|

市場調査レポート

商品コード

1408746

データセンターネットワーキング:市場シェア分析、産業動向・統計、成長予測、2024年~2030年Data Center Networking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2030 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンターネットワーキング:市場シェア分析、産業動向・統計、成長予測、2024年~2030年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

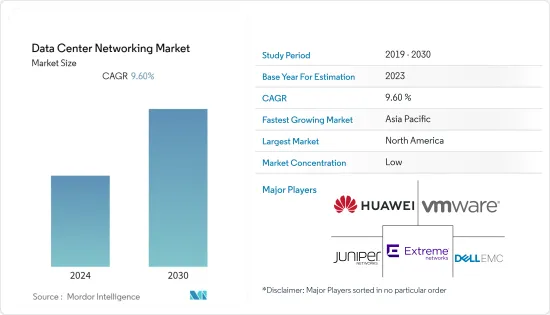

世界のデータセンターネットワーキング市場は、前年度に245億米ドルの規模に達し、予測期間中のCAGRは9.6%になると予測されています。

主なハイライト

- ネットワークソリューションはここ数年で大きな支持を得ているが、その主な理由は、負荷分散や性能向上、さらに高度な要件への対応に対するニーズの高まりにあります。帯域幅の需要は企業の予算をはるかに上回るペースで増加しており、分散型サービス拒否(DDoS)などのサイバー攻撃も絶えず増加しています。企業にとって、ユーザーが期待する速度でアプリケーションを安全かつ効率的に配信することが課題となっています。このことが大きな市場需要につながっています。

- デジタル化の進展はデータセンターの需要を増加させ、それに比例してネットワーキング市場も牽引すると思われます。エッジコンピューティングへの業界全体の投資は、今後4年間でデータセンターのエコシステムのプロファイルを大きく変え、コンピューティング全体に占めるエッジコンポーネントの割合を21%から2026年には27%へと29%引き上げると思われます。バーティヴがデータセンター業界のスペシャリストを対象に実施した新しい世界調査の重要な調査結果のひとつに、業界のエッジへのシフトがどの程度進行しているかがあります。

データセンターネットワーキング市場動向

アプリケーションデリバリーコントローラーが大きなシェアを占める

- アプリケーションデリバリーコントローラーは、主にピーク時のセキュリティとアプリケーションへのアクセスを提供します。コンピューティングがクラウドに移行するにつれ、ソフトウェア・アプリケーションデリバリーコントローラー(ADC)は、従来はカスタムメイドのハードウェアが行っていたタスクを実行するようになった。ADCはまた、アプリケーション展開のための追加機能と柔軟性を提供します。

- 今日のデジタルビジネス環境では、企業は競争、成長、繁栄のために俊敏性と革新性を維持することに重点を置いています。そのため、企業はアプリケーションの開発、デプロイ、変更、管理のためのシンプルで合理的な方法を求めており、DevOpsはデジタル・ビジネス戦略の最前線かつ中心的な役割を担っています。ADCは、DevOpsが可能にする完全なスピードと俊敏性を実現する上で非常に重要です。

- 企業が増大するデータ量からより大きな価値を引き出すことに注力する中、市場ベンダーはスケーラブルでセキュア、かつコスト効率に優れた最新のADCソリューションを投入しています。例えば、2021年5月、アレイ・ネットワークは、APVシリーズ・アプリケーション・パフォーマンス・コントローラのソフトウェア・バージョン(バージョン10.2.x)と革新的なハードウェア・プラットフォーム(x800シリーズ)を発表しました。APV x800シリーズの物理アプライアンス(APV1800、2800、5800など)は、複数のメトリクス、40 Gig-Eインターフェイス、SSLパフォーマンスの向上を提供します。

- ラップトップやデスクトップに比べ、スマートフォンやタブレットなどのモバイル端末でネットサーフィンをするユーザーが増え、大量のデータが生成されるようになっています。GSM協会によると、2025年には米国が世界で最もスマートフォンの普及率が高くなると予想されています。

- ベンダーは継続的に研究開発活動に投資し、市場での存在感と顧客基盤を高めるために革新的な製品を提供しています。例えば、F5は2022年8月、顧客のNGINXインスタンス・フリートに対するより良い制御を提供するよう設計された、新しいトラフィック管理およびセキュリティ・ソリューションの発売を発表しました。新たに発表されたF5 NGINX Management Suite 1.0は、NGINXインスタンス、アプリケーション・プログラミング・インターフェース(API)管理ワークフロー、アプリケーション配信サービス、セキュリティ・ソリューションの高い可視性と制御を提供する一元化されたダッシュボードを備えています。

