|

市場調査レポート

商品コード

1408189

航空機用熱交換器:市場シェア分析、産業動向と統計、2024~2029年の成長予測Aircraft Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用熱交換器:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

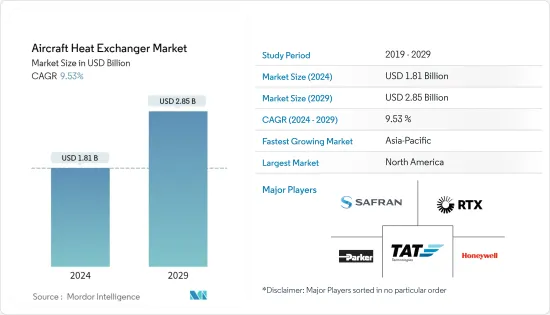

航空機用熱交換器の市場規模は2024年に18億1,000万米ドルと推定され、2029年には28億5,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは9.53%で成長する見込みです。

主なハイライト

- 世界の航空機用熱交換器市場は、COVID-19の大流行によりかつてない課題を目の当たりにしました。航空会社は、空港の閉鎖、航空交通量の減少、サプライチェーンの混乱による原材料の不足、整備・修理・オーバーホール作業の遅延により、莫大な損失に直面していました。軍事用途の航空機用熱交換器の研究開発(R&D)は、労働力不足のために妨げられていました。しかし、COVID後は、航空機納入の増加と航空機の整備・修理・オーバーホール(MRO)への支出の増加により、市場は力強い回復を見せた。

- 航空機用熱交換器は、航空機のエンジン、環境制御システム、航空電子機器に使用され、熱を制御してこれらのシステムの温度を維持するのに役立ちます。油圧作動油の冷却にも使用され、燃料タンク内に設置されています。熱交換器は、固定翼や回転翼を含むあらゆるタイプの航空機で使用されており、さまざまな航空機システムで使用されています。

- 先進的な航空機用熱交換器は、熱力学的効率を高めるため、チューブやフィンといった肉厚の薄い部品で構成されています。これらのシステムは、高温用途向けにアルミニウム、銅、チタンなどの耐熱金属で構成されています。航空交通量の増加、先進的な航空機用熱交換器の調達に対する支出の増加、世界の航空機保有台数の増加が市場の成長を促進しています。

航空機用熱交換器の市場動向

予測期間中、固定翼セグメントが最も高いCAGRで成長する見込み

- 固定翼セグメントは予測期間中に大きな成長を示すと予測されます。この成長は、航空交通量の増加、新しい航空機への需要の高まり、航空分野への支出の増加に起因しています。民間航空機の熱交換器は、エンジンのオイルシステムから熱を奪って冷たい燃料を加熱し、燃料効率を向上させるとともに、燃料に巻き込まれた水が部品内で凍結する可能性を低減します。したがって、民間航空機の納入台数の増加が予測期間中の市場成長を促進すると予測されます。国際航空運送協会(IATA)によると、全体の航空旅客数は2024年に40億人に達します。さらに、ボーイングはCMO(Commercial Market Outlook)2022を発表し、その中で2022年から2041年の間に新型航空機の需要が41,000機を超えると予測しています。

- さらに、軍用機の需要が増加し、空軍の能力強化に向けた支出が増加することで、先進的な航空機用熱交換器システムの需要が生まれています。例えば、2023年1月、エアロブレイズ・エンジニアード・テクノロジーズ・オクラホマシティは、ティンカー空軍基地でF-16戦闘機の再生熱交換器の再製造に関する米国空軍(USAF)との5年契約を締結しました。このように、固定翼機の納入数の増加とMRO事業への支出の増加が市場の成長を後押ししています。

