|

市場調査レポート

商品コード

1407082

キレート剤:市場シェア分析、産業動向・統計、2024~2029年成長予測Chelating Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キレート剤:市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

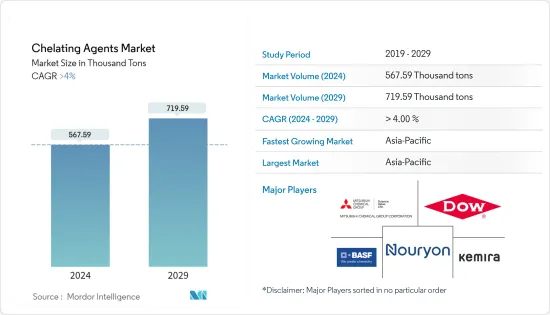

キレート剤の市場規模は2024年に56万7,590トンと推定され、2029年には71万9,590トンに達すると予測され、予測期間中(2024-2029年)のCAGRは4%以上で成長する見込みです。

市場は2020年のCOVID-19パンデミックによってマイナスの影響を受けました。2020年前半のCOVID-19の大流行により、紙パルプ産業はその成長率に大幅な下駄を履かされました。その結果、キレート剤の消費に不利な影響を与えました。現在、市場はパンデミックから回復しています。市場は2022年にパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

家庭用洗浄用途からのキレート剤需要の増加が、市場の成長を促進すると予想されます。

その反面、非生分解性キレート剤が環境に与える悪影響が、予測期間中の市場成長を抑制すると予想されます。

さらに、いくつかのエンドユーザー産業におけるグリーンキレート剤への需要の高まりは、将来的に世界市場に有利な成長機会をもたらすと思われます。

アジア太平洋地域が世界の市場を独占しており、中国、インド、日本などの国が最大の消費国となっています。

キレート剤市場の動向

洗浄用途でのキレート剤消費の増加

- キレート剤は主に洗浄用途で使用されます。キレート剤は、硬水に含まれるミネラルによる洗浄プロセスへの干渉を防ぐという重要な役割を果たすため、さまざまな洗浄剤に使用されています。

- 洗浄以外にも、キレート剤は、洗浄製品の保存性の向上、色の維持、抗菌効果の付与、ニッケルやクロムによるアレルギーの防止など、多くの利点を発揮します。

- 石鹸や洗剤に使用される場合、キレート剤は金属染みの防止や漂白剤の早期分解を促進します。一方、工業用洗浄液の製造に使用されるキレート剤は、機器の表面に付着した不溶性の塩分をほぐし、分解し、溶解することで、スケールや錆の除去を助ける。

- 個人および周辺空間の衛生維持に対する意識の高まりは、多くの世界の洗剤製造企業を刺激し、家庭用洗浄製剤の急増する需要を開拓しています。

- 例えば、2022年5月、AerialやTideなどのブランドを製造するプロクター・アンド・ギャンブル(P&G)は、ハイデラバードに液体洗剤製造工場を建設するために20億インドルピー(~2,652万米ドル)を投資しました。

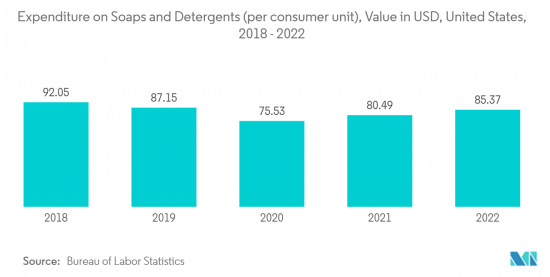

- 労働統計局によると、米国における石鹸・洗剤の年間平均支出額は、2022年には消費者1人当たりおよそ85.37米ドルとなり、前年比6%増となりました。

- したがって、上記の要因を考慮すると、キレート剤の需要は近い将来、洗浄剤用途分野で大幅に増加すると予想されます。

市場を独占するアジア太平洋地域

- アジア太平洋地域は、中国、インド、日本などの主要国における紙・パルプ部門、洗浄剤、廃水処理、農薬、製薬産業用途などの拡大により、予測期間中、キレート剤市場の最大市場を占めると予想されます。

- アジア太平洋地域は、家庭用および工業用洗剤の需要が最も急速に伸びています。工業化が急速に進んでいるため、これらの国々では便利で使いやすい洗剤が普及しています。