アジア太平洋地域が市場を大きく成長させる

- アジア太平洋地域では、ハイパーコネクティビティ環境により、消費者や企業のコネクティビティやコラボレーションのニーズをサポートする上で基盤となる役割を担う通信事業者の重要性が高まっています。アジア太平洋全体では、通信事業者の75%がプラスの収益成長を記録しました。通信市場の成熟度ランキングでは、韓国は香港に次いで世界第2位です。

- データセンターのニーズは大幅に増加しており、効率性と低遅延性が重視されています。中国とインドは、データセンターの建設で世界的に競合他社を追い抜くことに力を入れており、大企業がデータサービスの安定性と信頼性を確保するためにデータセンターの規模を拡大しようとしているため、処理能力に対する需要が急増しています。

- 韓国政府は、同国の超高速インターネット接続、電子政府サービス、安定した長期進化(LTE)の可用性を強化するため、クラウドコンピューティング技術を採用しました。これは予測期間中、市場の成長にプラスに働くと予想されます。

- 技術の進歩により、調査対象市場では接続機器数が増加しています。さらに、中国のクラウドコンピューティング産業の成長の背景には、政府の強力なバックアップと民間セクターの多額の投資があります。さらに、5Gおよび5G対応機器は、機器の相互接続性を飛躍的に高める。その結果、接続デバイスが増加し、クラウドベースのアプリケーションのデータトラフィックとセキュリティを制御する必要性が直接増大します。

- また、中国、インド、インドネシアなどの国々では、インターネットユーザーとデータトラフィックが増加しており、同地域におけるADCソリューションの成長をさらに促進しています。デジタル時代の進展に伴い、市場ベンダーはエンドユーザーにより革新的なネットワークソリューションや製品を提供し、最高の技術体験を保証することで、市場セグメントを牽引しています。

- 例えば、2022年6月、サイバーセキュリティおよびアプリケーションデリバリソリューションプロバイダーのラドウェアとマネージドセキュリティサービスプロバイダーのOneSecureは、協業契約の拡大を発表しました。OneSecureのASEAN企業向けWebyith改ざんおよびドメインフィッシング監視サービスを強化するため、MSSPはサイバーセキュリティ・スイートを拡張し、ラドウェアのApplication Protection-as-a-Serviceサービスとクラウド分散型サービス妨害(DDoS)防御サービスを含めると発表しました。

データセンターネットワーキング業界の概要

世界のデータセンターネットワーキング市場は、近年激化している競合情勢を特徴とする、顕著な断片化を示しています。Extreme Networks社、Dell EMC社、VMware社をはじめとする業界の主要企業は、その地位を固め、大きな市場シェアを獲得しています。これらの主要企業は、様々な地域における顧客基盤の拡大に積極的に注力しています。この目標を達成するために、市場シェアを強化し、全体的な収益性を向上させることを目的とした戦略的な協業イニシアティブを採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- クラウドストレージのニーズの高まりと信頼性の高いアプリケーションパフォーマンスに対する需要の高まり

- 企業におけるサイバー攻撃の増加

- 市場抑制要因

- ネットワークの複雑化

- バリューチェーン/サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響評価

第5章 市場セグメンテーション

- コンポーネント別

- 製品別

- Ethernet スイッチ

- ルーター

- ストレージエリアネットワーク(SAN)

- アプリケーションデリバリーコントローラー(ADC)

- その他

- サービス別

- 設置・インテグレーション

- トレーニング・コンサルティング

- サポート・メンテナンス

- 製品別

- エンドユーザー別

- IT・通信

- BFSI

- 政府

- メディア・エンターテインメント

- その他

- 地域

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東

- アフリカ

第6章 競合情勢

- 企業プロファイル

- Extreme Networks Inc.

- Dell EMC

- Vmware, Inc.

- Huawei Technologies Co. Ltd.

- Juniper Networks Inc.

- Arista Networks Inc.

- NEC Corporation

- HP Development Company, L.P.

- Fortinet, Inc.

- Array Networks, Inc.

- Radware Corporation

- A10 Networks, Inc.

- Moxa Inc.

- Lenovo Group Limited

- Broadcom Corporation

- H3C Holding Limited

- NVIDIA(Cumulus Networks Inc.)

- Cisco Systems Inc.

- F5 Networks Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The global data center networking market reached a value of USD 24.5 billion in the previous year, and it is further projected to register a CAGR of 9.6% during the forecast period.