アジア太平洋地域が予測期間中に最も高い成長を示す

- アジア太平洋地域は予測期間中に最も高い成長を示すと予測されています。航空セクターへの支出の増加と、特に中国とインドからの新しい航空機に対する需要の増加が、この地域の市場成長を後押ししています。国際航空運送協会(IATA)によると、中国は2022年に米国を抜いて世界最大の航空市場になります。さらに、中国は2036年までに航空旅客数が15億人に達すると予想されています。また、インド民間航空省は、2021年にインドが国内航空市場第3位になったと発表しました。

- さらに、インド、中国、日本による防衛費の増大と次世代戦闘機の調達が市場の成長を後押ししています。中国とインドは世界第2位と第3位の防衛支出国であり、防衛予算はそれぞれ2,930億米ドルと766億米ドルです。例えば、2022年2月、Bharat Heavy Electricals Limited(BHEL)は、Hindustan Aeronautics Limited(HAL)から、83機のLCA Tejas MK1A航空機用の小型熱交換器セットの供給を受注しました。このように、アジア諸国からの民間機や軍用機の需要の高まりが、市場の成長を後押ししています。

航空機用熱交換器産業の概要

航空機用熱交換器市場は適度に統合されており、少数のプレーヤーが市場で大きなシェアを占めています。著名な市場プレイヤーには、Safran SA、TAT Technologies Ltd.、RTX Corporation、Honeywell International Inc.、Parker Hannifin Corporationなどがいます。

市場の主なプレーヤーは、さまざまなタイプの航空機に対応する先進的な航空機用熱交換器の開発に注力しています。研究開発と新しい航空機用熱交換器のイントロダクションへの支出の増加は、今後数年間により良い機会を生み出すと思われます。例えば、ゼネラル・アトミクス航空システムズ社(GA-ASI)はコンフラックス・テクノロジー社と共同で、MQ-9B用の新しい燃料油熱交換器(FOHE)の設計と開発に取り組んでいます。GA-ASIはMQ-9B SkyGuardianおよびSeaGuardian遠隔操縦航空機用の強化された熱ソリューションを製造しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 板フィン

- フラットチューブ

- プラットフォーム

- 固定翼

- 回転翼

- 無人航空機(UAVs)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Safran SA

- RTX Corporation

- TAT Technologies Ltd.

- Honeywell International Inc.

- Parker Hannifin Corporation

- Triumph Group

- Wall Colmonoy Corporation

- Boyd Corporation

- IHI Corporation

- AMETEK, Inc.

第7章 市場機会と今後の動向

The Aircraft Heat Exchanger Market size is estimated at USD 1.81 billion in 2024, and is expected to reach USD 2.85 billion by 2029, growing at a CAGR of 9.53% during the forecast period (2024-2029).

Key Highlights

- The global aircraft heat exchanger market witnessed unprecedented challenges due to the COVID-19 pandemic. The airlines had faced huge losses due to airport shutdowns, reduced air traffic, and supply chain disruptions that had led to a shortage of raw materials and delayed maintenance, repair, and overhaul operations. Research and development (R&D) of aircraft heat exchangers for military applications had been hampered due to a shortage of labor force. However, the market had showcased a strong recovery post-COVID due to increased aircraft deliveries and rising spending on aircraft maintenance, repair, and overhaul (MRO).

- Aircraft heat exchangers are used in aircraft engines, environmental control systems, and avionics that help to control heat and maintain the temperature of these systems. These are used to cool down hydraulic fluid and are located inside the fuel tank. The heat exchangers are used in all types of aircraft, including fixed-wing and rotary, and in many different aircraft systems.

- Advanced aircraft heat exchangers consist of thin wall thickness components such as tubes and fins to increase their thermodynamic efficiency. These systems are made up of heat-resistant metals such as aluminum, copper, titanium, and others for high-temperature applications. Increasing air traffic, rising expenditure on the procurement of advanced aircraft heat exchangers, and growing aircraft fleets worldwide drive the growth of the market.

