|

市場調査レポート

商品コード

1407054

胃腸機器:市場シェア分析、産業動向・統計、2024~2029年成長予測Gastrointestinal Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 胃腸機器:市場シェア分析、産業動向・統計、2024~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

胃腸機器市場は予測期間中にCAGR 7.4%を記録する見込み

主なハイライト

- COVID-19パンデミックは、当初は他の慢性疾患の治療の封鎖、中止、遅延の賦課により、胃腸機器市場に悪影響を及ぼしました。パンデミックの間、胃腸処置を含む他の疾患の治療や外科処置が延期または中止されたため、これは胃腸デバイスの需要減少につながりました。例えば、2021年4月にClinical Journal of Gastroenterologyに掲載された研究では、パンデミックの間、急性虫垂炎や急性石灰沈着性胆嚢炎など多くの腹部疾患の手術が延期されたと言及されています。しかし、パンデミック後はCOVID-19の患者数が減少したため、消化器疾患など他の慢性疾患の手術が再開され、市場は正常なペースで成長しています。このように、COVID-19のパンデミックは前段階では市場に悪影響を与えました。しかし、パンデミック後の段階では、世界的に消化器疾患の治療が再開されたため、市場は通常のペースを取り戻し、予測期間中も同様の状態が続くと予想されます。

- 市場の成長を後押しする主な要因は、胃腸疾患の増加と老人人口の増加です。

- 例えば、国際消化器疾患財団の2022年最新情報によると、世界では人口の5~10%が炎症性腸疾患に罹患していると推定されています。米国では年間240万~350万人が消化器内科を受診しています。このような要因が消化器機器の採用を後押しし、調査された市場成長に寄与すると考えられます。また、消化器癌、大腸炎などの消化器疾患の負担増も市場成長を促進すると予想されます。例えば、スペイン癌登録ネットワークが2021年に発表したデータによると、スペインでは2021年に結腸癌29,372例以上、直腸癌14,209例以上、胃癌7,313例以上が推定されています。さらに、クローン病・大腸炎UKが2022年3月に発表したデータによると、英国では123人に1人が潰瘍性大腸炎またはクローン病であると報告されています。このように、消化器疾患の負担が増加するにつれて、これらの疾患の診断と治療に対する需要が増加することが予想され、これが今後数年間の市場の成長を押し上げると予測されます。

- さらに、著名な市場プレーヤーによる新製品の発売は、市場の成長を後押しすると予想されます。例えば、2023年1月、富士フイルムはClutchCutterとFushKnifeを発売し、内視鏡ソリューションポートフォリオの拡充を発表しました。ClutchCutterは回転可能な鉗子で、臨床医の切開、剥離、凝固をサポートします。ギザギザの鋸歯状のジョーが特徴で、クラッチ能力が向上し、外縁は絶縁されているため耐久性に優れています。

- 同様に、2021年11月、Micro-Tech Endoscopy社は、極細ニチノールワイヤーを使用した新しいコールドスネアであるLesionHunterコールドスネアを市場に投入しました。LesionHunterニチノール製スネアは、コールドスネアポリペクトミーを進歩させるために特別に設計されました。このように、先進的な製品の発売により、調査対象市場は予測期間中に大きく成長することが期待されます。

- したがって、消化器疾患の負担の増加や主要企業による製品の発売により、調査された市場は分析期間中に成長を示すと予想されます。

- しかし、熟練した技術者の不足と複雑な滅菌手順、不利な報酬政策、政府からの低資金が、予測期間中の市場成長を阻害する可能性があります。

消化器デバイス市場の動向

内視鏡的逆行性胆管膵管造影装置(ERCP)は予測期間中に大幅な成長が見込まれる

- 内視鏡的逆行性胆管膵管造影装置は、内視鏡と透視を組み合わせた手技を実施できるサイドビュー十二指腸鏡です。胃腸炎の罹患率の上昇や成人人口における消化器疾患の増加傾向などの動向が、予測期間中に内視鏡的逆行性胆管膵管造影装置市場の需要を促進すると予想されています。

- 調査研究では、内視鏡的逆行性胆管膵管造影装置の利点と有効性が強調されており、この分野にはさらなる機会が生まれると予想されています。例えば、2021年8月にWorld Journal of Gastrointestinal Endoscopyに掲載された研究では、内視鏡的逆行性胆管膵管造影(ERCP)はよりゆっくりと進化してきたが、パンデミックの発生にもかかわらず、急速な発展を伴う技術革新の時期があったと説明しています。再使用可能な十二指腸内視鏡が院内感染の原因となることが懸念されるようになり、使い捨ての部品や使い捨ての十二指腸内視鏡への動向が現れています。

