|

|

市場調査レポート

商品コード

1408321

光音響イメージング:市場シェア分析、産業動向と統計、2024~2029年の成長予測Photoacoustic Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 光音響イメージング:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

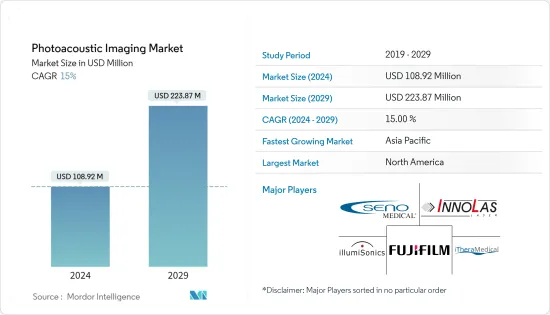

光音響イメージング市場規模は、2024年に1億892万米ドルと推定され、2029年には2億2,387万米ドルに達すると予測され、予測期間(2024~2029年)のCAGRは15%で成長します。

COVID-19パンデミックは当初、光音響イメージング市場に大きな影響を与えました。パンデミックは、COVID-19感染に関連する様々な調査目的での光音響イメージングの利用を増加させました。例えば、Journal of Sensorsが2023年3月に発表した論文によると、COVID-19ワクチン投与後の自己免疫疾患患者の炎症反応の研究に光音響イメージング法が使用された研究が行われました。このように、COVID-19の流行は市場の成長に大きな影響を与えました。しかし、パンデミックが沈静化するにつれて、本調査の予測期間中、市場はパンデミック以前の成長レベルを経験すると予想されます。

慢性疾患の有病率の上昇や研究調査における光音響イメージングの採用増加などの要因が市場成長を押し上げると見られています。

がんや心血管疾患などの慢性疾患の有病率の上昇は、市場成長を促進する重要な要因です。光音響イメージングがこれらの疾患の診断に使用されているからです。例えば、英国心臓財団が2023年に発表したデータによると、2022年に英国で心臓と循環器疾患が原因で入院した患者は推定110万人となります。したがって、このような慢性疾患の有病率の高さは、光音響イメージングシステムの利用を促進すると予想されます。

さらに、ACS Publicationsが2023年7月に発表した論文によると、光音響イメージングがin vivoでがんに関連するマイクロRNA-21と腫瘍組織をイメージングすることに成功したという研究があります。同様に、Experimental Biology and Medicine誌が2023年7月に発表した別の論文では、光音響イメージングが生体内の生理学的・形態学的情報を効果的に可視化することが示されています。このように、さまざまな調査における光音響システムの使用率が上昇していることも、市場成長を促進する大きな要因となっています。

さらに、市場の主要企業による新製品の発売や戦略的な活動が、調査市場の成長にプラスの影響を与えています。例えば、2022年6月、Seno MedicalのImagio Breast Imaging System(光音響イメージングシステム)は、米国食品医薬品局(FDA)のCenter for Devices and Radiological Health(CDRH)から市販前承認(PMA)を追認されました。このような製品承認により、同市場は予測期間中に大きく成長すると予想されます。

したがって、がんの有病率の上昇、光音響イメージングシステムの採用の増加、市場プレイヤによる戦略的活動の高まりなど、上記の要因によって、調査市場は分析期間中に成長すると予測されます。しかし、イメージングシステムの高コストと熟練した専門家の不足が市場成長を阻害する可能性が高いです。

光音響イメージング市場動向

がん領域は予測期間中に大幅な成長が見込まれる

光音響イメージングは、乳房や前立腺など様々な腫瘍の診断に広く利用されています。がんの有病率の上昇やがん診断のための光音響イメージングの使用量の増加といった要因が、予測期間中の調査対象セグメントの成長を後押しすると予想されています。

例えば、2022年11月にIndian Journal of Medical Researchが発表した論文によると、インドではがん罹患率が2022年の146万人から2025年には157万人に増加すると推定されています。2022年の10万人当たりの粗発生率の全国平均は、男性で100.4、女性で95.6でした。したがって、がん有病率の上昇は、がん診断のための光音響イメージング装置の採用を増加させるため、このセグメントの成長を促進する重要な要因です。

さらに、Frontiers in Oncologyが2022年3月に発表した論文によると、光音響イメージング(PAI)は、がんの分子イメージングのための新たなモダリティであると言われており、前例のない時空間分解能で、光学コントラストによる内因性組織発色団の非侵襲的評価を可能にしています。この情報源はまた、マウスモデルでの前臨床研究により、PAIは放射線治療や化学放射線治療に対する反応を評価するために使用できることが示されたと述べています。PAIは腫瘍の血管アーキテクチャと血中酸素飽和度の変化に基づいており、腫瘍の低酸素状態と密接に関連しています。このため、がん診断における光音響イメージングの利用が増加しており、同分野の成長を牽引すると期待されています。