Key Highlights

- Networking solutions have gained significant traction in the past few years, primarily owing to the rising need for load balancing, improving performance, as well as to handle much more advanced requirements. Bandwidth demand is growing much faster than the company budgets, and cyber attacks such as distributed denial-of-service (DDoS) are constantly on the rise. It has become a challenge for companies to securely and efficiently deliver their applications at the speed the users expect. This factor leads to major market demand.

- The rise in digitalization will likely increase the demand for data centers, proportionately driving the networking market. Significantly, industry-wide investment in edge computing will transform the profile of the data center ecosystem over the next four years, raising the edge component of total computing by 29%, from 21% of total computing to 27% in 2026. The extent of the industry's ongoing shift to the edge is among the significant findings from a new global survey of data center industry specialists from Vertiv.

- The upcoming IT load capacity of the global data center server market is expected to reach 71K MW by 2029. The region's construction of raised floor area is expected to increase 273.9 million sq. ft by 2029. The region's total number of racks to be installed is expected to reach 14.2 million units by 2029. North America is expected to house the maximum number of racks by 2029.

- There are close to 500 submarine cable systems connecting the regions globally, and many are under construction. One such submarine cable that is estimated to start service in 2025 is CAP-1, which stretches over 12,000 km with a landing point in Grover Beach, United States.

Data Center Networking Market Trends

Application Delivery Controller to Hold Significant Share

- The application delivery controllers primarily provide security and access to the applications at peak times. As computing is moving toward the cloud, software application delivery controllers (ADCs) have been performing tasks that have been traditionally performed by custom-built hardware. They also offer additional functionalities and flexibility for application deployment.

- In today's digital business environment, businesses focus on staying agile and innovative to compete, grow, and thrive. That puts DevOps front and center in digital business strategy as companies seek simple, streamlined ways to develop, deploy, change, and manage applications. The ADC is critical in enabling the full speed and agility that DevOps makes possible.

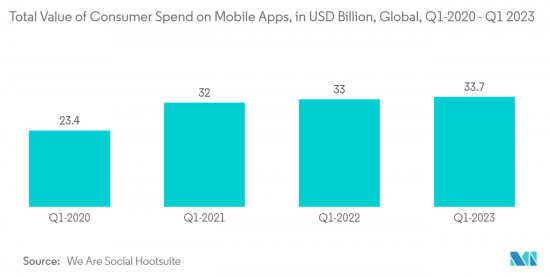

- Moreover, We Are Social and Hootsuite data indicates that consumer spending on mobile applications grew over the past few years, starting at USD 3.7 billion till quarter-one 2023, which is accelerating the demand for the ADC with features that enhance the performance of applications.

- With organizations focusing on extracting greater value from their growing data volumes, market vendors are introducing scalable, secure, and cost-effective modern ADC solutions. For instance, in May 2021, Array Network announced a software version (version 10.2.x) and innovative hardware platforms (the x800 Series) for its APV Series application performance controllers. APV x800 Series physical appliances (APV1800, 2800, 5800, etc.) offer production across multiple metrics, 40 Gig-E interfaces, and improved SSL performance.

- More users are surfing the web on smartphones, tablets, and other mobile devices compared to a laptop or desktops, resulting in the generation of large amounts of data. According to the GSM Association, by 2025, the United States is expected to have the highest smartphone adoption globally.

- Market vendors continuously invest in R&D activities to introduce innovative product offerings to gain more market presence and customer base. For instance, in August 2022, F5 announced the launch of a new traffic management and security solution designed to offer better control over its customers' fleets of NGINX instances. The newly launched F5 NGINX Management Suite 1.0 comes with a centralized dashboard to provide high visibility and control of NGINX instances, application programming interface (API) management workflows, application delivery services, and security solutions.

Asia-Pacific To Hold Significant Market Growth

- In Asia-Pacific, the hyper-connectivity environment has reinforced the importance of telcos, which play a foundational role in supporting consumers' and enterprises' connectivity and collaboration needs. Across Asia-Pacific, 75% of the operators registered positive revenue growth. South Korea is second only to Hong Kong in the world rankings of telecom market maturity.

- The need for data centers is increasing significantly and placing a greater emphasis on effectiveness and low latency. China and India are putting much effort into overtaking their competitors globally in constructing data centers, which is generating a booming demand for processing capacity as larger organizations attempt to scale up their data centers to assure the stability and reliability of data services.

