光音響トモグラフィーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Photoacoustic Tomography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740765

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

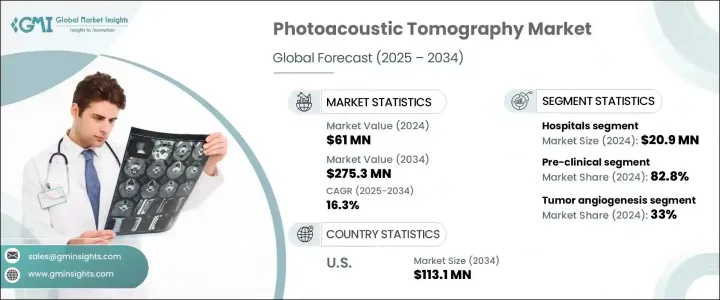

光音響トモグラフィーの世界市場は、2024年に6,100万米ドルと評価され、CAGR16.3%で成長し、2034年までには2億7,530万米ドルに達すると予測されています。

この目覚ましい成長は、深部組織の詳細な画像を生成する技術の能力によって促進され、PATが医療画像診断における有望なツールとして確立されました。イメージング技術の進歩に伴い、PATの臨床および前臨床応用の可能性は急速に拡大しています。正確な診断ツール、特にがん検出やその他の重要な健康状態に対する需要の高まりが、市場成長を促進する重要な要因となっています。さらに、ヘルスケア専門家も患者も、従来の方法と比較して不快感や回復時間を最小限に抑える非侵襲的イメージングソリューションを優先する傾向が強まっています。このような患者中心のヘルスケアへの注目の高まりは、様々な医療分野での光音響トモグラフィーの採用を加速させると予想されます。また、研究者は早期診断や個別化治療への応用を模索しており、アクセシビリティと精度の両方を向上させるイノベーションに貢献しています。

非侵襲的診断技術へのシフトは、特にがんのような疾患の早期発見の必要性が高まるにつれて、ヘルスケアの状況を一変させつつあります。患者は、よりリスクが少なく、より快適な、より高度な方法を求めており、PATは理想的なソリューションとなっています。早期診断の重要性に対する世界の認識が高まるにつれ、このような画像技術の研究開発への投資も増加しています。このような技術革新への注目の高まりは、PATの精度を高めるだけでなく、臨床および前臨床での使用事例を拡大しています。個別化治療と疾病の早期発見に対する需要は、最も治療可能な段階で健康状態を特定できる技術に対する持続的な推進力を生み出しています。さらに、光音響トモグラフィーは、治療効果をモニタリングする貴重なツールとして検討されており、臨床と研究の両分野での採用をさらに後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 6,100万米ドル |

| 予測金額 | 2億7,530万米ドル |

| CAGR | 16.3% |

市場は臨床試験と前臨床試験に区分され、2024年には前臨床試験が市場全体の82.8%を占めて市場をリードしました。これらの研究は、診断ツールや治療法などの新しい医療技術を臨床試験に導入する前に試験・開発する上で重要な役割を果たしています。前臨床研究は、制御された環境下でこれらの技術の安全性と有効性を保証するものであり、後期段階の開発に関連するリスクを最小限に抑えるために極めて重要です。製薬、バイオテクノロジー、医療機器産業が拡大を続ける中、前臨床研究の需要は拡大すると予想され、医療イノベーションを推進する上でこれらの研究の重要性が増しています。

光音響トモグラフィー市場には、アプリケーションの観点から、脳機能イメージング、腫瘍血管新生、血液酸素化マッピング、皮膚黒色腫検出などが含まれます。このうち、腫瘍血管新生は2024年に33%を占め、最大の市場シェアを占めました。腫瘍血管新生は、腫瘍がその成長を促進するために新しい血管を発達させるプロセスであり、がん研究の重要な分野です。PATは、血管構造のリアルタイム可視化を可能にし、腫瘍の早期発見と継続的モニタリングに不可欠な知見を臨床医に提供します。この機能によりPATは、早期発見が治療成績を向上させる鍵となるがんとの闘いにおいて不可欠なツールとなります。

米国の光音響トモグラフィー市場は、2034年までに1億1,310万米ドルに達すると予測されています。この成長の原動力となっているのは、技術の絶え間ない進歩と、患者中心のケアの重視の高まりです。米国の主要研究機関は、特にがんのような生命を脅かす疾患に対して、PATを使用して早期診断を強化する新しい方法を継続的に模索しています。このような技術革新により、光音響トモグラフィーはより正確で適応性の高いものとなり、治療モニタリングと患者ケアの向上に焦点が当てられています。非侵襲的診断ツールへの関心の高まりは、ヘルスケア現場におけるPATの普及をさらに後押ししています。

光音響トモグラフィーの世界市場における主要企業は、Fujifilm VisualSonics、Advantest、Vibronix、Aspectus、iThera Medical、Kibero、Seno Medical Instruments、TomoWaveなどです。これらの企業は研究開発に積極的に投資し、製品に磨きをかけ、光音響トモグラフィーの可能性を広げています。学術・研究機関との戦略的パートナーシップや協力関係も、これらの企業の戦略の中心であり、新たな動向を先取りし、PATの臨床応用を強化するのに役立っています。世界なリーチを拡大し、最先端の製品を導入することで、これらの業界リーダーは、市場の急成長を生かすべく自らを位置づけています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 非侵襲性画像診断技術の需要増加

