|

市場調査レポート

商品コード

1690143

電力エンジニアリング・調達・建設(EPC)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Power Engineering, Procurement, And Construction (EPC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電力エンジニアリング・調達・建設(EPC)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

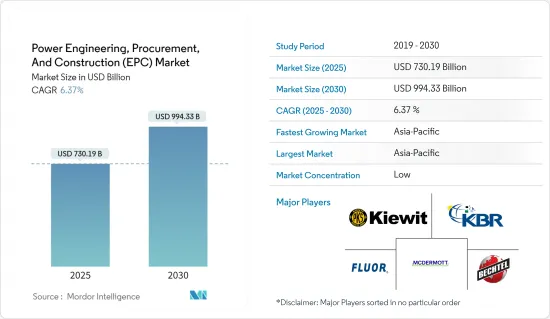

電力エンジニアリング・調達・建設市場規模は2025年に7,301億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.37%で、2030年には9,943億3,000万米ドルに達すると予測されます。

主要ハイライト

- 長期的には、発電量の増加、エネルギー消費需要、発電産業の力学の変化といった要因が、電力EPC市場の需要を促進すると予想されます。さらに、再生可能エネルギーに対する政府支出の増加など、電力セクタへの投資が市場をさらに押し上げると予想されます。

- 一方、世界中の発電で大きなシェアを占める石炭ベースの発電所の段階的廃止や、いくつかの上流プロジェクトの遅れにつながる不安定な原油価格は、電力EPC市場の成長を妨げると予想されます。

- 超臨界圧や超々臨界圧の石炭発電所のような新しく効率的な技術や、再生可能エネルギーのシェアを拡大するための政府の取り組みが、将来的に電力EPC市場にいくつかの機会を生み出すと予想されます。

- 予測期間中、アジア太平洋が最大の市場になると予想されます。これは、高い都市化率と、主に中国とインドからの電力需要の増加によるものです。

電力EPC市場動向

市場セグメンテーションは再生可能エネルギーが急成長の見込み

- 温室効果ガスの排出や気候変動など、化石燃料が環境に与える悪影響に対する認識が世界的に高まっています。政府、組織、個人は、二酸化炭素排出量の削減と、よりクリーンなエネルギー源への移行にますます力を入れています。太陽光、風力、水力、バイオマスなどの再生可能エネルギーは、化石燃料に代わる持続可能で低炭素な代替エネルギーを提供し、再生可能プロジェクトへの需要を牽引しています。

- さらに、長年にわたって再生可能エネルギー技術のコストは大幅に低下し、従来のエネルギー源との競合が高まっています。ソーラーパネルの効率、風力タービン技術、エネルギー貯蔵システムの継続的な進歩は、再生可能エネルギープロジェクトの信頼性、拡大性、費用対効果を向上させました。これは投資家の信頼を高め、EPC企業やプロジェクト開発者にとって再生可能エネルギーがより魅力的なものとなりました。

- 国際再生可能エネルギー機関(IRENA)の報告によると、2023年の世界の再生可能エネルギー設備容量は約3.9テラワットに達し、前年から14%近く急増しました。過去数十年にわたり、再生可能エネルギー部門は、技術コストの急落と従来のエネルギー源に対する環境的懸念の高まりにより、急成長を遂げてきました。

- さらに、世界各国の政府は、再生可能エネルギーの導入を促進するための支援施策やインセンティブを実施しています。これらの施策には、固定価格買取制度、税額控除、補助金、再生可能エネルギーポートフォリオ基準などが含まれます。これにより、再生可能エネルギープロジェクトにとって有利なビジネス環境が構築されています。安定した長期的な施策は、予測可能な市場展望を提供し、再生可能エネルギーEPCプロジェクトへの投資を促進します。