- キレート剤はパルプや紙の漂白に幅広く使用されており、eコマース活動の活発化によって成長が促進されている産業です。紙ベースのフレキシブル・パッケージング・ソリューションは、従来使用されてきたプラスチック・パッケージングに代わる、耐久性があり環境に優しい代替品として台頭してきました。紙ベースの包装の人気は、パルプ・製紙業界におけるキレート剤の需要ファンダメンタルズを強化しています。

- 中国製紙協会が発表したデータによると、世界最大の製紙国である中国のパルプ・紙・紙製品産業の総生産量は、2022年に2億8,391万トンに達しました。これは2021年から1.32%の微増であり、調査対象市場にプラスの影響を与えます。

- また、アジア太平洋地域の廃水処理は、環境規制の強化や日常生活における高品質で安全な水への嗜好の高まりとともに急速に増加しています。中国、インド、日本における飲食品、医薬品、化学、パーソナルケア分野の急成長は、人口規模の拡大と消費者の消費力の強化に伴い、キレート剤の需要を急増させており、市場の成長をさらに高めると思われます。

- 上記の要因が、予測期間中のアジア太平洋地域のキレート剤市場の成長を促進すると思われます。

キレート剤業界の概要

キレート剤市場は、その性質上、部分的に統合されています。主要企業(順不同)には、ダウ、BASF SE、Nouryon、Kemira、三菱化学グループなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 家庭でのクリーナー使用の増加

- パルプ・製紙業界におけるキレート剤消費の増加

- 水処理用途での需要の高まり

- 抑制要因

- 非生分解性キレート剤に伴う環境リスク

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- タイプ

- 非生分解性

- 生分解性

- 用途

- クリーナー

- パルプ・紙

- 水処理

- 農薬

- 化学薬品

- 飲食品

- 医薬品

- パーソナルケア

- その他の用途(写真、繊維加工など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ADM

- Ascend Performance Materials

- Ava Chemicals Pvt. Ltd.

- BASF SE

- Bozzetto Group

- Chemtex Specialty Limited

- Dow

- Hexion

- Kemira

- Lanxess

- Macrocyclics

- Merck KGaA

- Mitsubishi Chemical Holdings Corporation

- Nagase & Co., Ltd.

- Nippon Shokubai Co., Ltd.

- Nouryon

- Shandong IRO Chelating Chemical Co. Ltd.

- Tate & Lyle PLC

- Tosoh Corporation

- Zhonglan Industry Co., Ltd.

第7章 市場機会と今後の動向

- グリーンキレート剤に対する認識と需要の高まり

- 拡大する医薬品産業

The Chelating Agents Market size is estimated at 567.59 Thousand tons in 2024, and is expected to reach 719.59 Thousand tons by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic in 2020. Due to the COVID-19 outbreak in the first half of 2020, the pulp and paper industry experienced a substantial clog in its growth rate. This, in turn, unfavorably impacted the consumption of chelating agents. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Increasing demand for chelating agents from household cleaning applications is expected to fuel market growth.

On the flip side, the adverse effects of non-biodegradable chelating agents on the environment are anticipated to restrain the growth of the market over the forecast period.

Further, the growing demand for green chelating agents in several end-user industries is likely to create lucrative growth opportunities for the global market in the future.

The Asia-Pacific region dominated the market around the world, with countries like China, India, and Japan being the biggest consumers.

Chelating Agents Market Trends

Increasing Consumption of Chelating Agents in Cleaning Applications

- Chelating agents are used majorly in cleaning applications. A variety of cleaning formulations are derived using chelating agents owing to their vital role in preventing interference in the cleaning process from the minerals present in hard water.

- Apart from cleaning, the chelating agents demonstrate many other advantages, such as improving the shelf life of the products being cleaned, maintaining color, imparting antimicrobial effects, preventing allergies from nickel or chromium, etc.

- When used in soaps and detergents, the chelating agents facilitate the prevention of metal staining as well as the premature decomposition of bleaching agents. On the other hand, the chelating agents used in making industrial cleaning solutions aid in scale and rust removal by loosening, breaking up, and dissolving insoluble salt deposits on the equipment's surface.

- The growing consciousness for hygiene maintenance in personal and surrounding spaces has stimulated many global detergent manufacturing companies to tap into the surging demand for domestic cleaning formulations.

