のデータセンターネットワーキング市場は、前年度に7億960万米ドルの規模に達し、予測期間中のCAGRは5.27%になると予測されています。

主なハイライト

- 中小企業におけるクラウドコンピューティング需要の増加、データセキュリティに関する政府規制、国内企業による投資の増加が、日本のデータセンター需要を牽引する主な要因の1つです。

- 日本のデータセンターネットワーキング市場の今後のIT負荷容量は、2029年までに2000MWに達すると予想されます。日本の床面積は2029年までに1,000万平方フィートに増加すると予想されます。

- 設置されるラックの総数は、2029年までに50万ユニットに達すると予想されます。2029年には、東京に最大数のラックが設置される見込みです。日本を結ぶ海底ケーブルシステムは30近くあり、その多くが建設中です。

- 2023年に開通が予定されているそのような海底ケーブルのひとつが東南アジア-日本ケーブル2(SJC2)で、千倉と志摩を陸揚げ点とする10,500キロメートル以上に及ぶ。

- データ・ストレージへのニーズの高まりにより、データセンターの数は全国的に急増しています。また、エネルギーはデータセンターの運用コストの約40%を占めており、データセンターがエネルギー効率を重視する重要性も高まっています。コスト削減策としてエネルギー効率を向上させるため、主要企業は日本におけるデータセンターのグリーン基準の策定に注力しており、その結果、インフラ管理に対する需要が高まっています。したがって、このような要因が予測期間中の市場成長を促進すると予想されます。

日本のデータセンターネットワーキング市場動向

IT・通信セグメントが大きなシェアを占める。

- クラウドベースのサービス導入の増加により、日本ではリテールおよびハイパースケールのコロケーションサービスが拡大し、その結果、データセンターのスペース需要が増加し、データセンター内のネットワーク機器やサービスのニーズが高まっています。

- 日本ではクラウドサービスの人気が高まっています。ビッグデータ統合の必要性、より多くのリモートワークとクラウドへのデータ移行に対する需要が、国内クラウドデータセンターの利用を促進しています。

- クラウドはすべてのエンドユーザーの間で大きな成長を示すと予想されます。日本政府のデジタル庁は、中央官庁と地方官庁の両方でクラウドサービスの利用を推進しています。日本では、企業がクラウドインフラに移行するビジネスケースは、いくつかの要因によって支えられています。クラウド・インフラストラクチャは多額の設備投資を必要とせず、クラウド・コンピューティングは各企業のITシステムに合わせて容易に拡張できます。全体として、クラウドの成長率は13.51%です。

- さらに、電気通信分野では、政府はLTEの長期進化に伴い、現在よりも高速なデータ転送が可能な5Gやその他の最先端技術の導入を引き続き推進しています。NTTドコモ、KDDI、ソフトバンク、楽天モバイルは、総務省からそれぞれ5Gの周波数帯を割り当てられました。

- 加えて、日本のモバイルデータサービス収入は、主にモバイルインターネット契約数の増加と、より高いARPU(ユーザー1人当たり平均収入)をもたらす5Gサービスの採用増加によって、予測期間中に6.8%の成長率で増加すると予想されます。このような発展的側面は、同地域におけるデータセンターの成長をさらに補完し、同市場におけるネットワーク機器とサービスの成長を実質化すると予測されます。

イーサネットスイッチが最大市場シェア

- データセンターのイーサネットスイッチは、データセンター環境で動作するネットワーク機器です。データの効率的かつ迅速な転送を促進するため、データセンターのサーバー、ストレージ機器、その他のネットワーク機器間の相互接続を確立する上で重要な役割を果たします。スイッチは、10GbE、25GbE、40GbE、100GbEなどのギガビットイーサネットやマルチギガビットイーサネットに対応し、高速データ転送を実現するように設計されています。

- 日本各地のデータセンターでは、イーサネット・スイッチの広範なネットワークが使用されています。日本には、金融、テクノロジー、ヘルスケアなど幅広い業界をサポートするデータセンターが数多くあります。インフラの効率性と信頼性を確保するため、これらのデータセンターはイーサネット・スイッチなどの高性能ネットワーク機器に依存しています。