- さらに、2021年4月にJournal of Clinical Medicine誌に掲載された研究では、外科的に解剖学的構造が変化した患者のためのインターベンショナル内視鏡的逆行性胆管膵管造影装置における最近の技術的進歩が強調されています。

- この研究ではまた、バルーン内視鏡でアクセスできない場合に、腹腔鏡補助下内視鏡的逆行性胆管膵管造影装置が乳頭や肝空腸吻合の標的部位にアクセスするために利用されていることにも言及しています。このような研究は、内視鏡的逆行性胆管膵管造影装置の利点を強調し、これらの装置の採用を増加させ、それによって市場の成長を急増させると予想されます。

- さらに、2022年11月、上海オペレーションロボットは、胆道ステント留置手術を行うためのERCP(内視鏡的逆行性胆管膵管造影)ロボットの初期臨床試験の結果を実証しました。この手術は、ロボット支援による胆道ステント留置手術の初のヒト臨床試験であり、Aopeng Medical社によって実施されました。このような発展は、内視鏡的逆行性胆道膵管造影装置の市場浸透率を高めると予想され、予測期間中の同分野の成長を後押しすると期待されます。

- そのため、内視鏡的逆行性胆管膵管造影装置分野は、関連する調査研究や技術進歩の増加により、予測期間中に大きな成長が見込まれます。

北米は予測期間中に大きな成長が見込まれる

- 北米市場は、消化器疾患の負担が大きいことと、同地域に有力な市場プレーヤーが存在することから、成長が見込まれています。例えば、米国癌協会が2023年に発表したデータによると、米国では2023年に1億5,302万人を超える大腸癌の新規症例が発生すると推定されています。さらに、カナダ癌協会が2022年5月に発表したデータでは、2022年にカナダで4100人以上が胃癌と診断されると推定されています。

- また、2021年にCrohn's and Colitis Canadaが発表したデータによると、カナダでは3億人以上が炎症性腸疾患に罹患していると推定され、2030年にはさらに4億300万人に増加すると予測されています。このように、消化器疾患や消化器障害(胃食道逆流症、癌、過敏性腸症候群、乳糖不耐症、食道裂孔ヘルニア)の負担が大きいことから、北米の消化器機器市場は予測期間中に大きな成長を遂げる可能性が高いです。

- 米国の胃腸機器市場の成長を促進する要因としては、主要製品の発売、高齢者患者の集中、複数のメーカーの同国におけるプレゼンスなどが挙げられます。例えば、2022年5月、Lumendi, LLC社は、内視鏡的粘膜切除術(EMR)や大腸内視鏡検査を目的とした使い捨て内視鏡治療器「DiLumen EZ1」が米国食品医薬品局(FDA)の510(k)承認を取得したと発表しました。

- 同様に、2022年2月、Motus GI社は、米国FDAからPure-Vu EVSシステムの販売許可を取得しました。このシステムは、曲がりくねった解剖学的構造におけるセットアップの迅速化とナビゲーションの改善を目的としています。また、医師が大腸内視鏡検査中に準備の不十分な大腸の障害を素早く克服するのにも役立ちます。さらに、2021年4月、米国食品医薬品局は、臨床医が大腸の潜在的な異常をリアルタイムで発見できるよう人工知能を採用した初の医療機器、GI GeniusTMインテリジェント内視鏡モジュールのデノボ・クリアランスを承認しました。GI Geniusモジュールは、大腸ポリープを検出するための、人工知能(AI)ベースのコンピュータ支援検出(CADe)システムとして、最初で唯一の市販品です。

- したがって、このような消化器疾患の高い負担と大手企業の存在が、北米地域における調査市場の成長を後押しすると予想されます。

胃腸機器産業の概要

胃腸機器市場は、世界的および地域的に事業を展開する複数の企業の存在により、適度に断片化されています。競合情勢には、市場シェアを持ち知名度の高い国際企業や地元企業の分析が含まれます。これらには、Boston Scientific Corporation、CONMED Corporation、Stryker、Medtronic、Olympus Corporation、KARL STORZ SE &Co.KG、Cook Group Incorporatedなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 胃腸疾患の有病率の増加

- 老年人口の増加

- 市場抑制要因

- 熟練技術者の不足と複雑な滅菌手順

- 不利な補償政策と低い政府資金

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 製品タイプ別

- Giビデオスコープ

- 生検装置

- 内視鏡的逆行性胆管膵管造影装置(ERCP)

- カプセル内視鏡

- 超音波内視鏡

- その他の製品タイプ

- エンドユーザー別

- 病院

- クリニック

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Boston Scientific Corporation

- CONMED Corporation

- Stryker

- Medtronic

- Olympus Corporation

- KARL STORZ SE & Co. KG

- Cook Group Incorporated

- B. Braun SE

- Johnson & Johnson

- Micro-tech

- PENTAX Medical

第7章 市場機会と今後の動向

The gastrointestinal devices market is expected to register a CAGR of 7.4% over the forecast period.

