|

市場調査レポート

商品コード

1408367

住宅ローン-市場シェア分析、産業動向・統計、2024~2029年の成長予測Home Loan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 住宅ローン-市場シェア分析、産業動向・統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

住宅ローン市場は、今年度13兆米ドルの収益を上げており、予測期間のCAGRは9%に達する見込みです。

住宅ローン市場は、経済状況、規制の枠組み、文化的要因、住宅市場力学の違いにより、地域によって異なります。新興経済諸国は住宅ローン市場があまり発達していないかもしれないが、先進諸国は銀行システムが充実しており、住宅ローン市場が確立されていることが多いです。世界の銀行を含む商業銀行は、住宅ローン市場で重要な役割を果たしています。これらの銀行は、借り手に様々な住宅ローン商品やサービスを提供しています。

銀行以外の金融機関や住宅ローン専門の貸金業者も住宅ローン市場に参加しています。これらの金融機関は、住宅ローンの貸し出しのみに重点を置いていることが多く、より専門的なローン商品を提供している場合もあります。多くの国では、政府系企業や政府系機関が住宅ローンの融資を促進しています。米国のFannie MaeやFreddie Macなどがその例です。

金融技術の台頭により、住宅ローンの代替供給源としてオンラインレンダーが台頭してきました。これらのデジタルプラットフォームは、便利で多くの場合合理化された申込プロセスを提供しています。金利の変動は住宅ローン市場に大きな影響を与えます。低金利は借り入れを刺激し、高金利は借り入れを抑制する傾向があります。雇用率、インフレ率、GDP成長率などの経済要因は、住宅ローンの需要全体に影響を与えます。雇用が安定し景気が堅調であれば、住宅や住宅ローンに対する需要が高まることが多いです。

住宅市場、住宅ローン融資、金利に関連する政府の政策と政策は、世界の住宅ローン市場に大きな影響を与える可能性があります。住宅取得の促進や融資慣行の規制を目的とした政策は、市場力学に影響を与える可能性があります。不動産価格や住宅供給など不動産市場の状況は、住宅ローン市場において極めて重要な役割を果たします。市場の状況は、値ごろ感や借り手の需要に影響を与える可能性があります。

COVID-19の大流行は市場に大きな変動と不確実性をもたらしました。住宅市場は変動を経験し、その影響は地域の状況によって様々でした。住宅販売や建設活動が減速した地域もあれば、在宅勤務の変化により住宅需要が増加した地域もあった。

住宅ローン市場動向

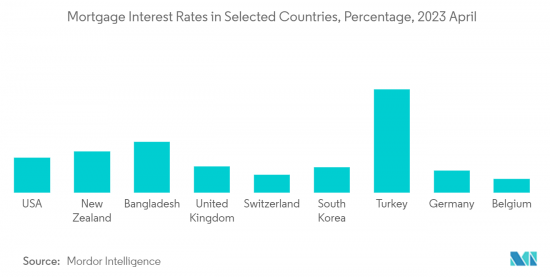

トルコの住宅ローン金利が最も高い

トルコは住宅ローン金利が最も高く、これは同国の住宅ローン市場と不動産セクター全体に大きな影響を与えると思われます。トルコでは国有銀行が住宅金融市場を独占してきました。住宅ローン金利と住宅価格は、間違いなくあらゆる住宅市場にとって極めて重要な要素であり、住宅需給を牽引する要因です。世界の原材料の高騰と供給問題により、建設セクターは鈍化する一方、価格は劇的に上昇しました。トルコの住宅ローン金利は、プライマリーとセカンダリーモーゲージ市場の規模において世界の主要国である米国の平均金利の4倍です。一方、トルコのGDPに占める住宅ローン市場のシェアは、住宅ローン制度が発達している他国に比べて低すぎる。