- 例えば、インド政府は2023年4月、今年度の最初の2四半期に15GWのプロジェクトのオークションを実施する計画を発表しました。さらに、その後の四半期にも約10GWのプロジェクトが提供される予定です。オークションは、Solar Energy Corp. of India Ltd.、NTPC Ltd.、NHPC Ltd.、SJVN Ltd.などの国営電力会社が政府に代わって実施します。

- WindEuropeの報告によると、風力発電市場の成熟した参入企業である欧州では、2023年に1,830万kWの新規風力発電容量が追加されました。このうちEU-27は過去最高の1,620万kWを占めました。しかし、この数字はEUの2030年の気候エネルギー目標を達成するために必要な容量の半分にすぎないです。新規設備の79%は陸上設備であったが、オフショア設備は過去最高の380万kWに達しました。オフショア容量の増加にもかかわらず、予測では2030年までの設置の3分の2は陸上にとどまる。

- 今後、欧州では2024~2030年までに260GWの風力発電容量が新たに追加される予定です。EU-27はこのうち200GW、年平均29GWの貢献が見込まれています。しかし、2030年の気候エネルギー目標に沿うためには、EUはそのペースを年間33GWまで加速させなければならないです。この予想される急増は、今後数年間の風力発電EPC市場に大きな活力を与えることになります。

- 2024年10月、Mitsubishi Heavy Industries, Ltd.(MHI)の一部門であるMitsubishi Powerは、風力発電のEPC(エンジニアリング・調達・建設)事業を開始しました。2024年10月、Mitsubishi Heavy Industries, Ltd.の一部門であるMitsubishi Powerは、宮崎県日向市に50メガワット(MW)の木質バイオマス焚き火力発電所を完成させました。日向バイオマス火力発電所は、Mitsubishi Heavy Industries, Ltd.を中心とするコンソーシアムが、エンジニアリング・調達・建設(EPC)を一括して請け負うフルターンキーソリューション。運営は特別目的会社(SPC)である日向バイオマスパワーが行っています。

- 以上のことから、再生可能エネルギーは予測期間中、市場調査において重要な役割を果たすと予想されます。

アジア太平洋が市場を独占する見込み

- 中国、インド、日本、韓国、東南アジアなどで構成されるアジア太平洋は、力強い経済成長を遂げています。この成長により、工業化、都市化、インフラ整備が進み、新しい電力プロジェクトの需要が高まり、EPCサービスの大きな市場が形成されています。

- Asia-Pacific Population and Development Report 2023によると、アジア太平洋には世界人口の60%以上と大都市の60%が集中しています。今後、再生可能エネルギー源の普及、電力消費の増加、電力へのアクセスの増加、送電網インフラの拡大・強化により、同大陸では電力需要が増加することが予想されます。中国、インド、日本、オーストラリアといった国々が、この地域における主要な貢献国になると予想されます。

- 例えば、BP Statistical Review of World Energy 2023によると、この地域の一次エネルギー消費量は2013年の219.8エクサジュールから2023年には291.77エクサジュールに増加し、2022年の水準から4.7%増加しました。

- さらに、アジア太平洋の多くの国々は、気候変動の懸念に対処し、化石燃料への依存を減らし、エネルギー安全保障を強化するために、野心的な再生可能エネルギー目標を設定しています。各国政府は、再生可能エネルギー開発を促進するために、有利な施策、インセンティブ、規制の枠組みを導入しています。その結果、太陽光発電、風力発電、水力発電などの再生可能エネルギープロジェクトが急増し、EPC企業にとって活況を呈しています。

- さらに、インド政府は二酸化炭素排出を抑制するため、再生可能エネルギーに多額の投資を行っています。これには、さまざまな大規模持続可能電力プロジェクトの立ち上げや、グリーンエネルギーイニシアティブの推進などが含まれます。2024年10月現在、インドの再生可能エネルギー容量は203.22GWに達し、太陽光発電(92.12GW)と風力発電(47.72GW)が設備容量に大きく貢献しています。同国は2031~32年までに再生可能エネルギー設備容量500GWという野心的な目標を掲げており、電力EPC市場の成長を後押ししています。