Key Highlights

- The COVID-19 pandemic had an adverse impact on the gastrointestinal devices market initially due to the imposition of lockdown, cancellation, and delay of the treatment of other chronic diseases. This led to a decline in the demand for gastrointestinal devices as the treatment and surgical procedures for other diseases, including gastrointestinal procedures, were postponed or canceled during the pandemic. For instance, a study published in the Clinical Journal of Gastroenterology in April 2021 mentioned that surgeries for many abdominal diseases, such as acute appendicitis and acute calculous cholecystitis, were postponed amid the pandemic. However, in the post-pandemic, the number of COVID-19 patients decreased, which led to the resumption of other chronic diseases, such as gastrointestinal diseases, thereby helping the market to grow at a normal pace. Thus, the COVID-19 pandemic adversely impacted the market in its preliminary phase. However, the market gained the normal pace in the post-pandemic phase with the resumption of gastrointestinal disease treatment globally and is expected to continue the same over the forecast period.

- The major factors fuelling the market's growth are the rise in gastrointestinal diseases and the increasing geriatric population.

- For instance, according to the International Foundation for Gastrointestinal Disorders 2022 update, it was estimated that 5-10% of the population has inflammatory bowel disease worldwide. Gastroenterologist visits in the United States were found to be 2.4 to 3.5 million yearly. Such factors are likely to boost the adoption of gastrointestinal devices, thereby contributing to the studied market growth. The increasing burden of gastrointestinal diseases such as gastrointestinal cancer, colitis, and others is also expected to propel the market growth. For instance, as per the data published by the Spanish Network of Cancer Registries in 2021, over 29,372 cases of Colon cancer, 14,209 cases of recto cancer, and over 7,313 cases of stomach cancer were estimated for 2021 in Spain. Furthermore, as per the data published by Crohn's & Colitis UK in March 2022, one in every 123 individuals in the United Kingdom was reported to have either ulcerative Colitis or Crohn's disease. Thus, with the increasing burden of gastrointestinal diseases, the demand for the diagnosis and treatment of these diseases is expected to increase, which is anticipated to boost the growth of the market in the upcoming years.

- Furthermore, new product launches by prominent market players are anticipated to favor market growth. For instance, in January 2023, Fujifilm announced the expansion of its endoscopy solutions portfolio by launching the ClutchCutter and FushKnife. ClutchCutter is a rotatable forceps that supports clinicians in making incisions, dissections, and coagulation. The solution features jagged, serrated jaws for enhanced clutching ability and an insulated outer edge for maximum durability.

- Similarly, in November 2021, Micro-Tech Endoscopy launched the LesionHunter Cold Snare, a novel cold snare with an ultra-thin Nitinol wire, to the market. The LesionHunter nitinol snare was specifically designed to advance cold snare polypectomy. Thus, owing to the advanced product launches, the studied market is expected to have significant growth over the forecast period.

- Therefore, owing to the increasing burden of gastrointestinal diseases and product launches by the key players, the studied market is anticipated to witness growth over the analysis period.

- However, a lack of skilled technicians & complex sterilization procedures, unfavorable compensation policies, and low government funding may impede the market growth over the forecast period.

Gastrointestinal Devices Market Trends

Endoscopic Retrograde Cholangiopancreatography Devices (ERCP) is Expected to Witness Significant Growth Over the Forecast Period

- The endoscopic retrograde cholangiopancreatography device is a side-viewing duodenoscope capable of conducting combined endoscopic and fluoroscopic procedures. Factors such as the rising incidence of gastroenteritis and an increasing trend of digestive disorders in the adult population are expected to propel the demand for the endoscopic retrograde cholangiopancreatography devices market over the forecast period.

- Research studies have highlighted the advantages and efficacy of endoscopic retrograde cholangiopancreatography devices, which are anticipated to create more opportunities for the segment. For instance, a study published in the World Journal of Gastrointestinal Endoscopy in August 2021 explains endoscopic retrograde cholangiopancreatography (ERCP) has evolved more slowly, yet there have been periods of innovation with fast development in spite of the outbreak of the pandemic. With an increasing concern regarding reusable duodenoscopes being linked to nosocomial outbreaks, a trend toward disposable components and disposable duodenoscopes has emerged.

- Further, a study published in the Journal of Clinical Medicine in April 2021 highlighted the recent technological advancements in interventional endoscopic retrograde cholangiopancreatography devices for patients with surgically altered anatomy.

- The study also mentioned that laparoscopy-assisted endoscopic retrograde cholangiopancreatography devices are utilized to access the target site of the papilla or hepaticojejunal anastomosis when it cannot be accessed by balloon enteroscopy. Such studies highlight the advantage of endoscopic retrograde cholangiopancreatography devices, which is anticipated to increase the adoption of these devices, thereby surging the market growth.