ほとんどの国で住宅価格が所得を上回るスピードで上昇。

急速な都市化と特定地域の人口増加により、住宅需要が増加しています。この需要の増加は、限られた土地の利用可能性や規制上の制約と相まって、価格の上昇につながった。多くの国で低金利が持続しているため、借入がより手ごろになり、住宅需要が増加しています。この需要増は、特に供給が限られている地域では、価格を押し上げる可能性があります。不動産はしばしば魅力的な投資オプションとみなされ、住宅市場への投資や投機の増加につながります。これは、特に人気のある場所や望ましい場所での価格を押し上げる可能性があります。ゾーニング、土地利用、建設許可、税制に関連する政府の政策や規制は、住宅供給や値ごろ感に影響を与える可能性があります。場合によっては、こうした政策が所得に対する価格上昇の一因となることもあります。

住宅ローン業界概要

世界の住宅ローン市場は競争が激しく、多数の参入企業が市場シェアを争っています。市場の競合情勢は、金融機関の規模や財務体質、市場での存在感、商品内容、顧客サービス、技術力など様々な要因に影響されます。市場参入企業は、競合金利、柔軟な条件、効率的なプロセス、個別化された顧客体験を提供することで、常に差別化を図っています。当レポートでは、住宅ローン市場の完全な背景分析(経済評価、市場概要、主要セグメントの市場規模推定、市場の新興動向、市場力学、主要企業のプロファイルなど)を掲載しています。住宅ローン市場は、Bank of America Corporation、Charles Schwab &Co.、Citigroup, Inc.、Dewan Housing Finance Corporation Limited、Goldman Sachs(Marcus)、HSBC Group、JPMorgan Chase &Co.、LIC Housing Finance Limited、Morgan Stanley、Wells Fargo &Co.などのトップ企業が提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 不動産市場の動向

- 政府の政策

- 市場抑制要因

- 住宅ローンの金利

- 市場のボラティリティと不確実性

- 市場を形成する様々な規制動向に関する洞察

- 市場における技術の影響に関する洞察

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 目的別

- 住宅購入

- 借り換え

- 住宅リフォーム

- 建設

- その他

- エンドユーザー別

- 被雇用者

- 専門職

- 学生

- 起業家

- その他(主婦、失業者、退職者など)

- 勤続年数別

- 5年以下

- 6~10年

- 11~24年

- 25~30年

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- その他の南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- オランダ

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- シンガポール

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- Market Concetration Overview

- 企業プロファイル

- Bank of America Corporation

- Charles Schwab & Co.

- Citigroup, Inc.

- Dewan Housing Finance Corporation Limited

- Goldman Sachs(Marcus)

- HSBC Group

- JPMorgan Chase & Co.

- LIC Housing Finance Limited

- Morgan Stanley

- Wells Fargo & Co.*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

Home Loan Market has generated a revenue of USD 13000 billion in the current year and is poised to achieve a CAGR of 9% for the forecast period. The home loan market varies across regions due to differences in economic conditions, regulatory frameworks, cultural factors, and housing market dynamics. Developed countries often have well-established home loan markets with extensive banking systems, while emerging economies may have less developed mortgage markets. Commercial banks, including global banking institutions, play a significant role in the home loan market. They offer a range of mortgage products and services to borrowers.

Non-banking financial institutions and specialized mortgage lenders also participate in the home loan market. These lenders often focus solely on mortgage lending and may offer more specialized loan products. In many countries, government-sponsored enterprises or agencies facilitate home loan financing. Examples include Fannie Mae and Freddie Mac in the United States.

With the rise of financial technology, online lenders have emerged as alternative sources of home loans. These digital platforms provide convenient and often streamlined application processes. Changes in interest rates significantly impact the home loan market. Lower interest rates tend to stimulate borrowing activity, while higher rates can discourage borrowing. Economic factors such as employment rates, inflation, and GDP growth affect the overall demand for home loans. A robust economy with stable employment often increases demand for housing and home loans.

Government policies and regulations related to the housing market, mortgage lending, and interest rates can significantly impact the global home loan market. Policies aimed at promoting homeownership or regulating lending practices can influence market dynamics. The state of the real estate market, including property prices and housing supply, plays a crucial role in the home loan market. Market conditions can affect affordability and borrower demand.