- 2024年9月、インドは洋上風力発電プロジェクトの入札を開始し、再生可能エネルギーの旅において極めて重要な瞬間を迎えました。この入札は、新・再生可能エネルギー省傘下のSolar Energy Corporation of India Ltd(SECI)が、グジャラート州沖に位置する500MWの洋上風力発電所の入札を募集するものです。落札者はSECIと25年間の電力購入契約(PPA)を結び、風力発電所の建設、所有、運営を担う。

- 大規模な再生可能エネルギー発電プロジェクトの急増により、総発電量に占める石炭の割合は2020年の62%から2023年には49.5%まで減少しました。2024年10月、再生可能エネルギー目標による新規発電所容量の承認を担当するクリーンエネルギー規制当局は、2024年の大規模風力・太陽光発電容量の承認予測を3GWから4GWに引き上げました。2024年の新規再生可能エネルギー発電容量は7GWを超え、これに3.1GWの小規模発電容量が加わると予想されます。これらの発表を受けて、2024年の再生可能エネルギー発電プロジェクトの容量(160万kW)は、2023年の合計容量(130万kW)を上回りました。

- したがって、急速な経済成長、都市化、政府のイニシアティブ、再生可能エネルギー導入、インフラ開発、産業需要、技術進歩に牽引され、アジア太平洋が市場を独占することになります。

電力EPC産業概要

電力EPC市場は細分化されています。市場の主要参入企業(順不同)には、Fluor Corp.、KBR Inc.、Kiewit Corporation、McDermott International Ltd.、Bechtel Corporation、Saipem SpAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 2029年までの設置容量と予測

- 一次エネルギー消費量(単位:MTOE、2023年)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- エネルギー需要の増大

- 再生可能エネルギー源の採用増加

- 抑制要因

- 従来の電力源の段階的廃止

- 高い初期投資コストと限られた天然リソース

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 投資分析

第5章 市場セグメンテーション

- 発電

- 火力

- 原子力

- 再生可能エネルギー

- 送配電(T&D)-(定性分析のみ)

- 市場分析:地域別{2028年までの市場規模・需要予測(地域による)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- イタリア

- スペイン

- フランス

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- EPC Developers

- Fluor Ltd

- John Wood PLC

- Kiewit Corporation

- McDermott International Inc.

- Bechtel Corporation

- Saipem SpA

- Larsen & Toubro Limited

- KBR Inc

- Original Equipment Manufacturers(OEMs)

- General Electric Company

- Siemens Energy AG

- ABB Ltd

- Schneider Electric SE

- Eaton Corporation PLC.

- EPC Developers

第7章 市場機会と今後の動向

- 送電網の近代化とスマート技術

The Power Engineering, Procurement, And Construction Market size is estimated at USD 730.19 billion in 2025, and is expected to reach USD 994.33 billion by 2030, at a CAGR of 6.37% during the forecast period (2025-2030).

Key Highlights

- Over the long term, factors such as increased electricity generation, energy consumption demand, and changing power generation industry dynamics are expected to drive demand for the power EPC market. Moreover, investments in the power sector, including increased government spending on renewable energy, are further expected to boost the market.

- On the other hand, the phasing out of coal-based power plants, which account for a major share in power generation around the globe, and volatile crude oil prices leading to delays in several upstream projects are expected to hinder the growth of the power EPC market.

- Nevertheless, new and efficient technologies like supercritical and ultra-supercritical coal power plants and government initiatives to increase renewable energy's share are expected to create several opportunities for the power EPC market in the future.

- Asia-Pacific is expected to be the largest market during the forecast period. It is due to the high urbanization growth rate and growing electricity demand, mainly from China and India.