- 日本では5Gサービスが大幅に展開・採用され、データセンターの成長が拡大しています。総務省は、日本の5G体験を引き続き前進させることを目指しています。2024年3月末までに5G人口カバー率98%という目標を掲げています。データセンター事業者は、世界市場での競争力を維持するため、先端技術への投資を増やしています。ネットワークのニーズを満たすために、国内外のブランドを含む様々なメーカーのイーサネットスイッチに頼ることがあります。

- 市場の主要企業は、市場の需要を満たすためにネットワーク機器の更新に注力しています。2023年6月、シスコのNexus 9800シリーズモジュラースイッチは、複数の第1世代ラインカードとファブリックモジュールの組み合わせを含む新しいシャーシアーキテクチャにより、Cisco Nexus 9000シリーズのポートフォリオを拡張し、57Tbpsから最大115Tbpsまで拡張できるようになります。シャーシの各ラインカードスロットは、400GEまたは100GEポート、およびそれ以上の速度を提供するラインカードに対応します。

- ハイパースケールのデータセンターは、エンタープライズ・データセンターと比較して、規模の経済性やカスタム・エンジニアリングなどの利点があります。こうした施設は日本でも増えつつあります。以前は、日本の企業は地元のシステム・インテグレーターに依存していました。しかし現在では、フルクラウド化に対してより保守的なアプローチをとっています。ハイパースケーラは日本への投資を続けており、民間企業や政府のデジタル化によって未開拓の大きな成長がもたらされると見ています。データセンターに対する需要は、インターネット利用者の増加や国全体のデジタル化に伴って継続的に高まっており、予測期間中、同分野はまずまずの成長を遂げると予想されます。

日本のデータセンター・ネットワーキング産業の概要

日本では今後DC建設プロジェクトが予定されており、日本のデータセンター・ネットワーキング産業の今後数年間の需要増加が見込まれます。同市場は、Cisco Systems Inc.、Arista Networks Inc.、H3C Technologies、VMware Inc.、Huawei Technologiesなどの主要プレイヤーを中心に、適度に統合されています。これらの主要プレイヤーは大きな市場シェアを持ち、同地域での顧客基盤拡大に積極的に取り組んでいます。

2023年8月、H3Cは次世代データセンタースイッチS9827シリーズを発表しました。この革新的な製品は、CPOシリコンフォトニクス技術で構築され、その顕著な能力で業界の画期的な出来事となった。シングルチップで最大51.2Tの帯域幅を提供し、64個の800Gポートをサポートすることで、400G製品と比較してスループットが8倍向上しています。この設計には、液体冷却やインテリジェントなロスレスオペレーションなどの先進技術が組み込まれており、これらの技術を総動員することで、高度に普及し、低レイテンシーでエネルギー効率の高いスマートネットワークの構築に貢献します。

2022年11月、エクイニクスとヴイエムウェアは、新たなデジタルインフラとマルチクラウドサービスに対する需要の高まりを受けて、重要な発表を行いました。両社は、パートナーシップを世界規模で拡大する計画を明らかにしました。さらに両社は、パフォーマンス、セキュリティ、コスト効率の向上によりエンタープライズ・アプリケーションをサポートすることを目的とした新しい分散型クラウド・サービスとして、VMware Cloud on Equinix Metalを発表しました。このサービスは、VMwareが管理・サポートするクラウドインフラストラクチャと、エクイニクスの相互接続された世界なベアメタル・アズ・ア・サービスを組み合わせたもので、企業向けに強化されたクラウドソリューションを提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドベースのサービス採用の増加

- 5Gネットワークの登場が市場成長を促進

- 市場抑制要因

- サイバーセキュリティの脅威とランサムウェア攻撃

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- 成分別

- 製品別

- イーサネットスイッチ

- ルーター

- ストレージ・エリア・ネットワーク(SAN)

- アプリケーション・デリバリー・コントローラー(ADC)

- その他のネットワーク機器

- 以下を含むネットワーク・セキュリティ機器、WAN最適化アプライアンス、ソフトウェア

- サービス別

- インストレーション&インテグレーション

- トレーニング&コンサルティング

- サポート&メンテナンス

- 製品別

- エンドユーザー

- IT・通信

- BFSI

- 政府機関

- メディア&エンターテイメント

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Arista Networks Inc.