Aircraft Heat Exchanger Market Trends

The Fixed-Wing Segment is Anticipated to Grow with the Highest CAGR During the Forecast Period

- The fixed-wing segment is expected to show significant growth during the forecast period. The growth is attributed to the increasing air traffic, rising demand for new aircraft, and growing expenditure on the aviation sector. Commercial aircraft heat exchangers take heat from the engine's oil system to heat cold fuel, which improves fuel efficiency and reduces the possibility of water entrapped in the fuel freezing in components. Thus, increasing commercial aircraft deliveries is projected to drive market growth during the forecast period. According to the International Air Transport Association (IATA), the overall air passenger number will reach 4 billion in 2024. Furthermore, Boeing released its Commercial Market Outlook (CMO) 2022, in which it forecasted that demand for new aircraft will exceed 41,000 units during the 2022-2041 period.

- Additionally, increasing demand for military aircraft and growing expenditure in enhancing air force capabilities is creating demand for advanced aircraft heat exchanger systems. For instance, in January 2023, Aerobraze Engineered Technologies Oklahoma City signed a five-year contract with the United States Air Force (USAF) for the remanufacturing of F-16 fighter aircraft regenerative heat exchangers at the Tinker Air Force Base. Thus, growing fixed-wing aircraft deliveries and increasing spending on MRO operations boost the market growth.

Asia-Pacific Will Showcase Highest Growth During the Forecast Period

- Asia-Pacific is projected to show the highest growth during the forecast period. Growing expenditure on the aviation sector and growing demand for new aircraft, especially from China and India, boost the market growth across the region. According to the International Air Transport Association (IATA), China surpassed the United States and became the largest aviation market in the world in 2022. Furthermore, China is expected to reach a total of 1.5 billion aviation passengers by 2036. Also, the Indian civil aviation ministry announced that India became the third-largest domestic aviation market in 2021.

- Furthermore, growing defense expenditure and procurement of next-generation fighter jets from India, China, and Japan propel the growth of the market. China and India are the second and third largest defense spenders in the world, with a defense budget of USD 293 billion and USD 76.6 billion, respectively. For instance, in February 2022, Bharat Heavy Electricals Limited (BHEL) received a contract from Hindustan Aeronautics Limited (HAL) for the supply of compact heat exchanger sets for 83 LCA Tejas MK1A aircraft. Thus, the growing demand for commercial and military aircraft from Asian countries drives the growth of the market.

Aircraft Heat Exchanger Industry Overview

The aircraft heat exchangers market is moderately consolidated in nature, with few players holding significant shares in the market. Some prominent market players are Safran SA, TAT Technologies Ltd., RTX Corporation, Honeywell International Inc., and Parker Hannifin Corporation.

The key players in the market are focusing on the development of advanced aircraft heat exchangers for different types of aircraft. Growing expenditure on research and development and the introduction of new aircraft heat exchangers will create better opportunities in the coming years. For instance, General Atomics Aeronautical Systems Inc. (GA-ASI) is working in collaboration with Conflux Technology on the design and development of a new Fuel Oil Heat Exchanger (FOHE) for the MQ-9B. GA-ASI is manufacturing enhanced thermal solutions for its MQ-9B SkyGuardian and SeaGuardian remotely-piloted aircraft

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Plate-Fin

- 5.1.2 Flat Tube

- 5.2 Platform

- 5.2.1 Fixed-Wing

- 5.2.2 Rotary-Wing

- 5.2.3 Unmanned Aerial Vehicles (UAVs)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Safran SA

- 6.1.2 RTX Corporation

- 6.1.3 TAT Technologies Ltd.

- 6.1.4 Honeywell International Inc.

- 6.1.5 Parker Hannifin Corporation

- 6.1.6 Triumph Group

- 6.1.7 Wall Colmonoy Corporation

- 6.1.8 Boyd Corporation

- 6.1.9 IHI Corporation

- 6.1.10 AMETEK, Inc.