Power Engineering, Procurement, And Construction (EPC) Market Trends

Renewable Expected to be the Fastest-growing Market Segment

- There is a growing global awareness of the adverse impacts of fossil fuels on the environment, including greenhouse gas emissions and climate change. Governments, organizations, and individuals increasingly commit to reducing carbon emissions and transitioning to cleaner energy sources. Renewable energy, such as solar, wind, hydroelectric, and biomass, offers a sustainable and low-carbon alternative to fossil fuels, driving the demand for renewable projects.

- Moreover, over the years, the costs of renewable energy technologies significantly declined, making them increasingly competitive with conventional energy sources. The continuous advancements in solar panel efficiency, wind turbine technology, and energy storage systems improved renewable energy projects' reliability, scalability, and cost-effectiveness. It boosted investors' confidence and made renewable energy more attractive for EPC companies and project developers.

- In 2023, global installed renewable energy capacity hit approximately 3.9 terawatts, marking a nearly 14 percent surge from the prior year, as reported by the International Renewable Energy Agency (IRENA). Over the past few decades, the renewable energy sector has witnessed a meteoric rise, driven by plummeting technology costs and growing environmental concerns over conventional energy sources.

- Additionally, governments worldwide are implementing supportive policies and incentives to promote renewable energy deployment. These policies include feed-in tariffs, tax credits, grants, and renewable portfolio standards. It creates a favorable business environment for renewable energy projects. Stable and long-term policies provide a predictable market outlook and encourage investments in renewable EPC projects.

- For instance, in April 2023, the Indian government announced plans to conduct auctions for 15 GW of projects in the first two quarters of the current fiscal year, 2023. Additionally, approximately 10 GW of projects will be offered in subsequent quarters. The auctions will be conducted by state-run power companies, including Solar Energy Corp. of India Ltd., NTPC Ltd., NHPC Ltd., and SJVN Ltd., on behalf of the government.

- In 2023, Europe, a mature player in the wind power market, added 18.3 GW of new wind power capacity, as reported by WindEurope. Of this, the EU-27 accounted for a record 16.2 GW. However, this figure is only half of the capacity needed to meet the EU's 2030 climate and energy targets. While 79% of the new installations were onshore, offshore installations reached a record 3.8 GW. Despite the growth in offshore capacity, projections indicate that two-thirds of installations through 2030 will remain onshore.

- Looking ahead, Europe is set to add 260 GW of new wind power capacity from 2024 to 2030. The EU-27 is expected to contribute 200 GW of this total, averaging 29 GW annually. However, to align with its 2030 climate and energy targets, the EU must accelerate its pace to 33 GW per year. This anticipated surge is poised to significantly energize the wind power EPC market in the coming years.

- In October 2024, Mitsubishi Power, a division of Mitsubishi Heavy Industries, Ltd. (MHI), completed a 50-megawatt (MW) woody biomass-fired power plant in Hyuga, Miyazaki Prefecture. The Hyuga Biomass Power Plant, a product of a consortium led by MHI, is a full turnkey solution for engineering, procurement, and construction (EPC). The facility will be operated by Hyuga Biomass Power Co., Ltd., a special purpose company (SPC).

- Therefore, according to the above points, renewable energy is expected to play a significant role in market studies during the forecasted period.

Asia-Pacific Expected to Dominate the Market

- The Asia-Pacific region, comprising countries such as China, India, Japan, South Korea, and Southeast Asia, is experiencing robust economic growth. This growth increased industrialization, urbanization, and infrastructural development, driving the demand for new power projects and creating a significant market for EPC services.

- According to the Asia-Pacific Population and Development Report 2023, the Asia-Pacific region is home to more than 60% of the global population and 60% of the large cities. In the future, the continent will witness increasing demand for power due to the increasing penetration of renewable energy sources, rising power consumption, and growing access to electricity, expanding and enhancing the power grid infrastructure. Countries like China, India, Japan, and Australia are expected to be the key contributing nations in the region.

- For instance, according to the BP Statistical Review of World Energy 2023, primary energy consumption in the region increased from 219.8 exajoules in 2013 to 291.77 exajoules in 2023, representing a 4.7% increase from 2022 levels.