- H3C Technologies Co., Ltd.

- VMware Inc

- Huawei Technologies Co. Ltd.

- Extreme Networks Inc.

- NVIDIA Corporation(Cumulus Networks Inc.)

- Dell EMC

- NEC Corporation

- IBM Corporation

- HP Development Company, L.P.

- Intel Corporation

- Broadcom Corp

- Schneider Electric

第7章 投資分析

第8章 市場機会と今後の動向

The Japan data center networking market reached a value of USD 709.6 million in the previous year, and it is further projected to register a CAGR of 5.27% during the forecast period.

Key Highlights

- The increasing demand for cloud computing among SMEs, government regulations for local data security, and growing investment by domestic players are some of the major factors driving the demand for data centers in the country.

- The upcoming IT load capacity of the Japan data center market is expected to reach 2000 MW by 2029. The country's construction of raised floor area is expected to increase to 10 million sq. ft by 2029.

- The country's total number of racks to be installed is expected to reach 500 K units by 2029. Tokyo is expected to house the maximum number of racks by 2029. There are close to 30 submarine cable systems connecting Japan, and many are under construction.

- One such submarine cable that is estimated to start service in 2023 is Southeast Asia-Japan Cable 2 (SJC2), which stretches over 10,500 Kilometers with landing points from Chikura and Shima, Japan.

- An increasing need for data storage has resulted in an upsurge in the number of data centers nationwide. Additionally, energy represents around 40% of the operational costs of a data center; it is also becoming increasingly important for data centers to focus on energy efficiency. To improve energy efficiency as a cost-saving measure, key players focus on developing a green standard for data centers in Japan, which results in increasing the demand for Infrastructure management. Hence, such factors are expected to drive market growth during the forecast period.

Japan Data Center Networking Market Trends

IT & Telecommunication Segment Holds the Major Share.

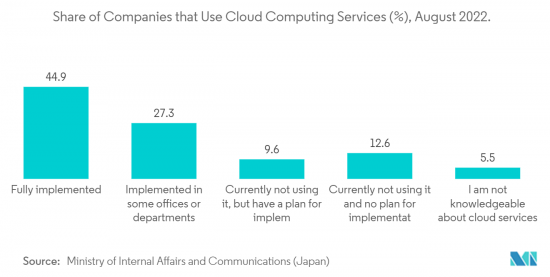

- The increasing adoption of cloud-based services is driving the expansion of retail and hyperscale colocation services in Japan, resulting in increased demand for space in data centers and, consequently, the need for more network devices and services within data centers.

- Cloud services are growing in popularity in Japan. The need for big data integration and the demand for more remote work and data migration to the cloud are driving the use of domestic cloud data centers.

- Cloud is expected to showcase major growth among all the end users. The Government of Japan's Digital Agency promotes the utilization of cloud services for both central government and local government offices. In Japan, the business case for enterprises moving to cloud infrastructure is supported by several factors. Cloud infrastructure does not require a large capital investment, and cloud computing can easily be scaled to each company's IT system. Overall, the growth rate for the cloud is 13.51%.

- Further, in the Telecom sector, the Government is continuing its push to deploy 5G and other cutting-edge technologies that could transfer data faster than currently available with the long-term evolution of LTE. NTT DOCOMO, KDDI, Softbank, and Rakuten Mobile were each allocated a 5G spectrum by the Ministry of Internal Affairs and Communication (MIC).

- Additionally, Mobile data service revenue in Japan is expected to increase at a growth rate of 6.8% during the forecast period, primarily driven by growing mobile internet subscriptions and the increasing adoption of higher average revenue per user (ARPU)-yielding 5G services. Such developmental aspects are expected to further complement the growth of the data centers in the region and substantiate the growth of network devices and services in the market.

Ethernet Switches Holds Largest Market Share

- Data center ethernet switches are network devices that operate in a data center environment. In order to facilitate the efficiency and rapid transfer of data, they play an essential role in establishing interconnection between servers, storage devices, or other network equipment at a data center. Switches are designed for high-speed data transmission with support for gigabit and multigigabit Ethernet, including 10GbE, 25GbE, 40GbE, 100GbE, and beyond.