したがって、がん分野は、がんの有病率上昇やがん診断のための光音響イメージング利用といった上述の要因によって、予測期間中に大きな成長を示すことが期待されます。

予測期間中、北米が市場で大きなシェアを占める見込み

北米は市場で大きなシェアを占めると予想されます。これは、技術的に高度な製品が容易に入手可能であることや、光音響イメージングシステムの採用が増加していることなどの要因によるものです。さらに、がんや心血管疾患などの慢性疾患の有病率の上昇や高齢者人口の増加も北米市場の成長に寄与する主要因の一つです。

例えば、2022年7月にカナダ健康情報研究所が更新したデータによると、2022年には約240万人のカナダ人が心臓病を患っていると推定されています。このように、国全体で慢性疾患の負担が増加していることから、このセグメントは力強い成長が見込まれています。これは、診断のための光音響イメージング装置の採用増加につながると思われます。

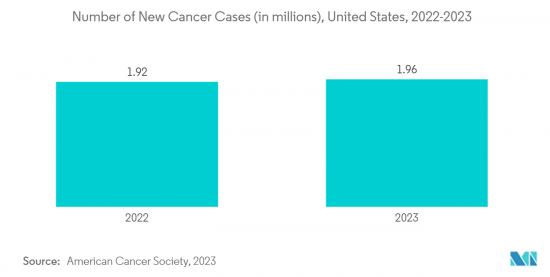

さらに、National Breast Cancer Foundation Inc.が2022年6月に発表したデータによると、2022年に米国の女性で浸潤性乳がんの新規症例が28万7,500例、非浸潤性乳がんの新規症例が5万1,400例と推定されると言及しています。さらに、2023年に発表された米国がん学会のデータによると、大腸がんは米国の男女で最も多く診断されるがんの一つです。2023年には米国で約10万6,970例の結腸がんと4万6,050例の直腸がんが診断されると推定されています。したがって、このような疾患の有病率の上昇は、光音響イメージングシステムの採用を後押しすると予想されます。

従って、様々な慢性疾患の高い有病率などの上記の要因によって、調査された市場の成長は北米地域で予測されます。

光音響イメージング産業概要

光音響イメージング市場は、世界的と地域的に事業を展開する複数の企業が存在するため、半統合状態にあります。競合情勢には、市場シェアを持ち知名度の高い国際企業や地元企業の分析が含まれます。主要市場参入企業としては、illumiSonics Inc.、Seno Medical、InnoLas Laser GmbH、Fujifilm Holdings Corporation(Fujifilm Visualsonics, Inc.)、Kibero、iThera Medical GmbHなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の有病率の上昇

- 調査研究における光音響イメージングの採用増加

- 市場抑制要因

- イメージングシステムの高コストと熟練した専門家の不足

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- タイプ別

- イメージングシステム

- レーザー

- その他

- 製品タイプ別

- 光音響トモグラフィ

- 光音響顕微鏡

- 用途別

- 腫瘍学

- 循環器

- 血液学

- その他の用途

- エンドユーザー別

- 病院

- 診断センター

- 学術研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- その他

- 北米

第6章 競合情勢

- 企業プロファイル

- illumiSonics Inc.

- Seno Medical

- InnoLas Laser GmbH

- Fujifilm Holdings Corporation(Fujifilm Visualsonics, Inc.)

- Kibero

- iThera Medical GmbH

- Photosound Technologies Inc.

- Advantest Corporation

- TomoWave Laboratories, Inc.

- Aspectus GmbH

- VibroniX

第7章 市場機会と今後の動向

The Photoacoustic Imaging Market size is estimated at USD 108.92 million in 2024, and is expected to reach USD 223.87 million by 2029, growing at a CAGR of 15% during the forecast period (2024-2029).

The COVID-19 pandemic had a substantial impact on the photoacoustic imaging market initially. The pandemic increased the usage of photoacoustic imaging for various research purposes related to COVID-19 infection. For instance, according to an article published by the Journal of Sensors in March 2023, a study was conducted where a photoacoustic imaging method was used for studying the inflammation responses in autoimmune disease patients after COVID-19 vaccine administration. Thus, the COVID-19 outbreak affected the market's growth significantly. However, as the pandemic subsided, the market is expected to experience pre-pandemic growth levels during the study's forecast period.

Factors such as the rising prevalence of chronic diseases and the increasing adoption of photoacoustic imaging in research studies are expected to boost market growth.

The rising prevalence of chronic diseases such as cancer and cardiovascular diseases is a significant factor driving the market growth. It is because photoacoustic imaging is used to diagnose these diseases. For instance, according to the data published by the British Heart Foundation in 2023, an estimated 1.1 million patients were admitted to hospitals in the United Kingdom due to heart and circulatory diseases in 2022. Thus, the high prevalence of such chronic diseases is expected to boost the usage of photoacoustic imaging systems.

Moreover, according to an article published by ACS Publications in July 2023, a study showed that photoacoustic imaging succeeded in imaging microRNA-21 and tumor tissues related to cancer in vivo. Similarly, in another article published by Experimental Biology and Medicine in July 2023, a study showed that photoacoustic imaging effectively visualizes physiological and morphological information in biological systems in vivo. Thus, the rising usage rate of photoacoustic systems in various research studies is also a significant factor driving market growth.