- Furthermore, many countries in the Asia-Pacific region set ambitious renewable energy targets to address climate change concerns, reduce dependence on fossil fuels, and enhance energy security. Governments implement favorable policies, incentives, and regulatory frameworks to promote renewable energy development. As a result, there is a surge in renewable energy projects such as solar, wind, and hydroelectric power, creating a thriving market for EPC firms.

- Moreover, the Government of India is investing significantly in renewable energy to curb carbon emissions. This includes launching various large-scale sustainable power projects and championing green energy initiatives. As of October 2024, India's renewable energy capacity reached 203.22 GW, with solar power (92.12 GW) and wind (47.72 GW) majorly contributing to installed capacity. The nation aims for an ambitious target of 500 GW of installed renewable energy capacity by 2031-32, bolstering the growth of the power EPC market.

- In September 2024, India marked a pivotal moment in its renewable energy journey by unveiling its inaugural offshore wind project tender. The tender, issued by the Solar Energy Corporation of India Ltd (SECI) - an entity under the Ministry of New and Renewable Energy - seeks bids for a 500-MW offshore wind farm situated off the coast of Gujarat. The successful bidder will secure a 25-year power purchase agreement (PPA) with SECI and take on the responsibilities of constructing, owning, and operating the wind farm.

- Due to surging large-scale renewable energy projects, coal's share in the total electricity generation dwindled from 62% in 2020 to 49.5% in 2023. In October 2024, The Clean Energy Regulator, responsible for approving new power station capacities under the Renewable Energy Target, upped its forecast for large-scale wind and solar capacity approvals from 3GW to 4GW for 2024. The total new renewable capacity is projected to surpass 7GW in 2024, complemented by an anticipated 3.1GW of small-scale capacity. Following these announcements, the capacity of financially committed renewable electricity generation projects for 2024 (1.6 GW) has eclipsed the total for 2023 (1.3 GW).

- Therefore, driven by rapid economic growth, urbanization, government initiatives, renewable energy deployment, infrastructure development, industrial demand, and technological advancements, Asia-Pacific is set to dominate the market.

Power Engineering, Procurement, And Construction (EPC) Industry Overview

The power engineering, procurement, and construction (EPC) market is fragmented. Some of the major players in the market (in no particular order) include Fluor Corp., KBR Inc., Kiewit Corporation, McDermott International Ltd, Bechtel Corporation, and Saipem SpA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, Till 2029

- 4.3 Installed Capacity and Forecast, Till 2029

- 4.4 Primary Energy Consumption, in MTOE, 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Growing Energy Demand

- 4.7.1.2 Increasing Adoption Of Renewable Energy Sources

- 4.7.2 Restraints

- 4.7.2.1 Phasing Out of Conventional Sources of Electricity

- 4.7.2.2 High Initial Investment Cost And Limited Natural Resources

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products and Services

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Power Generation

- 5.1.1 Thermal

- 5.1.2 Nuclear

- 5.1.3 Renewables

- 5.2 Power Transmission and Distribution (T&D) - (Qualitative Analysis Only)

- 5.3 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 Spain

- 5.3.2.5 France

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Chile

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 EPC Developers

- 6.3.1.1 Fluor Ltd

- 6.3.1.2 John Wood PLC

- 6.3.1.3 Kiewit Corporation

- 6.3.1.4 McDermott International Inc.

- 6.3.1.5 Bechtel Corporation

- 6.3.1.6 Saipem SpA

- 6.3.1.7 Larsen & Toubro Limited

- 6.3.1.8 KBR Inc

- 6.3.2 Original Equipment Manufacturers (OEMs)

- 6.3.2.1 General Electric Company

- 6.3.2.2 Siemens Energy AG

- 6.3.2.3 ABB Ltd

- 6.3.2.4 Schneider Electric SE

- 6.3.2.5 Eaton Corporation PLC.

- 6.3.1 EPC Developers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Grid Modernization and Smart Technologies