- For instance, In May 2022, Proctor & Gamble (P&G), the manufacturer of brands like Aerial and Tide, invested INR 2 billion (~ USD 26.52 million) in the construction of a liquid detergent manufacturing plant in Hyderabad.

- According to the Bureau of Labor Statistics, the average annual expenditures for soaps and detergents in the United States amounted to roughly USD 85.37 per consumer unit in 2022, reflecting an increase of 6% compared to the previous year.

- Therefore, considering the factors mentioned above, the demand for chelating agents is expected to rise in the cleaners application segment significantly in the near future.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to account for the largest market for chelating agents market during the forecast period owing to the expanding paper and pulp sector, cleaners, wastewater treatment, agrochemicals, and pharmaceutical industry applications etc. in major countries such as China, India, Japan, etc.

- The Asia-Pacific is witnessing the fastest growth in the demand for both household and industrial detergents. The fast-paced industrialization has made way for the penetration of convenient and easy-to-apply cleaners in these countries.

- Chelating agents find wide usage in the bleaching of pulp and paper, an industry whose growth is being propelled by the rise in e-commerce activities. The paper-based flexible packaging solutions have emerged as durable and environment-friendly alternatives to conventionally used plastic packaging. The popularity of paper-based packaging has fortified the demand fundamentals for chelating agents in the pulp and paper industry.

- China, the world's largest paper manufacturing country, according to the data published by the China Paper Association, the total output of the pulp, paper, and paper products industry reached 283.91 million tons in 2022. This is a slight increase of 1.32 percent from 2021, thus positively impacting the studied market.

- In addition, the wastewater treatment in the Asia-Pacific region has rapid increase with tightening environmental regulations and a growing preference for high-quality and safe water in day-to-day life. Rapidly growing food and beverage, pharmaceutical, chemical, and personal care sectors in China, India, and Japan, with growing population size and strengthening consumer spending power, are spiraling the demand for chelating agents, which will further enhance the growth of the market studied.

- In June 2022, an environmental protection company that focuses on water environment management, named China Everbright Water, secured the expansion and upgrading project of the Zhangdian East Chemical Industry Park Industrial Wastewater Treatment in Zibo City, Shandong Province. This project will be operated on a BOT (Build-Operate-Transfer) model, with a designed daily industrial wastewater treatment capacity of around 5,000 m3.

- All the factors mentioned above are likely to fuel the growth of the Asia-Pacific chelating agents market over the forecast period.

Chelating Agents Industry Overview

The chelating agents market is partially consolidated in nature. The major players (not in any particular order) include Dow, BASF SE, Nouryon, Kemira, and Mitsubishi Chemical Group Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Cleaners in Households

- 4.1.2 Escalating Chelating Agents Consumption in the Pulp and Paper Industry

- 4.1.3 Growing Demand in Water Treatment Applications

- 4.2 Restraints

- 4.2.1 Environmental Risks Associated With Non-Biodegradable Chelating Agents

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Non-biodegradable

- 5.1.2 Biodegradable

- 5.2 Application

- 5.2.1 Cleaners

- 5.2.2 Pulp and Paper

- 5.2.3 Water Treament

- 5.2.4 Agrochemicals

- 5.2.5 Chemical

- 5.2.6 Food and Beverages

- 5.2.7 Pharmaceuticals

- 5.2.8 Personal Care

- 5.2.9 Other Applications (Photography, Textile Processing, Etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Ascend Performance Materials

- 6.4.3 Ava Chemicals Pvt. Ltd.

- 6.4.4 BASF SE

- 6.4.5 Bozzetto Group

- 6.4.6 Chemtex Specialty Limited

- 6.4.7 Dow

- 6.4.8 Hexion

- 6.4.9 Kemira

- 6.4.10 Lanxess

- 6.4.11 Macrocyclics

- 6.4.12 Merck KGaA

- 6.4.13 Mitsubishi Chemical Holdings Corporation

- 6.4.14 Nagase & Co., Ltd.

- 6.4.15 Nippon Shokubai Co., Ltd.

- 6.4.16 Nouryon

- 6.4.17 Shandong IRO Chelating Chemical Co. Ltd.

- 6.4.18 Tate & Lyle PLC

- 6.4.19 Tosoh Corporation

- 6.4.20 Zhonglan Industry Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Awareness and Demand for Green Chelating Agents

- 7.2 Expanding Pharmaceutical Industry