- Furthermore, in November 2022, Shanghai Operation Robot Co., Ltd. demonstrated the results of its initial clinical trial of an ERCP (Endoscopic retrograde cholangiopancreatography) robot for performing biliary stent placement surgery. The surgery is the first robot-assisted human clinical trial of biliary stent placement surgery and was conducted by Aopeng Medical. Such developments are expected to increase the market penetration of endoscopic retrograde cholangiopancreatography devices, which is expected to bolster the segment's growth over the forecast period.

- Therefore, the endoscopic retrograde cholangiopancreatography devices segment is expected to witness significant growth over the forecast period due to the increasing related research works and technological advancements.

North America is Expected to Witness Significant Growth Over the Forecast Period

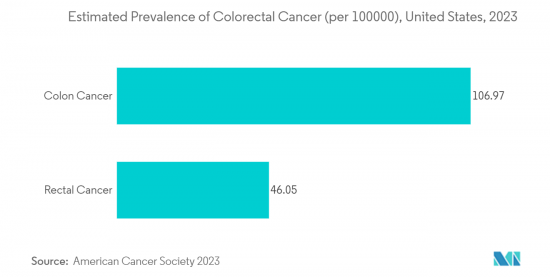

- The North American market is expected to grow owing to the high burden of gastrointestinal diseases and the presence of leading market players in the region. For instance, the data published by the American Cancer Society in 2023 stated that over 153.02 million new cases of colorectum cancer were estimated in the United States in 2023. Furthermore, as per the data published by the Canada Cancer Society in May 2022, it was estimated that over 4,100 people were estimated to be diagnosed with stomach cancer in Canada in 2022.

- Also, the data published by Crohn's and Colitis Canada in 2021 stated that over 300.0 million people in Canada were estimated to have inflammatory bowel disease, and it is expected to increase further to 403.0 million by 2030. Thus, owing to such a high burden of gastrointestinal diseases and digestive disorders (gastroesophageal reflux disease, cancer, irritable bowel syndrome, lactose intolerance, and hiatal hernia), the North American gastrointestinal devices market is likely to grow at a large rate over the forecast period.

- The factors driving the growth of the gastrointestinal devices market in the United States include key product launches, a high concentration of geriatric patients, and several manufacturer's presence in the country. For instance, in May 2022, Lumendi, LLC announced that the DiLumen EZ1, a single-use, disposable endo-therapy device intended for endoscopic mucosal resections (EMR) and colonoscopies, received the United States Food and Drug Administration 510(k) approval.

- Similarly, in February 2022, Motus GI received U.S. FDA clearance to market the Pure-Vu EVS System, which is intended to speed the set-up and improve navigation in tortuous anatomy. It also helps physicians to quickly overcome the obstacles of poorly prepared colons during a colonoscopy. Furthermore, in April 2021, the United States Food and Drug Administration approved the first medical device that employs artificial intelligence to help clinicians spot potential anomalies in the colon in real-time, de novo clearance for the GI GeniusTM intelligent endoscopy module. The GI Genius module is the first and only commercially available artificial intelligence (AI)-based computer-aided detection (CADe) system for detecting colorectal polyps.

- Therefore, such a high burden of gastrointestinal diseases and the presence of leading players are expected to boost the growth of the studied market in the North American region.

Gastrointestinal Devices Industry Overview

The gastrointestinal devices market is moderately fragmented due to the presence of several companies operating globally and regionally. The competitive landscape includes an analysis of a few international and local companies that hold market shares and are well known. These include Boston Scientific Corporation, CONMED Corporation, Stryker, Medtronic, Olympus Corporation, KARL STORZ SE & Co. KG, and Cook Group Incorporated.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Gastrointestinal Diseases

- 4.2.2 Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Technicians & Complex Sterilization Procedures

- 4.3.2 Unfavourable Compensation Policies and Low Government Funding

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Gi Videoscopes

- 5.1.2 Biopsy Devices

- 5.1.3 Endoscopic Retrograde Cholangiopancreatography Devices (ERCP)

- 5.1.4 Capsule Endoscopy

- 5.1.5 Endoscopic Ultrasound

- 5.1.6 Other Product Types

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Clinics

- 5.2.3 Other End-Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 CONMED Corporation

- 6.1.3 Stryker

- 6.1.4 Medtronic

- 6.1.5 Olympus Corporation

- 6.1.6 KARL STORZ SE & Co. KG

- 6.1.7 Cook Group Incorporated

- 6.1.8 B. Braun SE

- 6.1.9 Johnson & Johnson

- 6.1.10 Micro-tech

- 6.1.11 PENTAX Medical