- The South Korean government employed cloud computing technologies to enhance its banking on the country's super-fast internet connectivity, e-government services, and stable long-term evolution (LTE) availability. This is expected to contribute to the market's growth positively over the forecast period.

- Owing to technological advancements, there is an increase in the number of connected devices in the studied market. Moreover, strong government backing and substantial private sector investment are behind the growth of China's cloud computing industry. Furthermore, 5G and 5 G-enabled devices will exponentially increase the devices' interconnectivity. As a result, it increases connected devices, thereby directly augmenting the need for controlling the data traffic and security of the cloud-based applications.

- As financial organizations are increasingly adopting hybrid cloud, public cloud, and multi-cloud strategies to meet the need for compliance, competition, and modernization, the demand for networking solutions is anticipated to grow in the coming years. According to F5's State of Application Strategy Report- Financial Services Edition for 2022, 69% of financial services organizations in the Asia Pacific region have deployed multi-cloud strategies.

- In addition, the increasing internet users and data traffic in countries like China, India, and Indonesia are further augmenting the growth of ADC solutions in the region. With the evolving digital era, market vendors are offering more innovative network solutions and products for end-users, ensuring they have the best technology experience driving the market segment.

- For instance, in June 2022, Cyber security and application delivery solutions provider Radware and managed security service provider OneSecure announced the expansion of their collaboration agreement. In order to enhance OneSecure's Webyith defacement and domain phishing monitoring service for the ASEAN enterprises, the MSSP announced to expand of the cyber security suite to include Radware's Application Protection-as-a-service offering and cloud-distributed denial-of-service (DDoS) protection service.

Data Center Networking Industry Overview

The global data center networking market exhibits a notable degree of fragmentation, characterized by a competitive landscape that has intensified in recent years. Key industry players, including Extreme Networks Inc., Dell EMC, and VMware, Inc., among others, have solidified their positions and demonstrated substantial market shares. These major players are actively concentrating on expanding their customer base across various regions. To achieve this goal, they employ strategic collaborative initiatives designed to bolster their market share and enhance overall profitability.

In November 2022, VMware, Inc. introduced its cutting-edge SD-WAN solution, which encompasses a novel SD-WAN Client. This innovation aims to assist enterprises in delivering applications, data, and services securely, reliably, and efficiently across diverse networks to any device.

In September 2022, AppViewX, a prominent player specializing in automated machine identity management (MIM) and application infrastructure security, made a significant announcement. The company joined F5's Technology Alliance Program (TAP), ushering in a partnership that is expected to jointly promote enterprise application security and delivery solutions. This collaboration focuses on the management of applications and the enhancement of cybersecurity measures across on-premises, cloud, and edge locations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need of Cloud Storage and Rsing Demand for Reliable Application Performance

- 4.2.2 Increasing Cyberattacks Among Enterprises

- 4.3 Market Restraints

- 4.3.1 Increasing Network Complexity

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 Impact

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 By Product

- 5.1.1.1 Ethernet Switches

- 5.1.1.2 Router

- 5.1.1.3 Storage Area Network (SAN)

- 5.1.1.4 Application Delivery Controller (ADC)

- 5.1.1.5 Other Networking Equipment

- 5.1.2 By Services

- 5.1.2.1 Installation & Integration

- 5.1.2.2 Training & Consulting

- 5.1.2.3 Support & Maintenance

- 5.1.1 By Product

- 5.2 End-User

- 5.2.1 IT & Telecommunication

- 5.2.2 BFSI

- 5.2.3 Government

- 5.2.4 Media & Entertainment

- 5.2.5 Other End-Users

- 5.3 Region

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East

- 5.3.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Extreme Networks Inc.

- 6.1.2 Dell EMC

- 6.1.3 Vmware, Inc.

- 6.1.4 Huawei Technologies Co. Ltd.

- 6.1.5 Juniper Networks Inc.

- 6.1.6 Arista Networks Inc.

- 6.1.7 NEC Corporation

- 6.1.8 HP Development Company, L.P.

- 6.1.9 Fortinet, Inc.

- 6.1.10 Array Networks, Inc.

- 6.1.11 Radware Corporation

- 6.1.12 A10 Networks, Inc.

- 6.1.13 Moxa Inc.

- 6.1.14 Lenovo Group Limited

- 6.1.15 Broadcom Corporation

- 6.1.16 H3C Holding Limited

- 6.1.17 NVIDIA (Cumulus Networks Inc.)

- 6.1.18 Cisco Systems Inc.

- 6.1.19 F5 Networks Inc.