- 慢性疾患の増加

- 光音響トモグラフィーにおける技術の進歩

- 病気の早期発見への関心の高まり

- 業界の潜在的リスク・課題

- 光音響イメージングシステムの高コスト

- 新興諸国における熟練したヘルスケア従事者の不足

- 成長促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:研究タイプ別、2021年~2034年

- 主要動向

- 臨床研究

- 前臨床研究

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 機能的脳画像

- 腫瘍血管新生

- 血液酸素化マッピング

- 皮膚メラノーマの検出

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 画像診断センター

- 学術調査室

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Advantest

- Aspectus

- Fujifilm VisualSonics

- iThera Medical

- Kibero

- Seno Medical Instruments

- TomoWave

- Vibronix

目次

The Global Photoacoustic Tomography Market was valued at USD 61 million in 2024 and is estimated to grow at a 16.3% CAGR to reach USD 275.3 million by 2034. This impressive growth is fueled by the technology's ability to produce detailed images of deep tissues, establishing PAT as a promising tool in medical imaging. As imaging technology continues to advance, PAT's potential for both clinical and pre-clinical applications is expanding rapidly. The increasing demand for accurate diagnostic tools, especially for cancer detection and other critical health conditions, is a key factor driving market growth. Additionally, healthcare professionals and patients alike are increasingly prioritizing non-invasive imaging solutions, which minimize discomfort and recovery times compared to traditional methods. This growing focus on patient-centered healthcare is expected to accelerate the adoption of photoacoustic tomography across various medical fields. Researchers are also exploring its applications in early diagnosis and personalized treatment, contributing to innovations that improve both accessibility and accuracy.

The shift towards non-invasive diagnostic techniques is transforming the healthcare landscape, particularly as the need for early detection of diseases like cancer becomes more pressing. Patients are demanding more advanced methods that offer less risk and greater comfort, making PAT an ideal solution. As the global awareness of the importance of early diagnosis increases, so does the investment in research and development for such imaging technologies. This growing focus on innovation is not only making PAT more precise but also expanding its clinical and pre-clinical use cases. The demand for personalized treatment and early disease detection is creating a sustained drive for technologies that can identify health conditions at their most treatable stages. Moreover, photoacoustic tomography is being explored as a valuable tool in monitoring treatment effectiveness, further pushing its adoption in both clinical and research settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61 Million |

| Forecast Value | $275.3 Million |

| CAGR | 16.3% |

The market is segmented into clinical and pre-clinical studies, with pre-clinical studies leading the market in 2024, accounting for 82.8% of the total market share. These studies play a critical role in testing and developing new medical technologies, including diagnostic tools and therapies, before they are introduced to clinical trials. Pre-clinical research ensures the safety and efficacy of these technologies in controlled environments, which is crucial for minimizing the risks associated with later-stage development. As the pharmaceutical, biotechnology, and medical device industries continue to expand, the demand for pre-clinical studies is expected to grow, reinforcing the importance of these studies in advancing medical innovation.

In terms of application, the photoacoustic tomography market includes functional brain imaging, tumor angiogenesis, blood oxygenation mapping, skin melanoma detection, and more. Among these, tumor angiogenesis represented the largest market share in 2024, holding 33%. Tumor angiogenesis, the process by which tumors develop new blood vessels to fuel their growth, is a critical area of cancer research. PAT offers a significant advantage here, enabling real-time visualization of blood vessel structures and providing clinicians with essential insights for early tumor detection and ongoing monitoring. This capability makes PAT an indispensable tool in the fight against cancer, where early detection is key to improving treatment outcomes.

The U.S. Photoacoustic Tomography Market is projected to reach USD 113.1 million by 2034. This growth is driven by continuous advancements in technology and an increasing emphasis on patient-centered care. Leading research institutions in the U.S. are continuously exploring new ways to enhance early diagnosis using PAT, particularly for life-threatening conditions like cancer. These innovations are making photoacoustic tomography more precise and adaptable, with a focus on improving treatment monitoring and patient care. The growing interest in non-invasive diagnostic tools further supports the widespread adoption of PAT in healthcare settings.

Key players in the Global Photoacoustic Tomography Market include Fujifilm VisualSonics, Advantest, Vibronix, Aspectus, iThera Medical, Kibero, Seno Medical Instruments, and TomoWave. These companies are actively investing in research and development to refine their offerings and expand the potential of photoacoustic tomography. Strategic partnerships and collaborations with academic and research institutions are also central to these companies' strategies, helping them stay ahead of emerging trends and strengthen the clinical applications of PAT. By expanding their global reach and introducing cutting-edge products, these industry leaders are positioning themselves to capitalize on the rapid growth of the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for non-invasive imaging techniques

- 3.2.1.2 Growing prevalence of chronic diseases

- 3.2.1.3 Technological advancement in photoacoustic tomography

- 3.2.1.4 Rising preference for early disease detection

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of photoacoustic imaging system

- 3.2.2.2 Shortage of skilled healthcare professionals in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Study Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical study

- 5.3 Pre-clinical study

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Functional brain imaging

- 6.3 Tumour angiogenesis

- 6.4 Blood oxygenation mapping

- 6.5 Skin melanoma detection

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic imaging centers

- 7.4 Academic and research laboratories

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Advantest

- 9.2 Aspectus

- 9.3 Fujifilm VisualSonics

- 9.4 iThera Medical

- 9.5 Kibero

- 9.6 Seno Medical Instruments

- 9.7 TomoWave

- 9.8 Vibronix

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日