- Data centers throughout Japan use an extensive network of ethernet switches. Japan has many data centers to support a broad range of industries, including finance, technology, healthcare, and so on. To ensure efficiency and reliability in their infrastructure, these data centers rely on High-Performance Networking Equipment such as ethernet switches.

- Significant deployment and adoption of 5G services in Japan, resulting in increasing the growth of the data centers. The Ministry of International Affairs and Communications aims to continue moving the Japanese 5G experience forward. It set a target of 98% 5G population coverage by the end of March 2024. Data center operators are increasingly investing in advanced technology to maintain their competitiveness in a global market. To meet the network needs, they may rely on Ethernet switches from various manufacturers, including domestic and international brands.

- The key players in the market focus on updating the network devices to meet the market demand. In June 2023, Cisco's Nexus 9800 Series modular switches expand the Cisco Nexus 9000 Series portfolio with a new chassis architecture to include a combination of several first-generation line cards and fabrics modules, allowing it to scale from 57 Tbps up to 115 Tbps. Each line card slot on the chassis can support line cards that now offer 400GE or 100GE ports and higher speeds.

- Hyperscale data centers offer advantages such as economies of scale and custom engineering over enterprise data centers. These facilities are increasing in Japan. Previously, Japanese businesses relied on local systems integrators. However, now, they have a more conservative approach to going full cloud. Hyperscalers continue to invest in Japan and see a large, untapped growth coming from digitization in the private sector and the government. The demand for data centers is continuously rising along with a growing number of internet users and digitalization across the country, which is expected to experience decent growth in the segment during the forecast period.

Japan Data Center Networking Industry Overview

The upcoming DC construction projects in Japan are expected to drive increased demand in the Japan Data Center Networking Market over the coming years. This market is moderately consolidated, featuring key players such as Cisco Systems Inc., Arista Networks Inc., H3C Technologies Co., Ltd., VMware Inc., and Huawei Technologies Co. Ltd. These major players, holding significant market shares, are actively engaged in expanding their customer base in the region.

In August 2023, H3C introduced the S9827 series, a next-generation data center switch. This innovative product, built on CPO silicon photonics technology, marks a milestone in the industry with its remarkable capabilities. It offers a single-chip bandwidth of up to 51.2T and supports 64 800G ports, resulting in an eightfold increase in throughput compared to 400G products. The design incorporates advanced technologies such as liquid cooling and intelligent lossless operations, which collectively contribute to the creation of a highly widespread, low-latency, and energy-efficient smart network.

In November 2022, Equinix, Inc. and VMware, Inc. made a significant announcement in response to the growing demand for new digital infrastructure and Multicloud services. The two companies revealed their plans for a worldwide expansion of their partnership. Additionally, they introduced VMware Cloud on Equinix Metal as a new distributed cloud service aimed at supporting enterprise applications with improved performance, security, and cost-effectiveness. This service is set to combine VMware's managed and supported cloud infrastructure with Equinix's interconnected global bare-metal-as-a-service offering, providing an enhanced cloud solution for businesses.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Cloud-Based Services

- 4.2.2 Advent of 5G Networks Drives Market Growth

- 4.3 Market Restraints

- 4.3.1 Cybersecurity Threats and Ransomware Attacks

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.1.5.1 Including: Network security equipment, WAN optimization appliance, Softwares)

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Arista Networks Inc.

- 6.1.3 H3C Technologies Co., Ltd.

- 6.1.4 VMware Inc

- 6.1.5 Huawei Technologies Co. Ltd.

- 6.1.6 Extreme Networks Inc.

- 6.1.7 NVIDIA Corporation (Cumulus Networks Inc.)

- 6.1.8 Dell EMC

- 6.1.9 NEC Corporation

- 6.1.10 IBM Corporation

- 6.1.11 HP Development Company, L.P.

- 6.1.12 Intel Corporation

- 6.1.13 Broadcom Corp

- 6.1.14 Schneider Electric