In addition, new product launches and strategic activities by major players in the market are positively affecting the growth of the studied market. For instance, in June 2022, Seno Medical's Imagio Breast Imaging System (a photoacoustic imaging system) received supplemental premarket approval (PMA) from the Center for Devices and Radiological Health (CDRH) of the United States Food & Drug Administration (FDA). Thus, owing to such product approvals, the studied market is expected to grow significantly over the forecast period.

Therefore, owing to the factors mentioned above, such as the rising prevalence of cancer, the increasing adoption of photoacoustic imaging systems, and the rising strategic activities by market players, the studied market is anticipated to grow over the analysis period. However, the high cost of imaging systems and the lack of skilled professionals likely impede market growth.

Photoacoustic Imaging Market Trends

Oncology Segment is Expected to Witness Significant Growth Over the Forecast Period

Photoacoustic imaging is widely used to diagnose various tumors, such as breast and prostate. Factors such as the rising prevalence of cancer and the increasing usage of photoacoustic imaging for cancer diagnosis are expected to boost the growth of the studied segment during the forecast period.

For instance, according to an article published by the Indian Journal of Medical Research in November 2022, it was estimated in India, the incidence of cancer cases would likely increase from 1.46 million in 2022 to 1.57 million in 2025. The national average for 2022 crude incidence rate per 100,000 was 100.4 for males and 95.6 for females. Thus, the rising prevalence of cancer is a significant factor driving the segment's growth, as it would increase the adoption of photoacoustic imaging devices for cancer diagnosis.

Moreover, according to an article published by Frontiers in Oncology in March 2022, photoacoustic imaging (PAI) is said to be an emerging modality for molecular imaging of cancer, enabling non-invasive assessment of endogenous tissue chromophores with optical contrast at unprecedented spatiotemporal resolution. The source also stated that preclinical studies in mouse models showed that PAI could be used to assess response to radiotherapy and chemoradiotherapy. It is based on changes in the tumor vascular architecture and blood oxygen saturation, closely linked to tumor hypoxia. Thus, the rising usage of photoacoustic imaging for cancer diagnosis is expected to drive segment growth.

Therefore, the oncology segment is expected to witness significant growth over the forecast period due to the abovementioned factors, such as cancer's rising prevalence and photoacoustic imaging usage for diagnosing cancer.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant share of the market. It is due to factors such as the easy availability of technologically advanced products and the increase in the adoption of photoacoustic imaging systems. Moreover, the rising prevalence of chronic diseases such as cancer and cardiovascular disorders and the increasing geriatric population in the region are also among the key factors contributing to the growth of the studied market in North America.

For instance, according to the data updated by the Canadian Institute for Health Information in July 2022, it was estimated that about 2.4 million Canadians had heart disease in 2022. Thus, with the increasing burden of chronic diseases across the country, the segment is expected to grow strongly. It would lead to increased adoption of photoacoustic imaging devices for diagnosis.

Moreover, as per the National Breast Cancer Foundation Inc., data published in June 2022 mentioned that in 2022 an estimated 287,500 new cases of invasive breast cancer and 51,400 new cases of non-invasive breast cancer were diagnosed in women in the United States in 2022. Moreover, according to the American Cancer Society data published in 2023, colorectal cancer is one of the most common cancers diagnosed in men and women in the United States. It is estimated that approximately 106,970 cases of colon cancer and 46,050 cases of rectal cancer will be diagnosed in the United States in 2023. Thus, the rising prevalence of such diseases is expected to boost the adoption of photoacoustic imaging systems.

Therefore, owing to the factors above, such as the high prevalence of various chronic diseases, the growth of the studied market is anticipated in the North American region.

Photoacoustic Imaging Industry Overview

The photoacoustic market is semi consolidated due to the presence of several companies operating globally as well as regionally. The competitive landscape includes analyzing a few international and local companies that hold market shares and are well known. Some of the key market players include illumiSonics Inc., Seno Medical, InnoLas Laser GmbH, Fujifilm Holdings Corporation (Fujifilm Visualsonics, Inc.), Kibero, and iThera Medical GmbH, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic Diseases

- 4.2.2 Increasing Adoption of Photoacoustic Imaging in Research Studies

- 4.3 Market Restraints

- 4.3.1 High Cost of the Imaging Systems and Lack of Skilled Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Type

- 5.1.1 Imaging Systems

- 5.1.2 Lasers

- 5.1.3 Others

- 5.2 By Product Type

- 5.2.1 Photoacoustic Tomography

- 5.2.2 Photoacoustic Microscopy

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Cardiology

- 5.3.3 Hematology

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Centers

- 5.4.3 Academic and Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 illumiSonics Inc.

- 6.1.2 Seno Medical

- 6.1.3 InnoLas Laser GmbH

- 6.1.4 Fujifilm Holdings Corporation (Fujifilm Visualsonics, Inc.)

- 6.1.5 Kibero

- 6.1.6 iThera Medical GmbH

- 6.1.7 Photosound Technologies Inc.

- 6.1.8 Advantest Corporation

- 6.1.9 TomoWave Laboratories, Inc.

- 6.1.10 Aspectus GmbH

- 6.1.11 VibroniX