The COVID-19 pandemic created substantial market volatility and uncertainty. Housing markets experienced fluctuations, with varying impacts depending on local conditions. Some regions witnessed a slowdown in home sales and construction activity, while others experienced increased demand for housing due to changing work-from-home dynamics.

Home Loan Market Trends

Turkey has the Highest Mortgage Interest Rate

Turkey had the highest mortgage interest rates, which would have significant implications for the home loan market and the overall real estate sector in the country. state-owned banks have dominated the housing finance market in Turkey. Mortgage interest rates and house prices are undoubtedly significantly essential elements of any housing market and driving housing demand and supply factors. Due to sharp increases in raw materials globally and also supply problems, the construction sector slowed down while prices increased dramatically. Mortgage interest rates in Turkey are average four times higher than those in the US, which is the leading country in terms of its primary and secondary mortgage market sizes globally. On the other hand, the mortgage market share in GDP is too low in Turkey compared to other countries with well-developed mortgage systems.

House Prices grew Faster than Incomes in Most of the Countries.

Rapid urbanization and population growth in certain areas have increased the demand for housing. This increased demand, coupled with limited land availability and regulatory constraints, lead to higher prices. Persistently low-interest rates in many countries have made borrowing more affordable, increasing demand for housing. This increased demand can drive up prices, especially in areas with limited supply. Real estate is often seen as an attractive investment option, leading to increased investment and speculation in the housing market. This can drive up prices, particularly in popular or desirable locations. Government policies and regulations related to zoning, land use, construction permits, and taxation can impact housing supply and affordability. In some cases, these policies may contribute to the rising prices relative to incomes.

Home Loan Industry Overview

The Global home loan market is highly competitive, with numerous players vying for market share. The competitive landscape of the market is influenced by various factors, including the size and financial strength of the institutions, their market presence, product offerings, customer service, and technological capabilities. Market participants continually strive to differentiate themselves by offering competitive interest rates, flexible terms, efficient processes, and personalized customer experiences. A complete background analysis of the Home Loan Market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles are covered in the report. Home Loan Market is offered by top companies such as Bank of America Corporation, Charles Schwab & Co., Citigroup, Inc., Dewan Housing Finance Corporation Limited, Goldman Sachs (Marcus), HSBC Group, JPMorgan Chase & Co., LIC Housing Finance Limited, Morgan Stanley, Wells Fargo & Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real Estate Market Trends

- 4.2.2 Government Policies

- 4.3 Market Restraints

- 4.3.1 Interest rates on Home Loans

- 4.3.2 Market Volatility and Uncertainty

- 4.4 Insights on Various Regulatory Trends Shaping the Market

- 4.5 Insights on impact of technology in the Market

- 4.6 Industry Attractiveness - Porters' Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Purpose

- 5.1.1 Home Purchase

- 5.1.2 Refinance

- 5.1.3 Home Improvement

- 5.1.4 Construction

- 5.1.5 Other

- 5.2 By End User

- 5.2.1 Employed Individuals

- 5.2.2 Professionals

- 5.2.3 Students

- 5.2.4 Entrepreneur

- 5.2.5 Others (Homemaker, Unemployed, Retired, etc.)

- 5.3 By Tenure

- 5.3.1 Less Than 5 years

- 5.3.2 6-10 years

- 5.3.3 11-24 years

- 5.3.4 25-30 years

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Colombia

- 5.4.2.4 Chile

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 UK

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Netherlands

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 Australia

- 5.4.4.5 Singapore

- 5.4.4.6 South Korea

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Egypt

- 5.4.5.3 UAE

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 Bank of America Corporation

- 6.2.2 Charles Schwab & Co.

- 6.2.3 Citigroup, Inc.

- 6.2.4 Dewan Housing Finance Corporation Limited

- 6.2.5 Goldman Sachs (Marcus)

- 6.2.6 HSBC Group

- 6.2.7 JPMorgan Chase & Co.

- 6.2.8 LIC Housing Finance Limited

- 6.2.9 Morgan Stanley

- 6.2.10 Wells Fargo & Co.*

7 MARKET OPPORTUNTIES AND FUTURE TRENDS

8 DISCLAIMER AND ABOUT US